Indian Aluminum Ingots 2026: Market & SWOT Analysis

Introduction

India’s aluminium industry is undergoing a structural transformation, driven by rising demand from automotive, infrastructure, and renewable energy sectors. At the heart of this shift lies the secondary aluminium ecosystem, where aluminium scrap is recycled into value-added products like alloy ingots. These alloy ingots—particularly grades such as ADC12 and LM series—form the backbone of India’s die-casting and engineering industries.

Across the country, aluminium alloy ingot manufacturing is highly regionalized, with strong clusters in states like Gujarat, Haryana (NCR), Maharashtra, and Tamil Nadu. These regions host a mix of large organized players and hundreds of small and medium enterprises (SMEs), many operating in the 400–500 tons per month range. Together, they create a dynamic yet fragmented supply chain that depends heavily on imported aluminium scrap.

In recent times, global disruptions—including the ongoing tensions in the Gulf region—have added a new layer of complexity to this market. Supply chain bottlenecks, rising freight costs, and volatile scrap availability are reshaping pricing trends and trade flows. At the same time, these challenges are opening up new export opportunities for Indian alloy producers, especially in high-demand automotive grades.

This blog provides a comprehensive, state-wise analysis of aluminium alloy ingot manufacturers in India, covering their capacities, key alloy grades, regional strengths, and market dynamics. It also explores how global factors are influencing domestic production and why India’s recycling-driven aluminium sector is poised to play a critical role in the future of sustainable manufacturing.

Primary Aluminium Producers (Indirect Alloy Supply via Remelting)

| Company | Type | Capacity |

| Vedanta Aluminum | Primary | ~2.40 - 3.0 Million Tons |

| Hindalco Industries Ltd | Primary | ~1.30 + Million Tons |

| National Aluminum Company Ltd | Primary | ~460,000 + tons |

| Bharat Aluminum Company Ltd | Primary | ~570,000 tons |

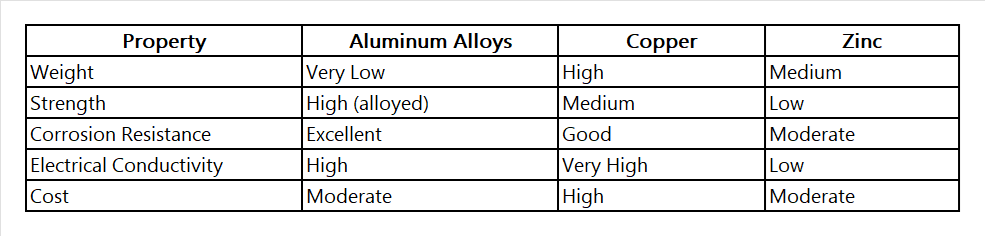

Importance of Aluminum Alloys vs Other Non-Ferrous Metals

Key Advantage:

Key Advantage:

Aluminum offers the best balance of lightweight, strength, and corrosion resistance, making it ideal for modern industries.

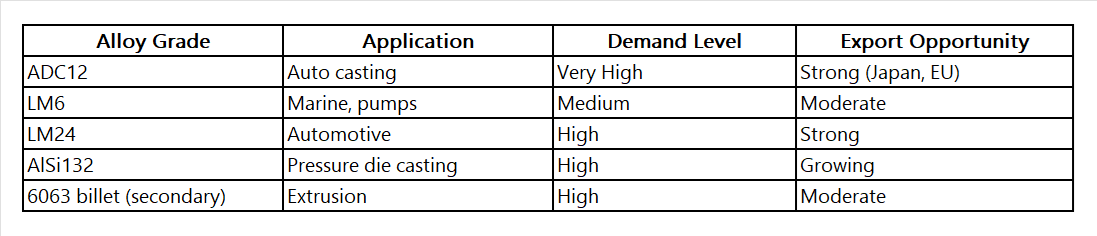

ALUMINIUM ALLOY GRADES – PRODUCTION & EXPORT OPPORTUNITY

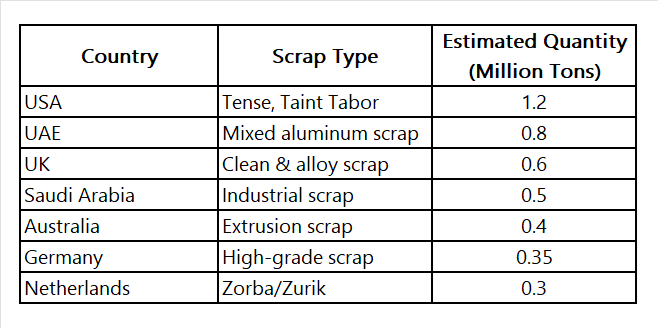

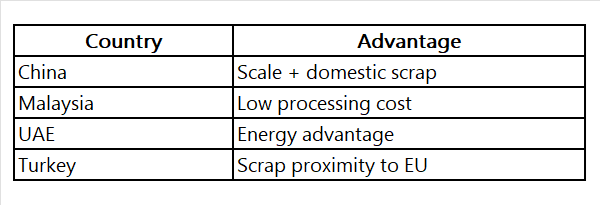

Major Scrap Exporting Countries to India (2025)

