Aluminum Scrap Market Outlook 2026 to 2030: CBAM & Gulf War

Introduction

The global aluminum industry is undergoing a significant transformation driven by Europe's Carbon Border Adjustment Mechanism (CBAM), geopolitical tensions in the Gulf region, decarbonization initiatives, and rising demand for recycled metals. CBAM is encouraging greater utilization of low-carbon aluminum and increasing demand for recycled aluminum scrap across Europe and Asia. Simultaneously, Gulf region conflicts are disrupting logistics, freight rates, energy costs, and raw material flows. These developments are reshaping global aluminum scrap trade patterns, secondary aluminum production economics, and investment strategies. India and China are emerging as major beneficiaries of changing scrap flows, while Africa and Latin America offer substantial future scrap-generation opportunities.

1. Impact of CBAM and Gulf Conflict on Aluminum Scrap Generation

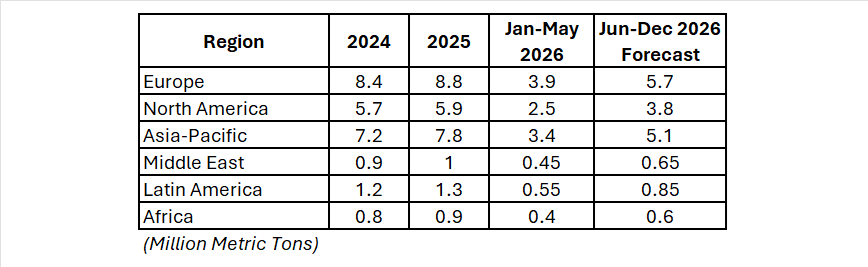

Estimated Additional Aluminum Scrap Availability by Region

Key Impacts

Key Impacts

CBAM Effects

• Increased demand for low-carbon secondary aluminum.

• More recycling investments in Europe.

• Greater exports of processed scrap to Asia.

• Premium pricing for recycled aluminum products.

Gulf Conflict Effects

• Higher freight and insurance costs.

• Supply-chain disruptions through Red Sea routes.

• Increased energy costs affecting smelters.

• Temporary scrap shortages in some importing regions.

