CBAM and India Reshape Ferrous Scrap Trade to 2030

Introduction

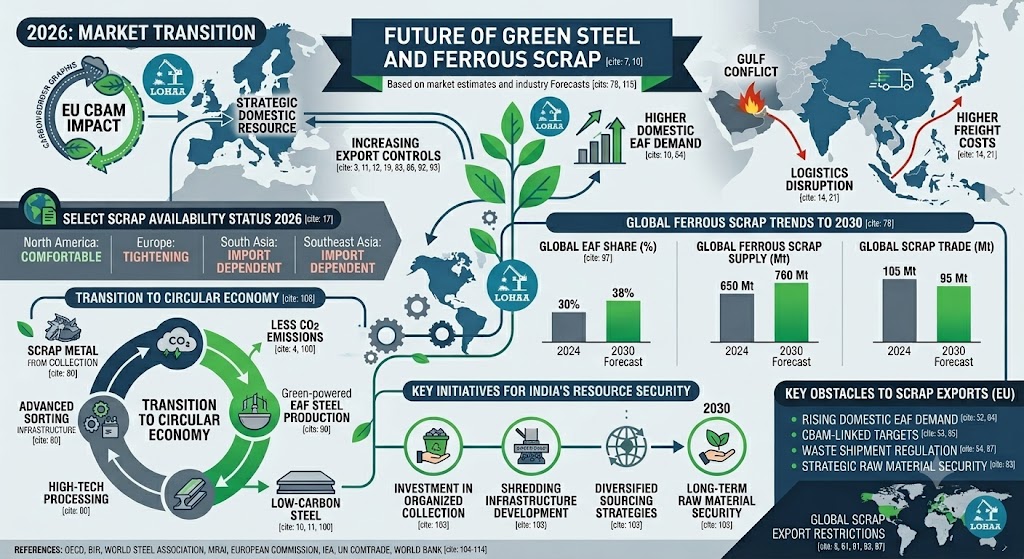

The global ferrous scrap market has entered a strategic phase driven by decarbonization, electric arc furnace (EAF) expansion, resource security concerns, and geopolitical disruptions. The implementation of the European Union's Carbon Border Adjustment Mechanism (CBAM) in 2026 and continuing tensions in the Gulf region have significantly altered scrap trade patterns. Steelmakers worldwide are increasingly dependent on ferrous scrap to reduce carbon emissions, making scrap a critical raw material rather than a waste product. Europe, North America, and parts of Asia are seeking to retain domestic scrap resources to support low-carbon steel production, while emerging steel-producing regions continue to rely heavily on imports. Export restrictions, duties, and outright bans are becoming more common globally, creating tighter supply conditions and greater price volatility. By 2030, global ferrous scrap demand is expected to grow substantially as EAF steel production expands, intensifying competition among consuming nations and reshaping international scrap trade flows.

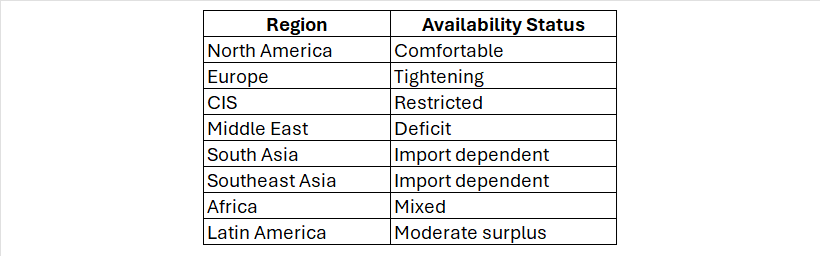

Present Status of Ferrous Scrap Availability After CBAM and Gulf Conflict

Impact of CBAM

The EU's CBAM has accelerated investment in low-carbon steelmaking and EAF capacity. This is increasing domestic demand for ferrous scrap within Europe while reducing the willingness of governments and industry to permit unrestricted exports. Scrap is increasingly viewed as a strategic decarbonization resource. (Le Monde.fr)

Impact of Gulf Conflict

The Gulf conflict has disrupted logistics through the Red Sea and increased freight costs for scrap shipments from Europe and North America to Asia. Import-dependent nations such as India, Bangladesh, Pakistan, and Southeast Asian countries have experienced periodic supply uncertainties and higher procurement costs.