Major Scrap Exporting Countries to India (2025)

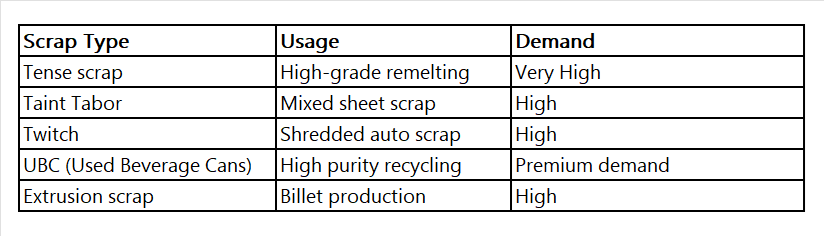

TYPES OF ALUMINIUM SCRAP IMPORTED INTO INDIA

WHICH COUNTRIES ARE CHEAPER THAN INDIA?

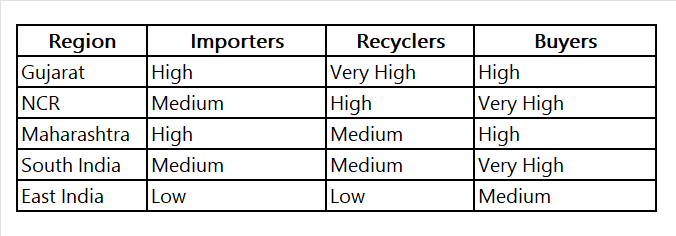

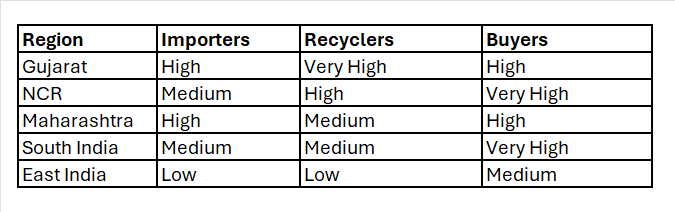

REGION-WISE DATABASE SUMMARY

Present Status of Aluminum Secondary Ingots (2026)

• India produces ~55–60% of its aluminum ingots via secondary (recycled) routes

• Domestic scrap availability remains limited (~30–35%), heavily dependent on imports

• Import dependency: 65–70% of aluminum scrap

• Key consuming sectors:

o Automotive (45%)

o Electrical (20%)

o Construction (15%)

o Packaging & others (20%)

Key Challenges:

• Scrap price volatility

• Import regulations & logistics

• Quality inconsistency in scrap

INDUSTRY SUMMARY

India Secondary Aluminium Alloy Sector

• Total industry size: ~3.5–4.5 million TPA (estimated)

• Organized players share: ~35–40%

• Unorganized SME sector: Highly fragmented (~60%)

Key Observations

• CMR Green Technologies Ltd. dominates alloy ingots (ADC12, LM series)

• Gujarat = largest cluster (Ahmedabad, Bhavnagar, Sanand)

• NCR = largest scrap processing hub

• South India = auto-driven alloy demand

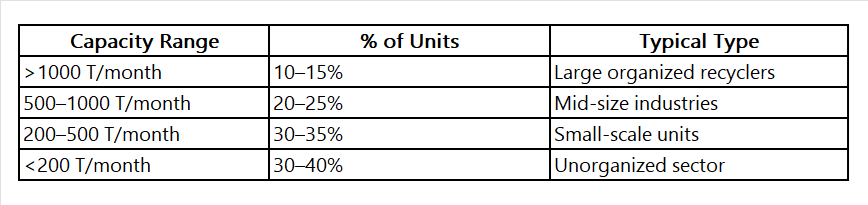

Capacity Segmentation (Pan-India)

KEY INSIGHT FOR LOHAA

• India’s alloy ingot sector is scrap-driven (import dependent)

