Indian Metals: FTA Impact, CBAM Risks & Export Strategy

FTAs and Their Impact on Indian Metals Industries — merits, demerits, trends, and regional SWOTs

Quick overview (TL;DR): India’s growing network of free trade agreements (FTAs) and comprehensive economic partnership agreements (CEPAs) is a major opportunity for exporters and downstream consumers in the metals value chain — but it also exposes domestic steel, aluminium, copper and scrap processors to tariff-driven import competition, duty-circumvention, and input-cost imbalances. Smart use of rules-of-origin, targeted safeguards, supportive domestic policy (input duty rationalisation, MSME support, infrastructure), and negotiated industrial cooperation can turn exposure into competitiveness.

Which FTAs/CEPAs matter for Indian metals

- Merits and demerits for the Indian metals sector (by product where relevant);

- Present trends and a table of “feature prosperity” (how FTAs are affecting demand, prices, and investment);

- Regional, SWOT analyses (Middle East/GCC, East Asia, ASEAN, Europe / UK, Americas & Rest);

- Concrete policy / industry recommendations;

Key players and agreements referenced (single entity highlights)

- India — the Indian economy and metals industry.

- United Arab Emirates — India-UAE CEPA partner.

- Japan — India-Japan CEPA partner.

- Republic of Korea — India-Korea CEPA partner.

- Vedanta Group — major Indian metals producer (quoted in news).

- Ministry of Commerce and Industry (India) — negotiator of FTAs/CEPAs.

1. Why FTAs matter for Indian metals — the mechanics

FTAs and CEPAs remove or lower tariffs, streamline customs procedures, and often include trade facilitation, investment, services and regulatory cooperation. For metals, the direct channels are:

a) Tariff removal on finished goods and inputs. Lower or zero tariffs on downstream metal products (e.g., pipes, tubes, finished aluminium extrusions) can open export markets — but can also let cheaper foreign finished goods enter India, competing with domestic producers. At the same time, zero or lower tariffs on raw inputs (e.g., primary aluminium ingots, hot-rolled coil, alloy billets) reduce costs for downstream exporters — but only if rules-of-origin permit.

b) Rules-of-origin (RoO) complexity and circumvention risk. If an FTA allows foreign value-addition (import → processing abroad → re-import) to qualify for preferential treatment, low-tariff finished goods can “fill” the Indian market, undercutting domestic value-add producers. Several studies and policy notes have flagged such duty-structure distortions. (Welcome to CUTS CITEE |)

c) Investment and technology transfer. CEPAs often include investment chapters; they can attract foreign plants, alloy-processing units, and recycling tech into India — positive for job creation and capex.

d) Service/finance/mobility provisions. Easier movement of technical personnel and financial services can help large projects and cross-border supply chains.

(Empirical note: as of late-2025/early-2026 India has actively been expanding its FTA/CEPA network to improve market access and diversify export markets.) (India Briefing)

2. Which FTAs/CEPAs most affect Indian metals — short list and significance

Practical importance (by trade volumes, depth of tariff cuts, industrial linkages):

a) India–United Arab Emirates CEPA (2022) — major hub for re-exports, refining, and metal trade in the Gulf. Significant tariff liberalisation on many product lines; strategic for aluminium, precious metals, and scrap trade. (Mcommerce)

b) India–Japan CEPA (2011; expanded in practice) — strong manufacturing and engineering linkages; Japan is a buyer of certain high-end Indian metal components and a supplier of technology and capital goods. Historical tariff reductions on several steel lines have influenced bilateral trade flows. (RIS)

c) India–Republic of Korea CEPA (2009) — Korea is a major metals manufacturer (steel, aluminium processing) and investor; clauses have at times affected imports of fabricated metal goods. Concerns have been raised about asymmetric tariff schedules benefiting some Korean processors. (Mcommerce)

d) India–ASEAN FTA — ASEAN members are important for scrap flows, semi-finished products, and intermediate goods; tariff liberalisation has boosted both imports and exports in certain lines. (ResearchGate)

e) Recent and emerging deals (Oman, UK, potential EU/UK expansions) — India’s push for more FTAs (e.g., Oman, UK) aims diversification; each new FTA reshapes where metals flow and where investment heads. Recent India-Oman deal (2026) is an example of expanding market access. (AP News)

3. CBAM — Carbon Border Adjustment Mechanism: implications for India’s metals

3. CBAM — Carbon Border Adjustment Mechanism: implications for India’s metals

What is CBAM?