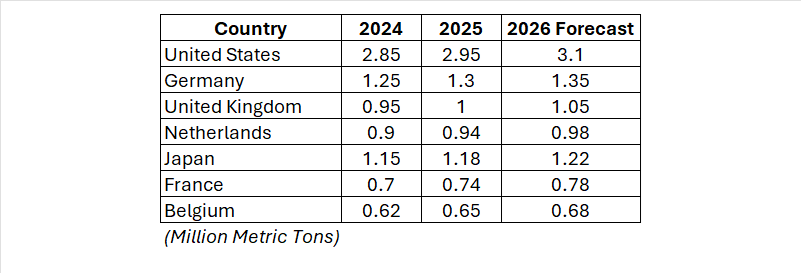

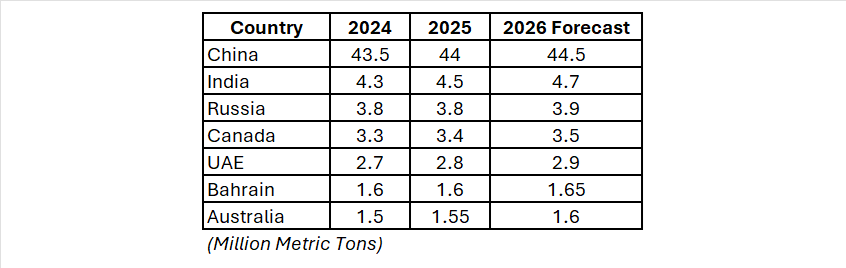

2. Major Aluminum Scrap Exporting Countries

Aluminum Scrap Exports by Major Exporters Major Types of Aluminum Scrap Traded

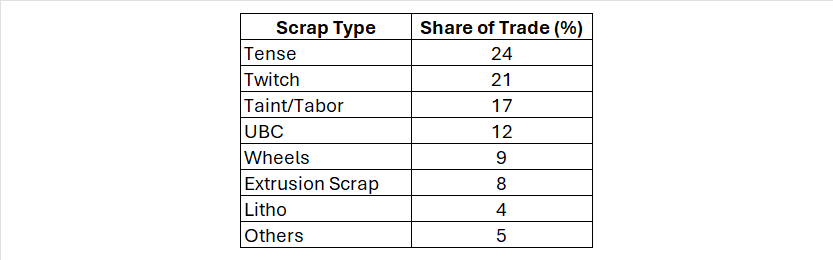

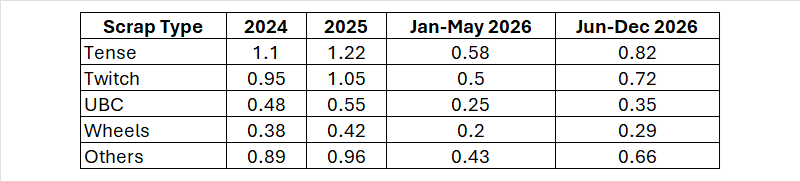

Major Types of Aluminum Scrap Traded

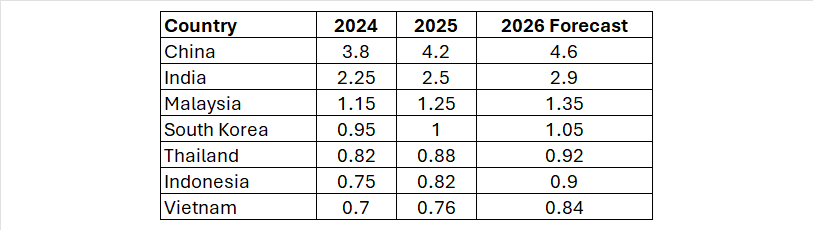

3. Top Aluminum Scrap Importing Countries

3. Top Aluminum Scrap Importing Countries

4. Primary Aluminum Production

Major Producing Countries

5. Availability of Alumina, Bauxite and Coke

5. Availability of Alumina, Bauxite and Coke

Major Sources Price Impact

Price Impact

• Guinea bauxite disruptions increased raw material costs.

• Higher energy prices raised smelting expenses.

• CBAM encouraged recycled aluminum utilization over primary metal.

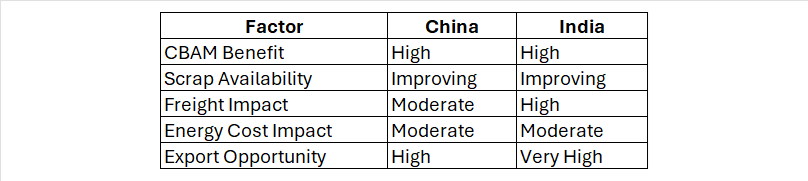

6. Impact on Secondary Aluminum Production in Asia

Secondary Aluminum Production Growth Impact Assessment

Impact Assessment

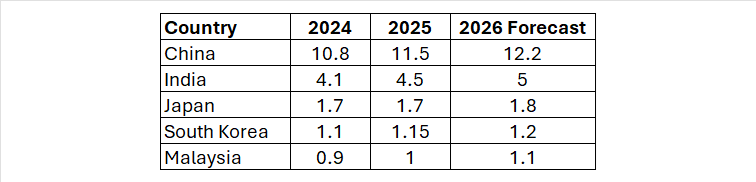

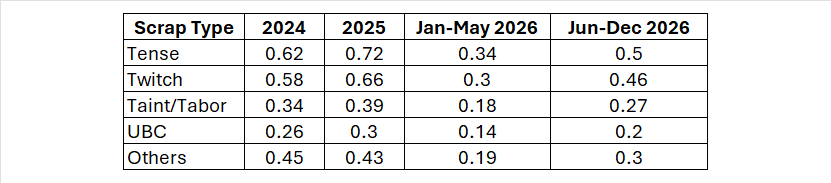

7. Aluminum Scrap Imports by Country and Type

7. Aluminum Scrap Imports by Country and Type

China Imports (Million Metric Tons)