• Capacity exists, but raw material supply is the bottleneck

• Large players expanding aggressively due to:

o EV demand

o Auto casting growth

o Export opportunities (Japan, EU)

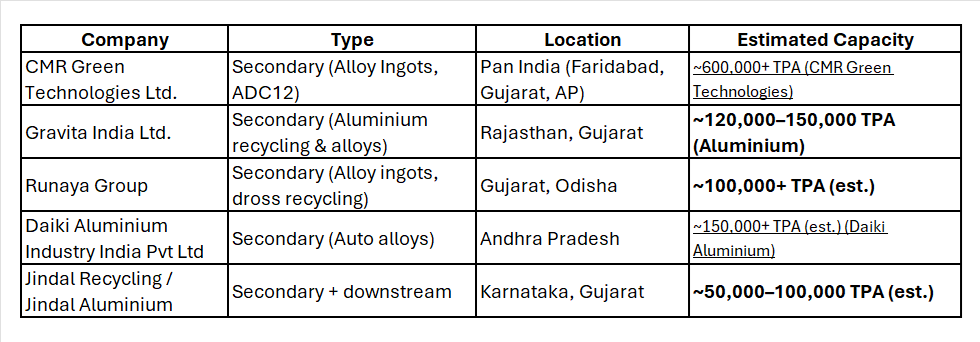

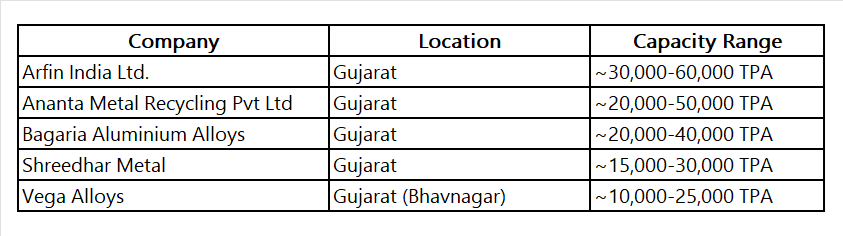

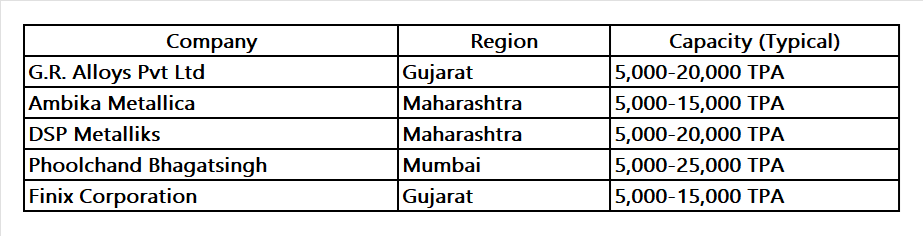

Top Aluminium Alloy Ingot Manufacturers in India (with Capacity)

Large Organized Secondary Aluminium Players

Mid-Sized Secondary Alloy Ingot Manufacturers (Cluster Leaders)

Regional / SME Alloy Ingot Producers (High Fragmentation Sector)

Here is a focused, ground-level dataset of Indian secondary aluminium alloy ingot manufacturers operating in the 400–500 tons/month scrap consumption range (≈5,000–6,000 TPA plants). These are typically SME / cluster-based recyclers, which form the backbone of India’s alloy ingot ecosystem.