CBAM is the European Union’s carbon border instrument that places a price on embedded emissions for certain carbon-intensive imports (steel, aluminium, cement, fertilisers, electricity, etc.), aimed at avoiding carbon leakage and ensuring a level playing field between EU producers subject to EU ETS and non-EU producers. Importers must report embedded emissions and may pay a charge tied to EU carbon prices. (Taxation and Customs Union)

How CBAM affects Indian metals exporters

- Immediate compliance burden: exporters to the EU (historically a major destination for Indian steel) must monitor, report, and in many cases pay adjustments for emissions intensity. This raises transaction and cost burdens. (Taxation and Customs Union)

- Market price squeeze: CBAM adds to landed cost in the EU; low-margin commodity shipments may become uncompetitive relative to low-carbon foreign suppliers. Recent reporting shows India is actively looking to diversify away from EU exposure because of CBAM. (Reuters)

- Value chain impact: for non-ferrous metals, aluminium is particularly exposed (energy-intensive smelting). Unless smelters can supply low-carbon aluminium or demonstrate credible embedded emissions accounting, EU volumes could shrink. (Taxation and Customs Union)

Measured responses available to India & industry

a) Decarbonize supply — invest in EAFs, renewable electricity for smelting, recycling inputs.

b) Emission accounting & certification — develop transparent, internationally accepted MRV (measurement, reporting, verification) systems so exporters can claim lower CBAM adjustments.

c) Market diversification — deepen FTA use to expand into CBAM-free or less-exposed markets (Middle East, Southeast Asia, Africa), and secure bilateral arrangements that prioritize green transition collaboration. Reports note a strategic pivot to Middle East & Asia to cushion CBAM impact. (Reuters)

d) Negotiation of FTA provisions — incorporate sustainability cooperation, mutual recognition of carbon accounting, or transition support in FTAs/CEPAs.

4. Merits and Demerits for Indian Metals (by product)

Steel

Merits

- Export market access for higher-value steel products (coated coils, automotive grade) as tariffs fall in partner markets.

- Potential for joint ventures and technology transfer (continuous casting, coating, advanced high-strength steels).

Demerits

- Risk of cheap flat and long product imports flooding the domestic market, particularly if partner countries subsidise production.

- Domestic MSME/secondary steel producers face margin squeeze when cheaper finished imports compete with local fabrication.

Aluminium

Merits

- Access to Gulf markets and re-export hubs (UAE) for extrusions and fabricated aluminium goods.

- Opportunity to import high-quality inputs at lower tariff lines to feed Indian downstream manufacturing.

Demerits

- As noted in policy studies, tariff asymmetries can let partners import raw aluminium into India duty-free as finished goods under certain RoO, undermining domestic value-add. This has been observed in some CEPA contexts. (Welcome to CUTS CITEE |)

Copper & Non-ferrous

Merits

- Stronger services and investment provisions can help attract smelter and recycling investments.

- Export opportunities for copper products (wire, tube).

Demerits

- Volatility of global base-metal prices and competition from established exporters (East Asia).

Scrap & Recycling

Merits

- FTAs can make Indian recycling exports more competitive if partners reduce tariffs on scrap and processed secondary raw materials.

- Attracts investment in modern recycling tech.

Demerits

- Import of cheap secondary products can undercut domestic scrap processors unless domestic recycling is upgraded and protected.

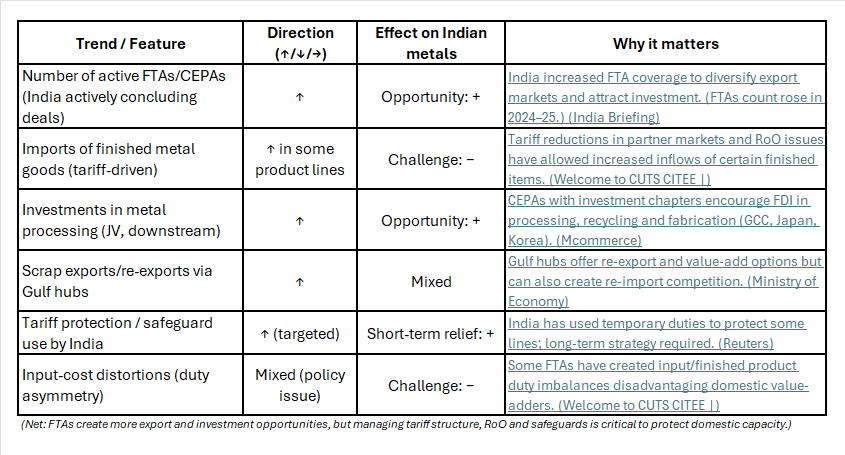

5. Present trends and “feature prosperity” — table

Below is a snapshot table summarising present trends, drivers, and whether they are (net) prosperous or challenging for Indian metals (short-to-medium term: 2024–2026).