Current Market Condition (2026)

Impact of CBAM

Impact of CBAM

• Growing EAF steel investments across Europe

• Higher domestic scrap consumption

• Increasing pressure to restrict exports

• Scrap increasingly classified as strategic raw material

Impact of Gulf Conflict

• Higher freight and insurance costs

• Red Sea shipping disruptions

• Delayed cargo movements to South Asia

• Greater volatility in import prices

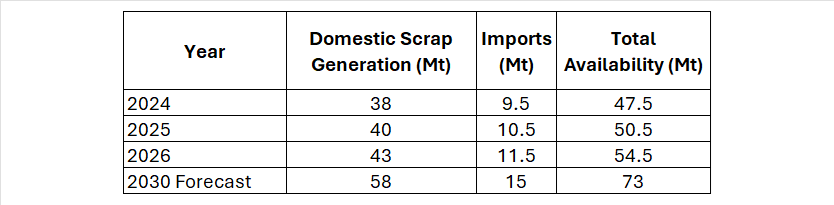

India's Ferrous Scrap Position

Domestic Generation and Import Dependence

India remains one of the world's largest ferrous scrap importers due to:

India remains one of the world's largest ferrous scrap importers due to:

• Rapid steel demand growth

• Expansion of EAF and induction furnace capacity

• Limited organized scrap collection network

• High proportion of obsolete scrap yet to enter recycling streams

India's Constraints in Importing Scrap

1. Export restrictions in supplier countries

2. Freight cost volatility

3. Container shortages

4. Currency fluctuations

5. Quality inconsistencies

