Ferrous Scrap & TMT Price Trends: India & Global

Why Ferrous Scrap & TMT Steel Prices Are Falling in India and Global Markets: Country-wise Analysis, Demand Trends & Outlook (2026)

1. Introduction

Ferrous scrap and TMT (Thermo-Mechanically Treated) steel bars are among the most important raw materials used in steel manufacturing and construction industries worldwide. Their prices directly influence infrastructure projects, manufacturing costs, automobile production, and real estate development. During the past several months, both ferrous scrap and TMT steel prices have declined across India and many international markets. The correction has resulted from slowing construction activities, oversupply of steel, weak manufacturing demand, lower raw material costs, geopolitical uncertainties, seasonal factors, and cautious buying behavior. Understanding these trends helps manufacturers, traders, recyclers, and investors make informed business decisions.

2. Understanding Ferrous Scrap and TMT Steel

Ferrous scrap consists of discarded steel and iron recovered from demolished buildings, vehicles, machinery, railways, ships, manufacturing industries, and fabrication units. It serves as the primary raw material for Electric Arc Furnace (EAF) and Induction Furnace (IF) steel producers.

TMT bars are high-strength reinforcement bars widely used in residential, commercial, industrial, bridge, highway, railway, and infrastructure construction due to their superior tensile strength and corrosion resistance.

Because scrap is the major raw material for secondary steel production, any movement in scrap prices eventually impacts TMT prices.

3. Why Are Ferrous Scrap & TMT Prices Falling in India and Other Countries?

Several global and domestic factors are contributing to the decline.

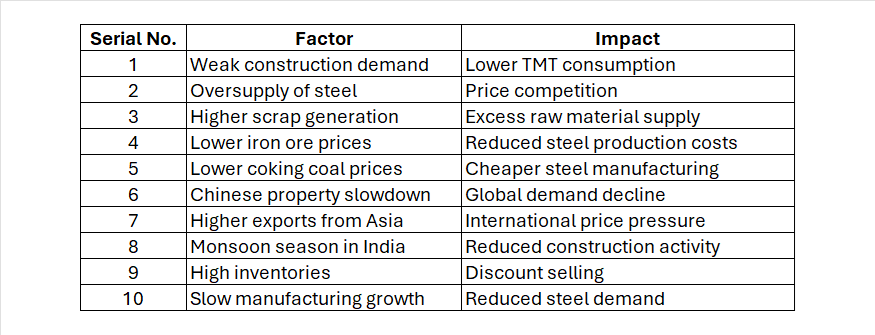

3.1 Weak Construction Demand

Construction activity has slowed in many countries because of:

• Higher interest rates

• Slow real estate sales

• Delayed infrastructure spending

• Rising financing costs

Since construction consumes nearly 55–60% of steel globally, weaker demand directly impacts TMT prices.

3.2 Oversupply of Steel

Many steel mills expanded production capacities during previous years expecting stronger demand.

However,

• Production increased faster than consumption.

• Inventory levels reached multi-year highs.

• Mills began offering discounts.

This created downward pressure on steel prices.

3.3 Declining Iron Ore Prices

Iron ore prices have weakened due to:

• Lower Chinese steel production

• Higher mine production

• Increased inventories

Lower iron ore prices reduce production costs of integrated steel plants.

3.4 Falling Coking Coal Prices

Coking coal is another major steelmaking input.

Lower coal prices reduce:

• Blast furnace production costs

• Finished steel costs

• Market selling prices

3.5 Weak Chinese Steel Consumption

China consumes nearly half of global steel production.

Current challenges include:

• Property market slowdown

• Reduced infrastructure growth

• Lower manufacturing output

• Export-oriented production

Lower Chinese demand affects worldwide steel pricing.

3.6 Higher Steel Exports

Countries facing weak domestic demand increase exports.

Large export volumes from:

• China

• Japan

• South Korea

• Vietnam

increase competition and reduce international prices.

3.7 Increased Scrap Availability

Higher scrap collection from:

• End-of-life vehicles

• Ship recycling

• Demolition projects

• Industrial waste

has increased supply, pushing prices downward.

3.8 Seasonal Monsoon Impact in India

During monsoon:

• Construction slows.

• Infrastructure work reduces.

• Builders postpone purchases.

• Inventory accumulates.