6. Regional SWOT analyses (specific to metals) — practical, region-by-region

How to read these SWOTs: each region’s block is concise for business planning — identifying strengths Indian players can leverage, weaknesses to guard against, opportunities to pursue, and threats to mitigate.

A) Middle East & GCC (example: United Arab Emirates, Oman)

Strengths

- Large trade and re-export hubs (Jebel Ali, Dubai) with advanced logistics and warehousing.

- Strong demand for construction and fabrication, plus refining and precious metals markets (aluminium and copper products). (Ministry of Economy)

Weaknesses

- Some GCC partners have highly integrated supply chains and could outcompete Indian fabricators on price/scale.

- Preference for large, reliable suppliers — smaller Indian MSMEs may struggle without scale.

Opportunities

- Use India–UAE CEPA to expand exports of fabricated aluminium and downstream components; leverage UAE as a re-export hub to Africa and Europe. (Mcommerce)

- Develop JV hubs in UAE for value-addition close to end markets.

Threats

- Duty-free inflows of finished goods into India through CEPA channels if RoO are lax could undercut domestic markets.

- Competition from low-cost regional producers.

B) East Asia (Japan, Republic of Korea, Taiwan, China — note India is not in RCEP)

Strengths

- Sophisticated technology providers (Japan & Korea) for smelting, rolling, coating and alloys.

- Strong demand for specialised steel/aluminium components.

Weaknesses

- High-quality competition; capital-intensive producers in East Asia enjoy scale and low per-unit cost.

- Korea/Japan CEPA schedules historically had tariff lines favourable to partner exporters; domestic sectors must meet efficiency benchmarks. (Mcommerce)

Opportunities

- Tech transfer and capex inflows via CEPAs — upgrade mills, downstream finishing and recycling tech.

- Co-production and contract manufacturing for JDM (Japanese design/manufacture) components.

Threats

- Imports of cheap processed inputs or finished goods from East Asia can displace Indian product lines, especially where Indian input duties are higher than partner countries’ duties on finished goods (duty asymmetry). (Welcome to CUTS CITEE |)

C) ASEAN (Indonesia, Vietnam, Thailand, Malaysia, Singapore)

Strengths

- Regional proximity reduces logistics costs; established trade routes for scrap and semi-finished goods.

- ASEAN members often have complementary demand (construction, automobile components).

Weaknesses

- Some ASEAN producers offer lower-cost intermediate goods; product-level competition can be intense.

Opportunities

- Regional value chains for components — India can export semi-finished products and import specific alloy inputs.

- Joint investments in recycling and secondary processing.

Threats

- Tariff liberalisation may encourage import of finished items that reduce domestic fabrication demand. (ResearchGate)

D) Europe & United Kingdom

Strengths

- High technology demand, standards and premium markets for high-spec alloys and engineering metals.

Weaknesses

- Stringent standards and certifications (CE marking, EU ecolabels) can be barriers for smaller Indian firms.

Opportunities

- If future India-EU or India-UK arrangements progress, Indian exporters could gain preferential access for engineered metal products and components.

- Attract EU investments in green metallurgy (decarbonisation tech). (AP News)

Threats

- Competition from established European suppliers on quality and proximity to EU markets.

E) Americas (United States, Canada, Latin America)

Strengths

- Large end markets, high demand for quality steel and non-ferrous products in certain niches (auto, aerospace).

Weaknesses

- Protectionist moves (e.g., recent U.S. aluminium tariff increases) can reduce Indian access and create global price shocks. (Reuters)

Opportunities

- Diversify exports to Latin American markets via CEPAs with GCC/UK partners acting as intermediaries.

- Target niche products less affected by tariffs (e.g., specialty alloys, engineering components).

Threats

- Tariff shocks (external to India’s control) can reduce commodity prices and harm exporters’ margins.