6. Competition from Turkey and Southeast Asia

7. Increasing domestic retention policies in Europe

8. Geopolitical disruptions in shipping routes

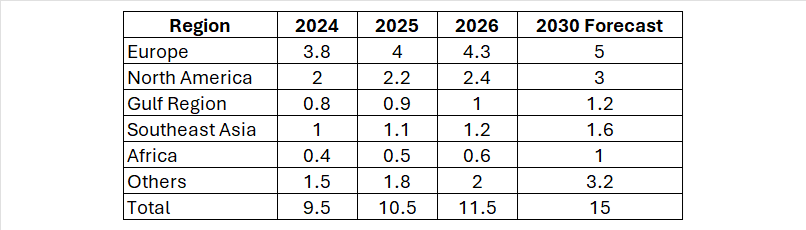

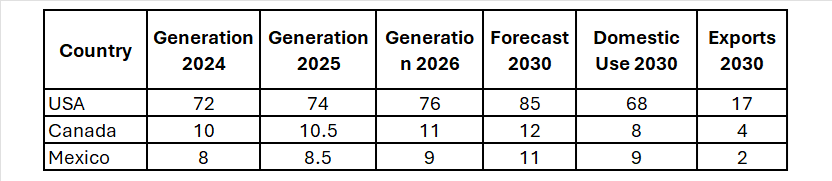

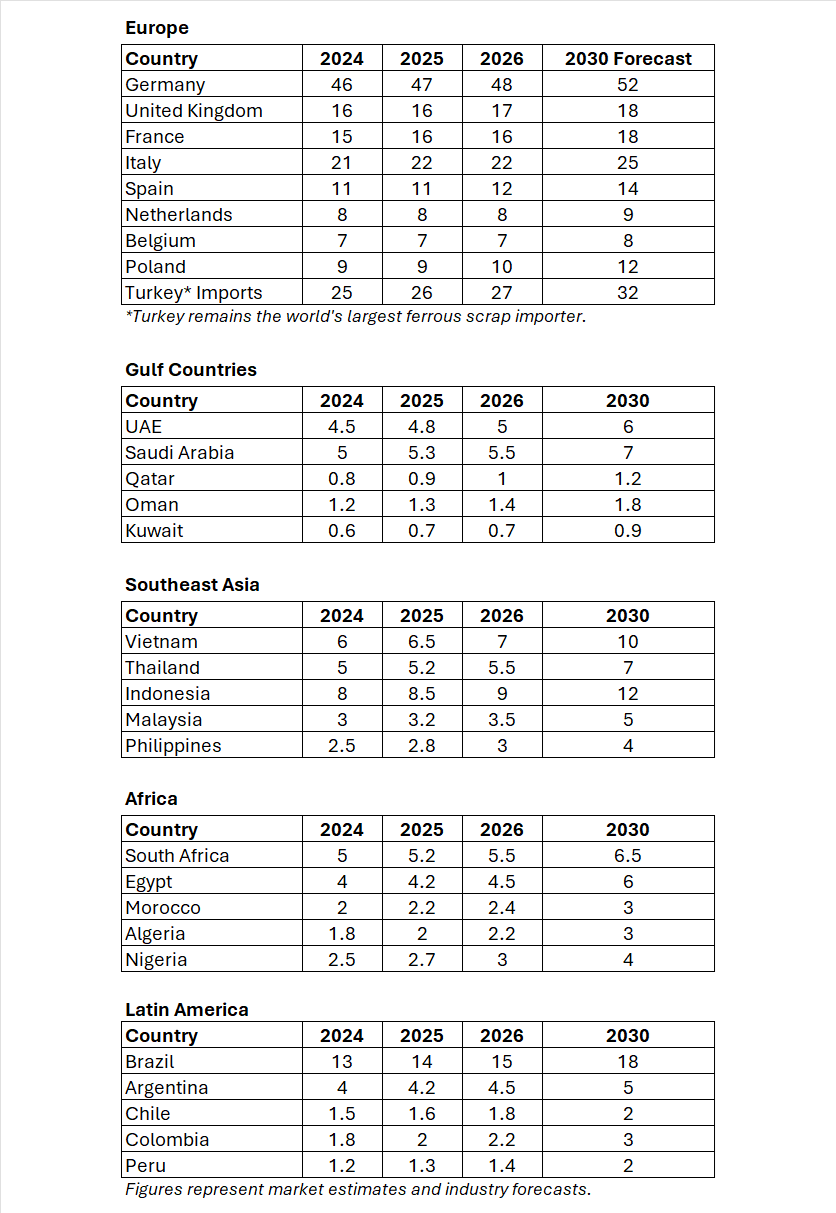

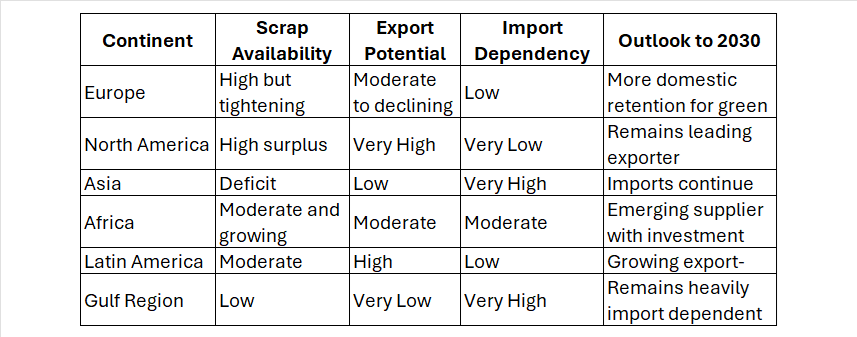

India's Regional Scrap Imports

Major Ferrous Scrap Generating Countries (Million Tons)

North America

Obstacles to Ferrous Scrap Exports from Europe

1. Rising domestic EAF demand

2. CBAM-linked decarbonization targets

3. Waste Shipment Regulation requirements

4. Carbon accounting obligations

5. Political pressure to retain scrap

6. Environmental compliance costs

7. Increasing logistics expenses

8. Strategic raw material security concerns

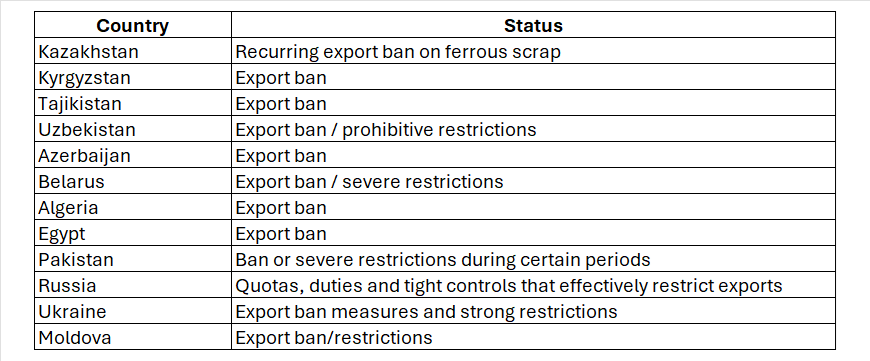

Countries with Full or Near-Full Ferrous (Steel) Scrap Export Bans (2025–2026)

Based on global scrap trade restriction studies, the following countries have implemented full bans or recurring blanket prohibitions on ferrous scrap exports:

Countries with Major Restrictions (Not Complete Bans)

Countries with Major Restrictions (Not Complete Bans)

These countries restrict exports through duties, licensing, quotas, destination controls, or waste shipment regulations rather than outright bans:

- India

- China

- South Africa

- Indonesia

- Malaysia

- Vietnam

- Morocco

- European Union (export authorization and waste shipment controls from 2027)

- United Kingdom (restrictions under discussion)

- Turkey

Global Situation

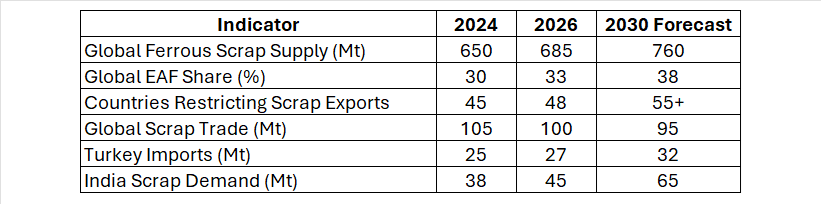

- As of March 2025, 48 countries had introduced 75 ferrous scrap export restrictions.

- Around 38% of these countries imposed partial or complete export bans.

- By 2027, an estimated 76 countries representing 77% of global steel production are expected to have some form of ferrous scrap export barrier.

Regional Overview

Central Asia

- Kazakhstan

- Kyrgyzstan

- Tajikistan

- Uzbekistan

- Azerbaijan

CIS/Eastern Europe

- Belarus

- Russia

- Ukraine

- Moldova

Middle East & North Africa

- Algeria

- Egypt

South Asia

- Pakistan

For a steel scrap market presentation or LOHAA market intelligence report, the most effective classification is:

- Export Ban Countries

- Export Duty Countries

- Quota & Licensing Countries

- Destination-Restricted Countries

Free Export Countries

This approach better reflects actual trade barriers than a simple banned/not-banned list.

Major HMS Exporting Countries with No Ban

The largest suppliers of HMS to the global market remain:

- United States

- United Kingdom

- Netherlands

- Germany

- Japan

- Australia

- Canada

These countries continue to supply most HMS cargoes to import-dependent markets such as Turkey, India, Bangladesh, and Pakistan.

For a market intelligence report, a useful headline would be:

"More than one-third of countries imposing ferrous scrap export restrictions have adopted full or partial bans, tightening global HMS availability and increasing competition among major importing regions."