8. India Imports (Million Metric Tons)

8. India Imports (Million Metric Tons)

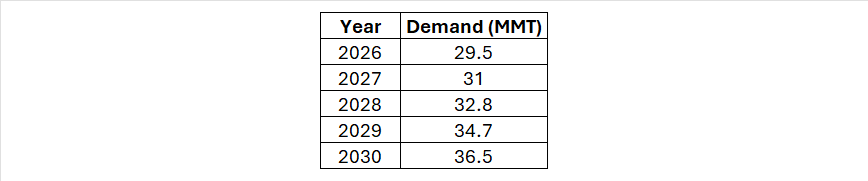

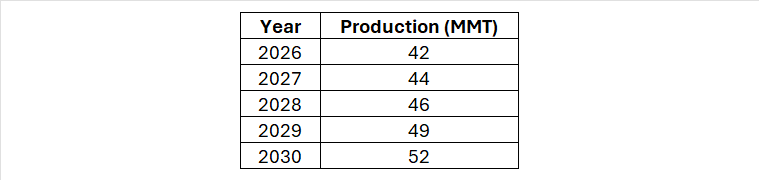

9. Forecast 2026-2030

9. Forecast 2026-2030

Global Aluminum Scrap Demand Forecast Secondary Aluminum Production Forecast

Secondary Aluminum Production Forecast

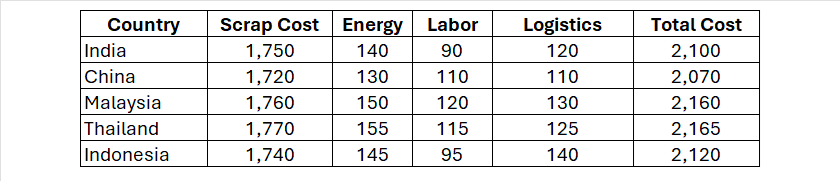

10. Secondary Aluminum Ingot Manufacturing Cost Comparison (2026)

Average Cost ($/Ton)

CBAM Impact

• Additional certification costs.

• Carbon reporting expenses.

• Investment in cleaner melting technologies.

• Increased demand for traceable scrap streams.

Opportunities

• Vehicle recycling.

• Beverage can recycling.

• Construction demolition scrap.

• Export to India, UAE and Europe.

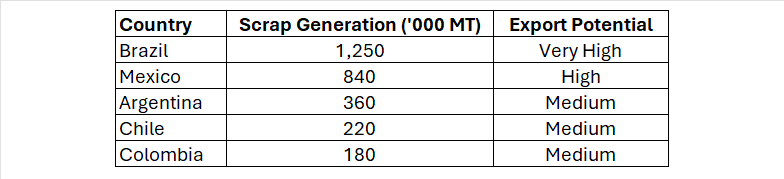

12. Latin America Aluminum Scrap Generation and Export Opportunities

Opportunities

• Automotive scrap.

• Beverage can recovery.

• Industrial manufacturing scrap.

• Growing exports to Asia.

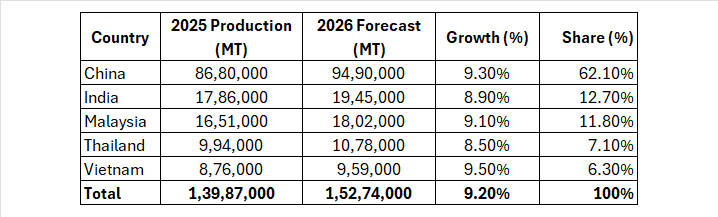

13. Top Secondary Aluminum Ingot Manufacturers in Asia

Top 10 Secondary Aluminum Ingot Manufacturers – Combined Production Comparison

Key Insights

- China remains the dominant producer, accounting for over 62% of total production among these five countries.

- India continues to be the second-largest secondary aluminum ingot producer, driven by growing scrap imports and automotive demand.

- Malaysia has emerged as a major regional recycling and alloy-ingot hub due to strong scrap imports and export-oriented manufacturing.

- Thailand benefits from its large automotive and die-casting industry.

- Vietnam is the fastest-growing market, supported by electronics manufacturing, foreign investment, and increasing exports.