Consequently TMT prices soften.

3.9 High Steel Inventories

Steel distributors continue carrying:

• Higher finished goods inventory

• Unsold TMT

• Unsold structural steel

Inventory liquidation causes aggressive price cuts.

3.10 Global Economic Uncertainty

Economic uncertainty arising from:

• Inflation

• Trade disputes

• Currency fluctuations

• Geopolitical conflicts

reduces industrial investment and steel demand.

4. Major Factors Contributing to Lower Prices

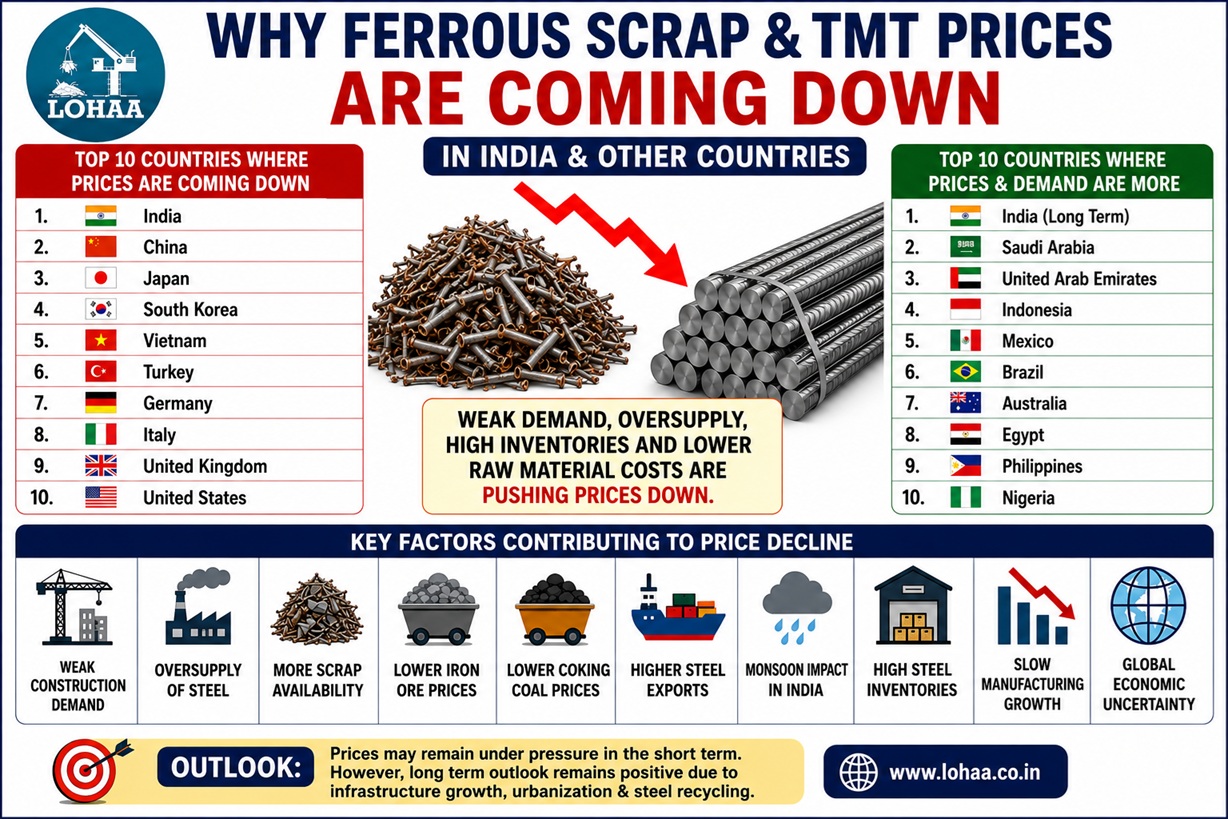

5. Top 10 Countries Where Ferrous Scrap & TMT Prices Are Declining

5. Top 10 Countries Where Ferrous Scrap & TMT Prices Are Declining

Country-wise Reasons

Country-wise Reasons

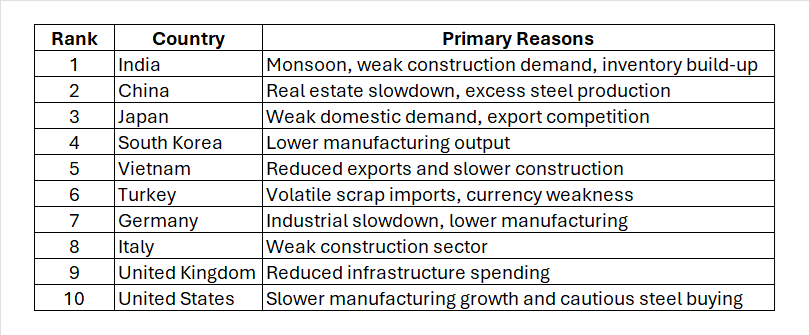

5.1 India

• Monsoon reduces construction.

• Infrastructure buying slows.

• Scrap availability improves.

• Mills reduce prices to clear inventory.

5.2 China

• Housing crisis continues.

• Developers reduce projects.

• Steel demand weakens.

• Mills export surplus steel.

5.3 Japan

• Aging population lowers domestic construction.

• Automotive production moderates.

• Export markets become highly competitive.

5.4 South Korea

Manufacturing slowdown has reduced demand from:

• Shipbuilding

• Machinery

• Construction

5.5 Vietnam

Export-oriented industries have weakened because of slower global trade.

5.6 Turkey

Turkey imports significant volumes of scrap.