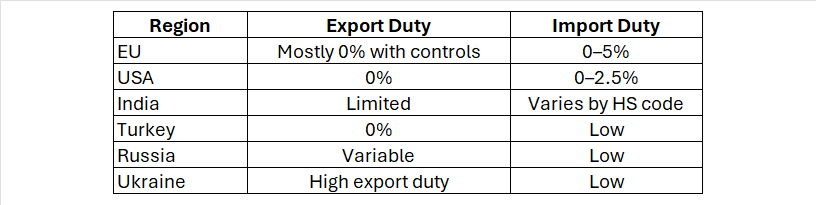

Duty Structure

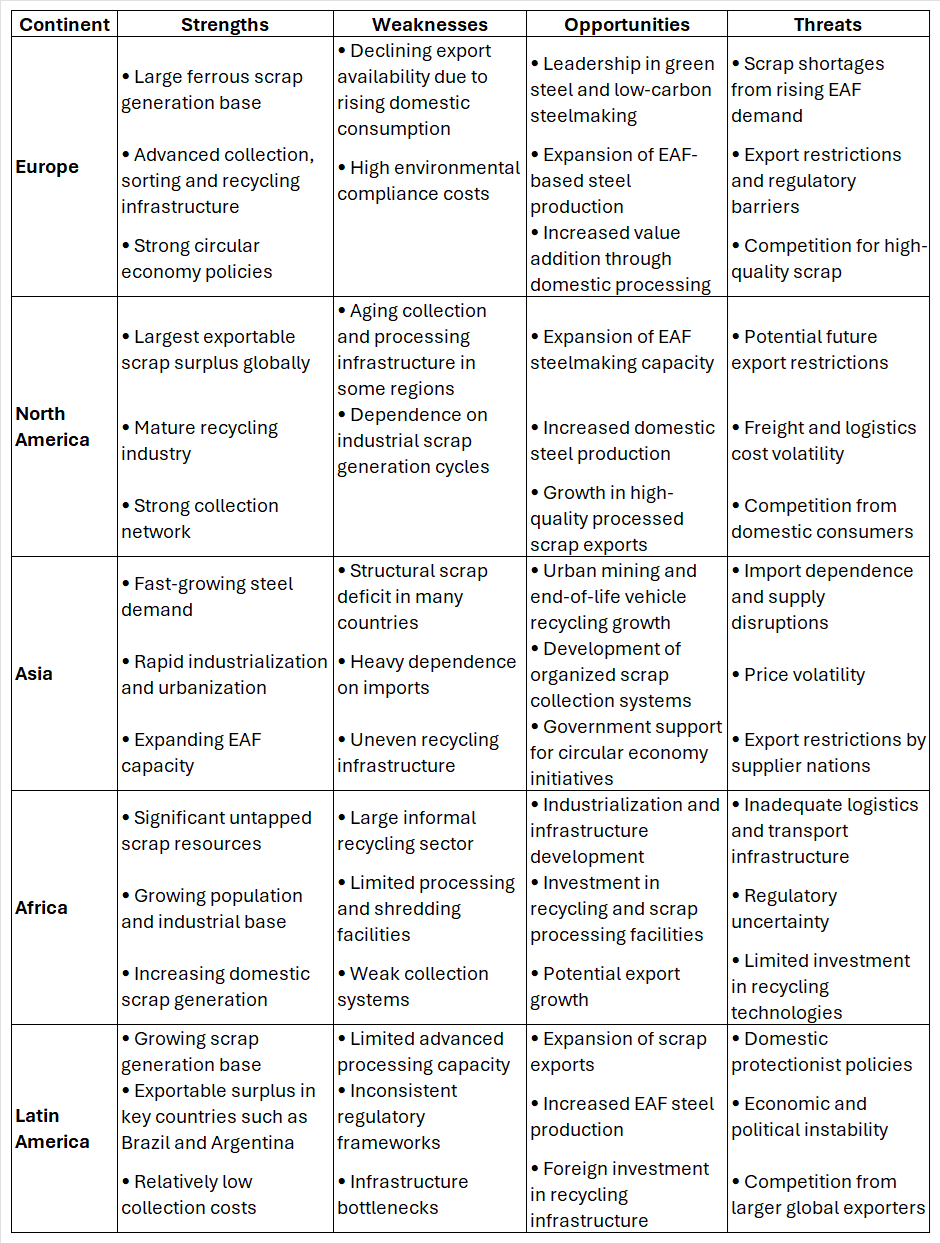

SWOT Analysis

Continental Ferrous Scrap SWOT Summary

Obstacles to Ferrous Scrap Exports from Europe

1. Growing domestic EAF demand.

2. CBAM-driven decarbonization policies.

3. Proposed export monitoring and restrictions.

4. Waste Shipment Regulation compliance.

5. Environmental traceability requirements.

6. Pressure from steelmakers to retain scrap domestically.

7. Increasing logistics costs and vessel shortages.

Key Findings

Conclusion

Ferrous scrap is increasingly becoming a strategic raw material essential for steel decarbonization and resource security. The implementation of CBAM, growth in EAF steelmaking and disruptions caused by Gulf-region conflicts are reshaping global trade patterns. Europe and North America are likely to retain more scrap domestically, while import-dependent regions such as India, Southeast Asia and the Middle East will face stronger competition for supply. India's steel growth ambitions will significantly increase its reliance on both domestic recycling and imported scrap. Investment in organized collection systems, shredding infrastructure, scrap processing and diversified sourcing strategies will be critical for ensuring long-term raw material security through 2030.

References

1. OECD – Export Restrictions on Industrial Raw Materials.

2. Bureau of International Recycling (BIR).

3. World Steel Association.

4. MRAI – Material Recycling Association of India.

5. EUROFER Circular Economy Reports.

6. European Commission CBAM Documentation.

7. International Energy Agency (IEA) Steel Outlook.

8. UN Comtrade Ferrous Scrap Trade Statistics.

9. World Bank Commodity Markets Outlook.

10. National Steel Policy of India.

Note: The country-wise figures are industry estimates and forecast ranges compiled from steel industry datasets, trade statistics, recycling associations, and EAF capacity expansion plans. For a board-level or investor report, I would recommend adding separate tables for Heavy Melting Scrap (HMS 1&2), Shredded Scrap, Bonus Grade Scrap, Busheling, and Stainless Scrap availability by region through 2030.

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)