Combined production of the top secondary aluminum ingot manufacturers in these five countries is estimated to increase from 13.99 million MT in 2025 to 15.27 million MT in 2026, representing approximately 9.2% year-on-year growth.

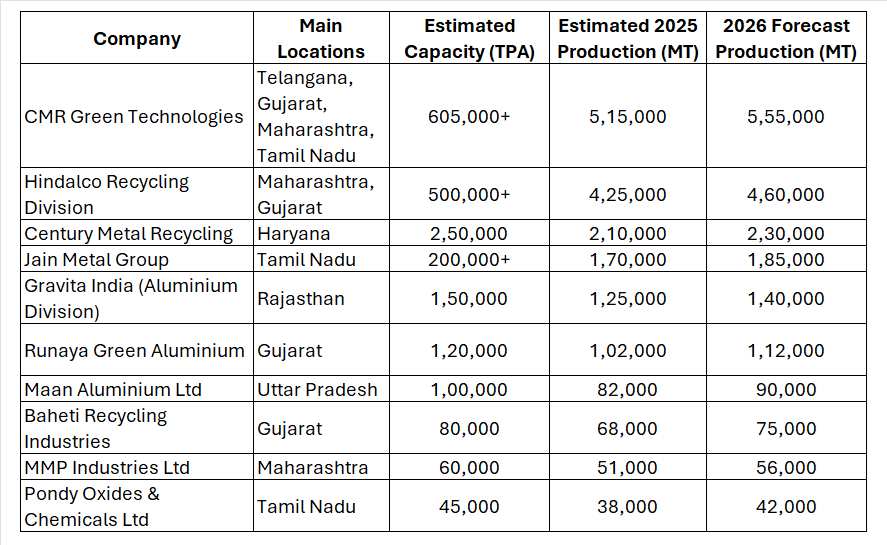

a) Top 10 Secondary Aluminum Ingot Manufacturers in India

Estimated Production in 2025 and 2026 Forecast

India's secondary aluminum industry is expanding rapidly due to growing scrap imports, automotive lightweighting, EV manufacturing, and demand for low-carbon aluminum. CMR Green Technologies is widely recognized as the largest secondary aluminum alloy producer in India, with a combined aluminum and zinc die-casting alloy capacity exceeding 605,000 TPA.

India's secondary aluminum production is expected to grow from approximately 5 million tonnes in 2026 to 6.5–7 million tonnes by 2030, driven by increasing scrap availability, CBAM-related demand for low-carbon materials, and rapid expansion of automotive and EV manufacturing. Companies such as CMR Green Technologies, Hindalco, Century Metal Recycling, Jain Metal Group, and Gravita India are expected to account for a significant share of this growth.

Note: Exact production figures are not publicly disclosed by most private secondary aluminum producers. The 2025 production and 2026 forecast figures above are industry estimates based on installed capacities, utilization rates, company disclosures, market share, and announced expansion plans.

b) Top 10 Secondary Aluminum Alloy Ingot Manufacturers in China

Estimated Production in 2025 & 2026 Forecast

China is the world's largest secondary aluminum producer, with secondary aluminum output expected to exceed 14 million tonnes in 2026 as Beijing promotes recycling and targets over 15 million tonnes of recycled aluminum production by 2027. (Reuters)

The following table represents the major producers of secondary aluminum alloy ingots, recycled aluminum alloys, and remelted aluminum products in China.

Industry China's secondary aluminum industry has become a strategic pillar of its low-carbon metals sector. Secondary aluminum supply exceeded 10 million tonnes several years ago and continues to grow rapidly, supported by increasing domestic scrap availability and recycling investments. (Transition Asia)

Industry China's secondary aluminum industry has become a strategic pillar of its low-carbon metals sector. Secondary aluminum supply exceeded 10 million tonnes several years ago and continues to grow rapidly, supported by increasing domestic scrap availability and recycling investments. (Transition Asia)

Note: China does not publicly disclose secondary aluminum alloy ingot production by company in a standardized format. The 2025 production figures and 2026 forecasts above are industry estimates derived from company capacities, utilization rates, downstream alloy production, recycling investments, and Chinese secondary aluminum market trends. They should be used for market analysis rather than as official company-reported production statistics.