Volatile international scrap prices and weaker domestic demand have lowered finished steel prices.

5.7 Germany

Industrial production remains soft.

Lower manufacturing reduces scrap consumption.

5.8 Italy

Construction recovery has slowed, reducing reinforcement steel demand.

5.9 United Kingdom

Higher financing costs continue affecting residential projects.

5.10 United States

Manufacturing remains cautious due to elevated borrowing costs and slower industrial investment.

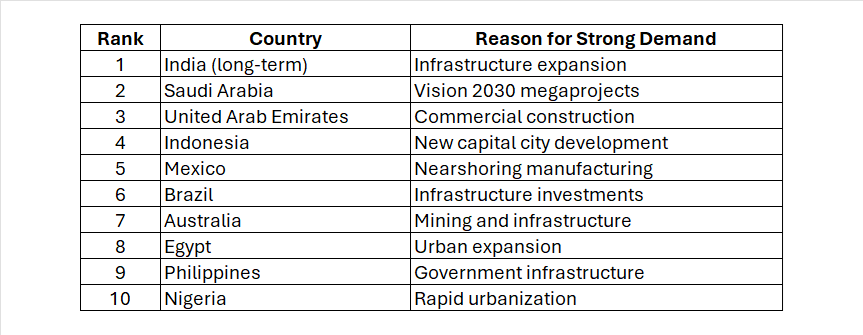

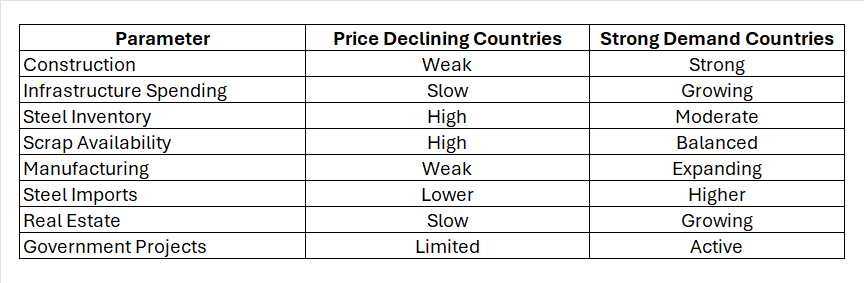

6. Countries Where Ferrous Scrap & Steel Demand Remains Strong

Not every country is experiencing weak demand. Some continue investing heavily in infrastructure and manufacturing. Country-wise Analysis

Country-wise Analysis

6.1 India

Although prices have softened temporarily, long-term demand remains robust because of:

• Highways

• Railways

• Metro projects

• Housing

• Manufacturing investments

6.2 Saudi Arabia

Mega projects including smart cities, tourism infrastructure, industrial zones, and transport networks require enormous steel consumption.

6.3 United Arab Emirates

Commercial buildings, logistics parks, ports, and industrial developments continue driving steel demand.

6.4 Indonesia

Development of the new capital city and industrial parks supports sustained TMT consumption.