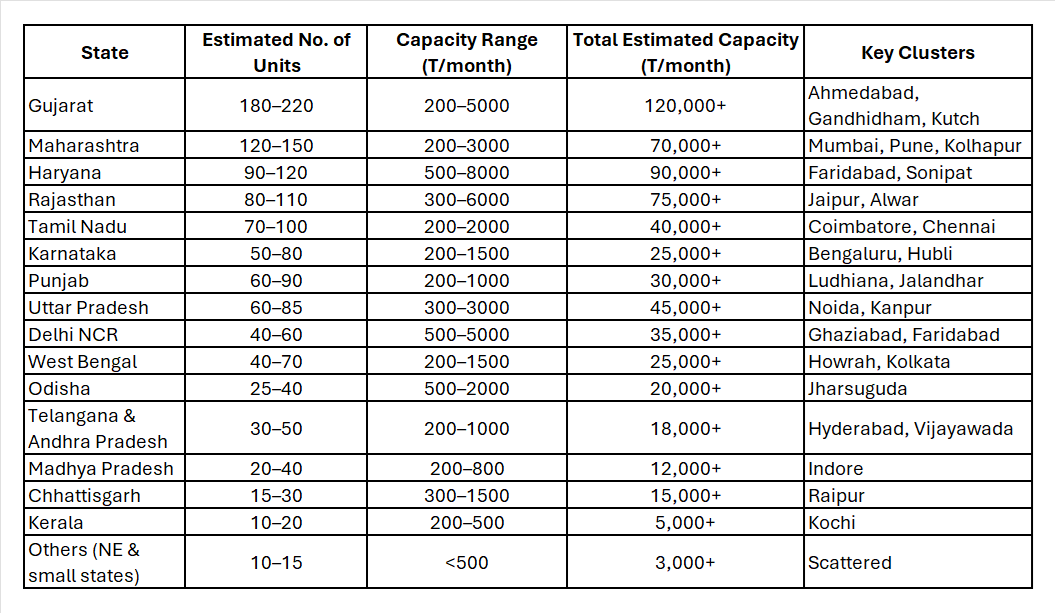

State-wise Aluminum Ingot Manufacturing Units & Capacity (2026)

WHAT THESE 400–500 T UNITS PRODUCE

High-volume alloys:

• ADC12 (auto casting)

• LM6 (pump, marine)

• LM24 (pressure die casting)

Raw material mix:

• Tense scrap

• Taint Tabor

• Twitch (auto shred)

• Local scrap

Secondary ingots are cost-effective and energy-efficient vs primary aluminium

ADC12 BUYER–SELLER NETWORK (INDIA – PRACTICAL FLOW)

Supply Chain Structure

Scrap Supplier → Alloy Ingot Manufacturer → Trader / Stockist → Die Casting Units → OEMs / Exporters

Most 400–500 T/month plants DO NOT sell directly to OEMs

They sell through traders or Tier-2 die casters

1. SELLERS (ALLOY INGOT MANUFACTURERS)

SME Manufacturers (Your Target Segment)

• Gujarat: Bhavnagar, Ahmedabad

• NCR: Faridabad, Bahadurgarh

• Maharashtra: Kolhapur, Pune

• Tamil Nadu: Coimbatore

Produce:

• ADC12 (60–70%)

• LM6 / LM24

Sell in:

• 5–25 ton lots

• Mostly credit-based (15–45 days)

2. KEY BUYER SEGMENTS (WHO BUYS ADC12)

A. DIE CASTING COMPANIES (BIGGEST BUYERS)

Role:

• Convert ADC12 → auto components

Examples (Industry Type):

• Auto component manufacturers

• Casting clusters in:

o Pune

o Chennai

o NCR

o Coimbatore

Evidence:

• India has large demand for aluminium die casting parts buyers across regions

B. AUTO COMPONENT OEM SUPPLIERS (TIER-1 / TIER-2)

They supply to:

• Maruti Suzuki vendors

• Tata Motors vendors

• Hyundai suppliers

• Other Automobile manufacturers

They buy ADC12 regularly in bulk

C. ENGINEERING & INDUSTRIAL CASTING UNITS

• Pump manufacturers

• Electrical housing manufacturers

• Lighting & appliance sector

ADC12 widely used for:

• Pressure die casting components

D. EXPORT TRADERS (VERY IMPORTANT)

Locations:

• Mumbai

• Gujarat

• Delhi

Example:

• Exporters placing 500-ton monthly orders

Export markets:

• Japan

• Italy

• Turkey

• Southeast Asia

E. STOCKISTS / TRADERS (MARKET MAKERS)

Role:

• Buy from SMEs

• Supply to multiple small die casters

Locations:

• Delhi (Kundewalan market)

• Ahmedabad

• Mumbai

They handle:

• Price discovery

• Credit risk

• Inventory

Example:

• Multiple dealers supplying ADC12 ingots across India (Justdial)

3. REGION-WISE BUYER–SELLER NETWORK

Gujarat (Largest Trading Hub)

Flow:

SME → Trader → Exporter

Strong export linkage

NCR (Delhi–Faridabad)

Flow:

SME → Trader → Auto vendors

Highest liquidity market

_

Maharashtra (Pune–Kolhapur)

Flow:

SME → Die caster → OEM

Direct consumption hub

South India (Chennai–Coimbatore)

Flow:

SME → Tier-1 supplier → OEM

High-quality alloy demand

4. KEY MARKET INSIGHTS (VERY IMPORTANT)

A. Traders control pricing

• SMEs depend on traders for liquidity

• Traders decide daily spread (?5–15/kg margin)

B. Die casters drive demand

• Auto sector = largest consumer of ADC12

• Demand fluctuates with:

o Auto sales

o Export orders

C Export market rising

• Due to:

o China supply constraints

o Gulf disruption

Indian ADC12 becoming globally competitive

5. WHERE LOHAA PLATFORM FITS (STRATEGIC INSIGHT)

Current problem:

• Fragmented buyers

• No price transparency

• Credit risk

Opportunity:

• Direct SME ↔ buyer connection

• Real-time pricing

• Scrap-to-ingot integration

FINAL TAKEAWAY

ADC12 market in India is:

• Buyer-driven (die casting industry)

• Trader-controlled (pricing & liquidity)

• Fragmented but high-volume

The real power chain:

Scrap → SME → Trader → Die caster → OEM

REGION-WISE DATABASE SUMMARY

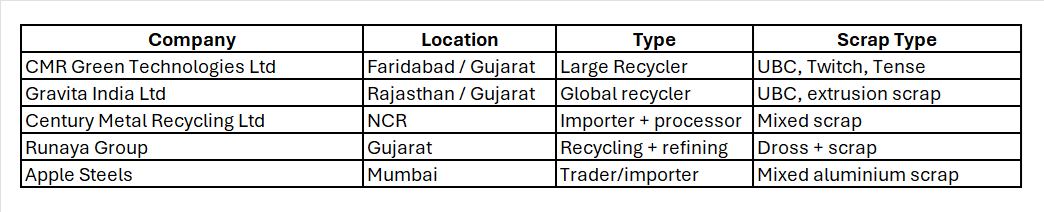

ALUMINIUM SCRAP IMPORTERS (HIGH-VOLUME BUYERS)

India has 2,500+ verified aluminium scrap importers with active shipments

Key Importers (Verified + Active)

KEY INSIGHTS (VERY IMPORTANT)

1. Gujarat = Price Benchmark Market

• Largest scrap consumption

• Highest number of SME alloy units

2. NCR = Volume + Liquidity Hub

• Dominated by large players like CMR

• Strong trader network

3. South India = Quality Demand Hub

• Driven by auto OEM supply chain

• Higher specification alloys

4. West India = Export Engine

• Gujarat + Maharashtra dominate exports

MOST COMMON ALLOY GRADES IN INDIA

• ADC12 → 60–70% market share

• LM6 / LM24 → industrial casting

• AlSi series → die casting

• Custom alloys → OEM-specific

ADC12 is widely used due to automotive demand & casting efficiency

FINAL TAKEAWAY

India’s aluminium alloy ingot industry is:

• Highly regionalized

• Scrap-driven

• Dominated by SMEs + few large players

KEY CHARACTERISTICS OF THIS SEGMENT

Strengths

• Highly flexible production

• Low capex (~Rs2–5 crore plants)

• Strong linkage with auto MSMEs

Weakness

• Quality inconsistency

• Heavy dependence on imported scrap

Opportunity

• Export ADC12 due to global shortage

• OEM outsourcing from China

Threat

• Scrap price volatility

• Environmental compliance tightening

Regional SWOT Analysis

North India

Strengths: Proximity to import ports, strong automotive demand

Weaknesses: Pollution regulations

Opportunities: Export potential

Threats: Scrap supply disruption

West India (Gujarat & Maharashtra)

Strengths: Major recycling hubs, port access

Weaknesses: High competition

Opportunities: Export-oriented growth

Threats: Price fluctuations

South India

Strengths: Growing industrial base

Weaknesses: Lower scrap availability

Opportunities: Infrastructure growth

Threats: Logistics cost

East India

Strengths: Low-cost labor

Weaknesses: Limited infrastructure

Opportunities: Untapped market

Threats: Supply chain inefficiencies

IMPORTANT INSIGHT (FOR YOUR LOHAA USE)

The 400–500 T/month segment is the “engine” of India’s aluminium recycling ecosystem:

• Supplies auto component MSMEs

• Drives regional scrap demand

• Acts as price-sensitive buyers in scrap imports

While large players dominate exports, these SME units control domestic liquidity & price trends

FINAL TAKEAWAY

• India’s aluminium alloy ingot industry is bottom-heavy

• 400–500 T/month plants = core volume contributors

• Gujarat + NCR = pricing benchmark regions

• Future growth depends on:

o Scrap availability

o Import logistics

o Environmental compliance

Conclusion: India’s aluminium alloy ingot industry is evolving rapidly, driven by recycling, regional clusters, and strong automotive demand. Despite challenges like scrap dependency and global disruptions, the sector offers significant growth and export potential. Strengthening supply chains, improving efficiency, and leveraging digital platforms like LOHAA will be key to sustained competitiveness.

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for scrap metal are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)