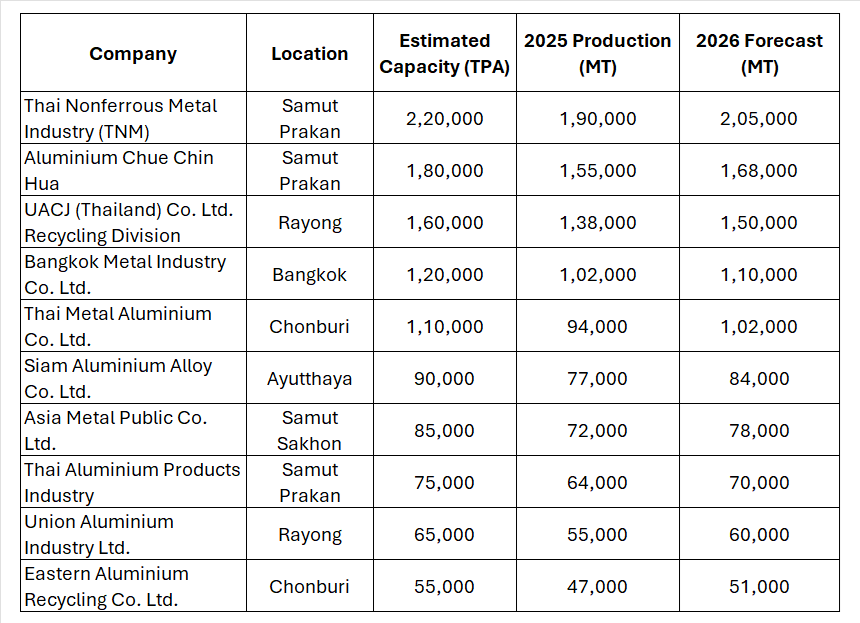

c) Top 10 Secondary Aluminum Alloy Ingot Manufacturers in Thailand

Estimated Production in 2025 & 2026 Forecast

Thailand is Southeast Asia's largest automotive manufacturing hub and one of ASEAN's major consumers of secondary aluminum alloy ingots. Demand is driven by automotive casting, die-casting, electronics, air-conditioners, and export-oriented manufacturing sectors. Most Thai secondary aluminum producers manufacture ADC12, A380, AlSi9Cu3, and customized die-casting alloys.

Top Secondary Aluminum Ingot Producers in Thailand

Thailand is expected to remain one of ASEAN's leading secondary aluminum alloy producers due to its strong automotive sector, Japanese manufacturing presence, and growing EV supply chain investments. The country's recycled aluminum demand is forecast to grow at 5–7% annually through 2030, supported by increasing scrap utilization and regional exports. Secondary aluminum production is becoming increasingly important because recycled aluminum requires about 95% less energy than primary aluminum production.

Thailand is expected to remain one of ASEAN's leading secondary aluminum alloy producers due to its strong automotive sector, Japanese manufacturing presence, and growing EV supply chain investments. The country's recycled aluminum demand is forecast to grow at 5–7% annually through 2030, supported by increasing scrap utilization and regional exports. Secondary aluminum production is becoming increasingly important because recycled aluminum requires about 95% less energy than primary aluminum production.

Note: Thailand does not publish company-wise secondary aluminum alloy ingot production data. The 2025 production figures and 2026 forecasts are industry estimates based on installed capacities, utilization rates, automotive demand, recycling activity, and ASEAN aluminum market trends. They should be used as market intelligence estimates rather than official company-reported production figures.