7) Strategic policy and industry recommendations (practical steps)

a) Rationalise input tariffs to remove distortions. If FTAs give partners duty benefits on finished goods while India keeps higher duties on inputs, domestic value addition suffers. India should align input tariff schedules or create targeted drawback/scheme support for downstream processors. (This aligns with policy analysis in trade papers.) (Welcome to CUTS CITEE |)

b) Tighten and clarify rules-of-origin (RoO). Ensure RoO require meaningful value-addition in partner countries to access preferences, reducing duty-circumvention.

c) Use targeted safeguards and anti-dumping tools swiftly. For sudden import surges, temporary duties and safeguards protect critical domestic capacities while firms upgrade.

d) Negotiate investment and co-production chapters. Use CEPAs to lock in technology transfer clauses (training, local procurement, JV requirements).

e) Support MSME modernisation. Provide capital and technical assistance for small rolling mills and fabricators to meet standards and compete on quality.

f) Promote “green” metallurgy cooperation. Prioritise FTAs that include cooperation on decarbonisation and low-emission steel/aluminium production — positioning Indian producers for premium markets.

g) Develop re-export and value-addition hubs. Leverage partners like UAE as logistics and processing hubs for accessing Africa and Europe.

8. Two actionable business playbooks for industry players

a) For a mid-sized aluminium extruder in Gujarat

- Strategy: Use India-UAE CEPA to set up a small office in UAE and a bonded logistics arrangement to supply GCC and East Africa. Negotiate supply contracts with UAE distributors. Use RoO-compliant input sourcing to preserve margins. (Mcommerce)

b) For an integrated steel SME in Eastern India

- Strategy: Invest in one finishing line (galvanizing/painting) to move up the value chain. Seek matching grants under industrial clusters, and use safeguard data to lobby for temporary relief if faced with sudden import surges.

9. Common pitfalls & how to avoid them

a) Pitfall: Treating FTAs as automatic market wins.

Fix: Conduct HS-code level analysis, check partner tariff lines, and verify RoO before pricing bids.

b) Pitfall: Ignoring hidden logistics costs (rules, testing & certification).

Fix: Budget for testing, certification and partner distribution costs.

c) Pitfall: Over-reliance on single export hub or partner.

Fix: Diversify markets (use India’s FTA network) and hedge prices.

10. SWOT summary (India’s metals sector, aggregated)

Strengths

- Rising domestic demand (infrastructure, construction, EV and renewables).

- Large installed base and recent capacity investments.

- Improved market access through FTAs/CEPAs and growing global diplomatic momentum for new deals. (India Briefing)

Weaknesses

- Input-cost distortion from asymmetric tariff schedules.

- Technology gaps in downstream finishing and recycling for some MSMEs.

- Occasional policy lags in safeguard action.

Opportunities

- Export growth to Gulf, ASEAN, Japan/Korea; incoming FTAs (Oman/UK/etc.) widen markets.

- Investment and technology transfer via CEPAs; green metallurgy export potential. (AP News)

Threats

- Global tariff moves (e.g., U.S. aluminium tariff increases) and commodity price swings. (Reuters)

- Duty-driven import surges that undermine domestic value addition.

11. Appendix — Practical checklist for companies (10-point)

i) Map your HS codes to partner FTA tariff schedules.

ii) Verify RoO and certificates required for preferential access.

iii) Estimate logistics & non-tariff costs (testing, certification).

iv) Identify where tariff mismatches hurt your inputs.

v) Consider bonded warehouse or re-export via CEPA partner hubs.

vi) Evaluate JV or licensing deals for tech transfer.

vii) Build a short-term contingency plan for safeguard filings.

viii) Upgrade quality certification (ISO, EN, ASTM) for premium markets.

ix) Seek focussed government schemes for MSME capex support.

x) Monitor geopolitics and tariff changes in the US/EU/GCC (they materially affect price and demand). (Reuters)

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

12. References (sources / further reading)

Below are the main sources I used for claims and recent facts (selection of the most relevant):

- India's Free Trade Agreements: Updates in 2025 — India Briefing (overview of India’s active FTAs/CEPAs and updates). (India Briefing)

- India–UAE CEPA (official / TPCI briefing) — Government documents summarising tariff coverage and trade facilitation (India–UAE CEPA). (Mcommerce)

- CUTS / policy brief on aluminium tariff distortions — analysis of input/finished goods duty asymmetry and impacts on India’s aluminium ecosystem. (Welcome to CUTS CITEE |)

- India–Japan CEPA appraisal (RIS/Oxford Academic) — historical appraisal of CEPA effects on trade and industry. (RIS)

- India–Korea CEPA (official text) — treaty text and tariff schedules (useful for HS-level RoO and tariff checking). (Mcommerce)

- Recent news: India–Oman agreement & India FTA push (AP News) — reporting on recent CEPA/FTA developments (2026). (AP News)

- Reuters coverage (Vedanta on U.S. tariffs) — example of external tariff shocks and industry reaction. (Reuters)