6.5 Mexico

Nearshoring of manufacturing from Asia to North America is increasing demand for factories, warehouses, and associated steel products.

6.6 Brazil

Government-backed infrastructure and energy projects continue to support construction steel demand.

6.7 Australia

Mining sector investments and transport infrastructure maintain stable steel consumption.

6.8 Egypt

Rapid urban development and housing projects increase demand for reinforcement steel.

6.9 Philippines

Roads, bridges, airports, and residential construction continue expanding under public infrastructure programs.

6.10 Nigeria

Urbanization, population growth, and industrial expansion create rising long-term steel demand.

7. Comparative Global Market Analysis

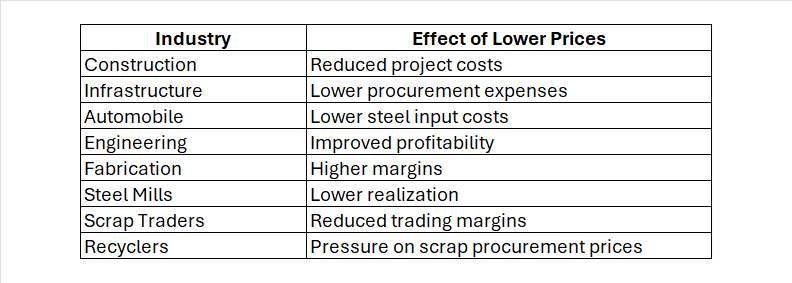

8. Impact on Different Industries

9. Opportunities Created by Lower Prices

Lower ferrous scrap and TMT prices present several opportunities:

• Faster completion of infrastructure projects.

• Reduced construction costs for residential and commercial developers.

• Better procurement opportunities for steel-intensive industries.

• Higher competitiveness for engineering and fabrication companies.

• Improved export potential for downstream steel products due to lower raw material costs.

10. Risks to Watch

Several factors could reverse the current price trend:

• Strong recovery in Chinese construction.

• Large-scale government infrastructure spending.

• Disruptions in scrap supply chains.

• Rising freight costs.

• Higher energy prices.

• Trade restrictions or tariffs on steel imports and exports.

• Geopolitical tensions affecting raw material availability.

11. Market Outlook (2026–2027)

The near-term outlook suggests that ferrous scrap and TMT prices may remain under pressure as long as construction demand stays subdued and inventories remain elevated. Seasonal factors such as the Indian monsoon may continue to weigh on consumption in the short run. However, medium- to long-term prospects remain positive due to accelerating urbanization, infrastructure expansion, renewable energy projects, railway modernization, electric vehicle manufacturing, and industrial investments across emerging economies. Growth in Electric Arc Furnace (EAF) steelmaking and stricter recycling policies are also expected to support sustainable demand for ferrous scrap over the coming years.

12. Conclusion

The decline in ferrous scrap and TMT steel prices is the result of multiple global and regional factors, including weaker construction activity, oversupply, high inventories, slowing industrial production, and softer raw material prices. While countries such as India, China, Japan, and Germany are experiencing downward price pressure, infrastructure-led economies including Saudi Arabia, Indonesia, the UAE, and Mexico continue to support healthy steel demand. Despite current market softness, the long-term outlook for ferrous scrap remains positive as sustainability goals, steel recycling, urbanization, and infrastructure development continue driving demand. Businesses should closely monitor market trends and adopt flexible procurement and inventory strategies.

13. References

1. World Steel Association (worldsteel)

2. Bureau of International Recycling (BIR)

3. OECD Steel Committee Reports

4. International Energy Agency (IEA)

5. International Monetary Fund (IMF)

6. World Bank – Global Economic Prospects

7. BigMint Steel Market Reports

8. Fastmarkets Steel & Scrap Reports

9. S&P Global Commodity Insights

10. Organisation for Economic Co-operation and Development (OECD)

11. National Steel Policy, Government of India

12. Ministry of Steel, Government of India

13. Reserve Bank of India Economic Reports

14. International Rebar Producers and Exporters Association (IREPAS)

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the Lohaa Metal Trading App for Android to access live scrap prices and real-time market updates anytime, anywhere.

Download the Lohaa Metal Trading App for iOS to access live scrap prices and real-time market updates anytime, anywhere.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)