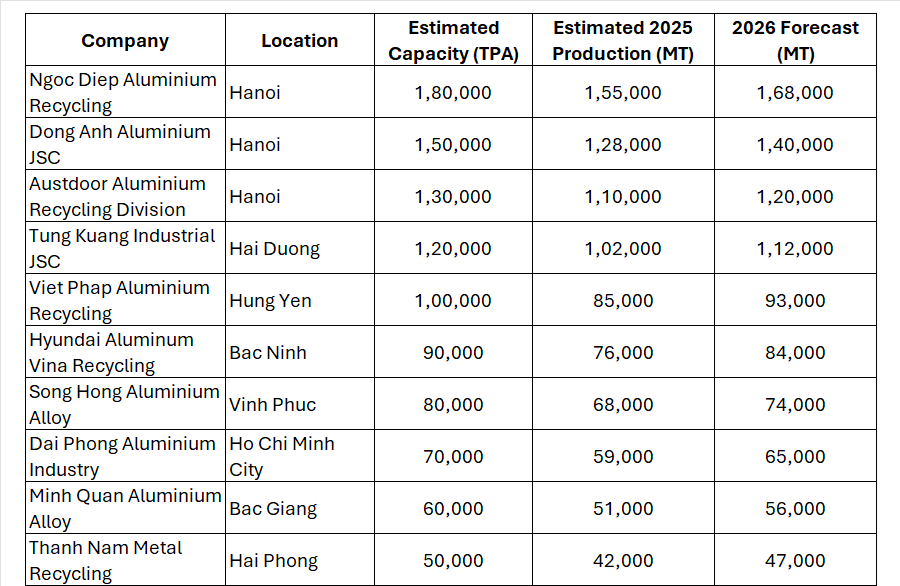

d) Top 10 Secondary Aluminum Alloy Ingot Manufacturers in Vietnam

Estimated Production in 2025 & 2026 Forecast

Vietnam has emerged as one of Southeast Asia's fastest-growing secondary aluminum markets due to strong growth in automotive components, electronics, construction materials, and exports to Japan, South Korea, China, and Europe. Rising imports of aluminum scrap from the United States, Europe, Japan, and Australia are supporting the expansion of secondary alloy ingot production.

Top Secondary Aluminum Ingot Producers in Vietnam

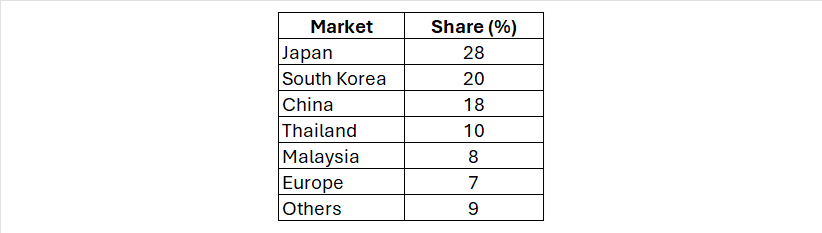

Major Export Markets for Vietnamese Aluminum Alloy Ingots

Industry Assessment

Industry Assessment

Vietnam's secondary aluminum sector is expected to grow at 8–10% annually through 2030, one of the fastest rates in ASEAN. The country benefits from lower labor costs, growing manufacturing investments, increasing aluminum scrap imports, and strong demand from Japanese and Korean automotive suppliers. CBAM implementation in Europe is also encouraging Vietnamese producers to improve traceability and increase recycled content in alloy ingots, creating additional export opportunities.

Note: Vietnam does not publicly publish company-wise secondary aluminum alloy ingot production statistics. The production figures shown above are market-based estimates derived from plant capacities, utilization rates, recycling operations, industry reports, and announced expansion projects. They should be treated as industry forecasts rather than official company-reported production data.

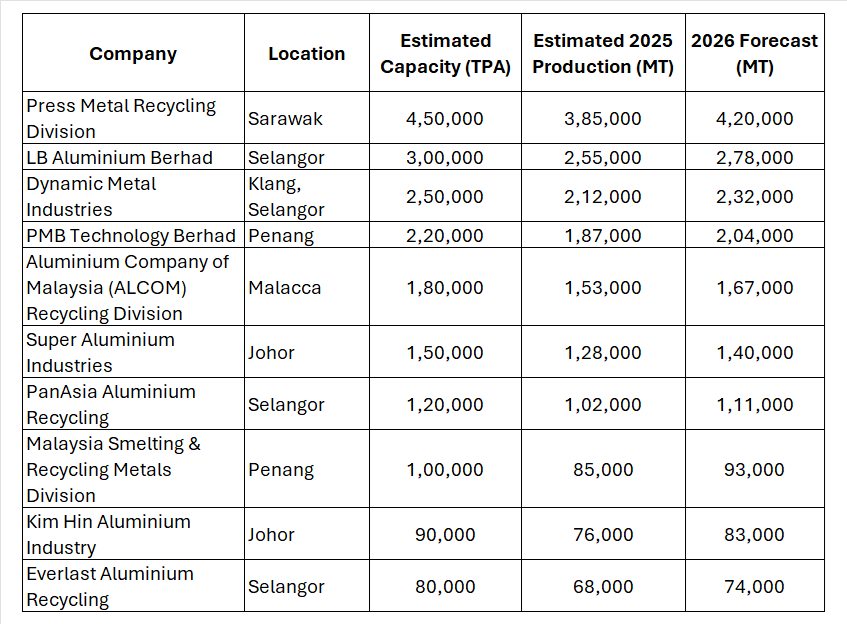

e) Top 10 Secondary Aluminum Alloy Ingot Manufacturers in Malaysia

Estimated Production in 2025 & 2026 Forecast

Malaysia has become one of Southeast Asia's most important secondary aluminum alloy production hubs due to strong scrap imports from the United States, Europe, Japan, Australia, and the Middle East. The country benefits from favorable trade policies, good port infrastructure, and growing demand from automotive, electronics, construction, and export markets.

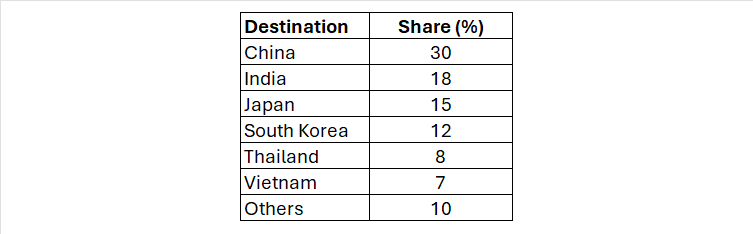

Major Export Destinations

Major Export Destinations

Industry Assessment

Industry Assessment

Malaysia is expected to remain one of Asia's largest importers and processors of aluminum scrap. Secondary aluminum alloy production is projected to grow at 7–9% annually through 2030, supported by increasing scrap imports, expansion of recycling facilities, automotive sector growth, and demand for low-carbon aluminum products driven by CBAM requirements. Malaysia's strategic location and strong export infrastructure position it as a major regional hub for recycled aluminum alloy ingot production serving China, India, Japan, South Korea, and ASEAN markets.

Note: Malaysia does not publish official company-wise secondary aluminum alloy ingot production data. The production figures presented above are market estimates derived from plant capacities, utilization rates, company disclosures, recycling investments, export volumes, and industry growth forecasts. They should be treated as analytical estimates rather than official company-reported statistics.

Conclusion

CBAM and Gulf-region geopolitical tensions are accelerating structural changes in global aluminum markets. Recycled aluminum is becoming increasingly important as governments and manufacturers pursue lower-carbon supply chains. Europe's recycling sector is expected to expand significantly, while India and China will remain the largest growth centers for secondary aluminum production. Despite temporary logistics and energy-cost disruptions caused by Gulf conflicts, long-term demand for aluminum scrap is expected to remain robust through 2030. Africa and Latin America will emerge as important supplementary sources of aluminum scrap, creating new trade opportunities for recyclers, traders, processors, and secondary aluminum producers worldwide.

References

1. International Aluminium Institute – Global aluminum production statistics.

2. World Bureau of Metal Statistics – Global metal production and trade data.

3. International Energy Agency – Energy and industrial decarbonization reports.

4. European Commission – CBAM regulations and implementation framework.

5. Bureau of International Recycling – Scrap trade and recycling market reports.

Note: Several 2026 (Jan–May), Jun–Dec 2026 estimates and 2027–2030 forecasts are analytical market projections based on industry trends, trade flows, recycling growth rates, CBAM implementation effects, and Gulf-region logistics assumptions. They should be treated as forecast scenarios rather than official statistics.

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)