Aluminium Price Swings Despite Stable Production

Introduction

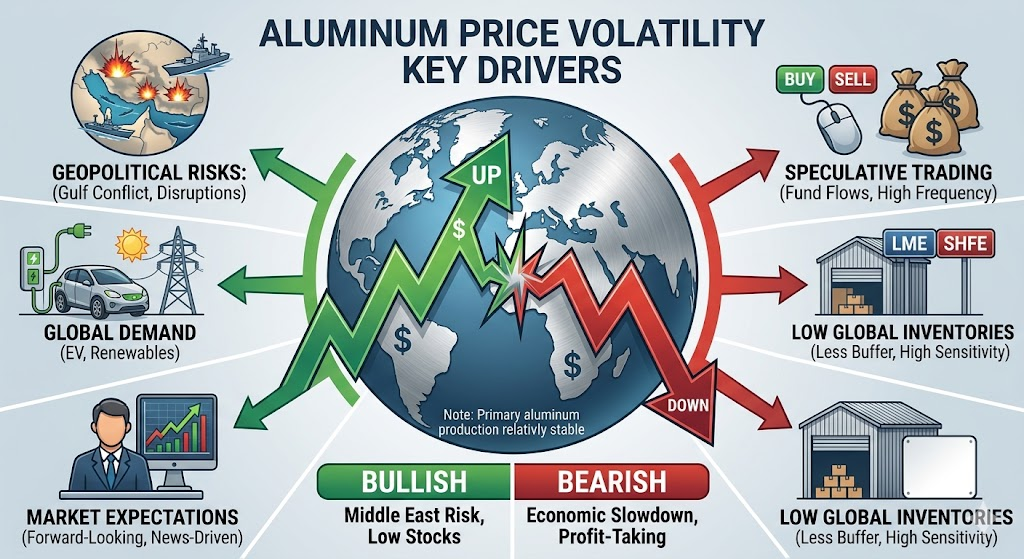

Over the past few months, aluminium prices have experienced significant volatility, leaving buyers, sellers, manufacturers, recyclers, and traders searching for answers. Whenever prices moved higher, many market participants quickly attributed the increase to the ongoing Gulf conflict and the risk of supply disruptions from the Middle East. This explanation seemed reasonable because Gulf countries account for a substantial share of global primary aluminium production and exports.

However, despite the conflict continuing and no comprehensive peace agreement being reached, aluminium prices have repeatedly risen and fallen. At the same time, there has been no major increase in primary aluminium production, nor have significant Gulf smelting capacities been permanently shut down. This raises an important question: if production remains largely stable and the geopolitical situation remains uncertain, why are aluminium prices fluctuating so dramatically? The answer lies in a combination of market psychology, inventory levels, logistics risks, financial trading, trade policies, and future expectations rather than actual production changes alone.

Understanding the Global Aluminium Market

Aluminium is one of the most widely used industrial metals in the world. It plays a critical role in transportation, construction, renewable energy, packaging, electrical infrastructure, aerospace, and consumer goods.

Unlike many commodities, aluminium pricing is influenced by both physical market fundamentals and financial market activity. Prices are primarily determined through the London Metal Exchange (LME), where traders continuously evaluate current supply conditions as well as future expectations.

As a result, aluminium prices often react not only to what is happening today but also to what traders believe may happen tomorrow.

Why the Gulf Conflict Initially Pushed Prices Higher

The Middle East has become a major aluminium-producing region over the last two decades. Countries such as the United Arab Emirates, Bahrain, Oman, Qatar, and Saudi Arabia have invested heavily in large-scale aluminium smelters.

A significant portion of global aluminium exports passes through the Strait of Hormuz, one of the world's most strategically important shipping routes.

When geopolitical tensions increased in the Gulf region, markets immediately began pricing in potential risks such as:

• Supply disruptions

• Export restrictions

• Shipping delays

• Higher freight rates

• Increased marine insurance costs

• Energy supply concerns

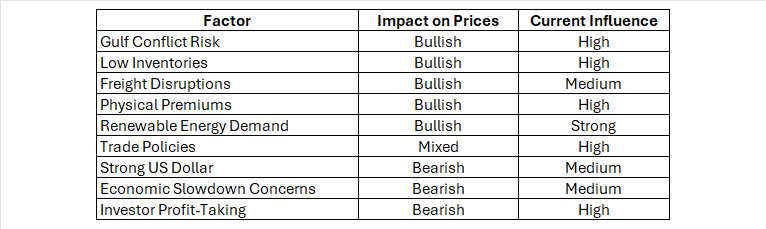

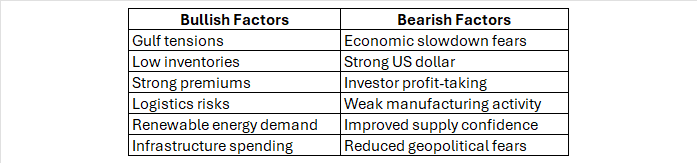

Even before any actual disruption occurred, traders added a "risk premium" to aluminium prices. This caused prices to rise sharply.

Why Prices Fall Even Though the Conflict Continues

Many market participants expected aluminium prices to continue climbing as long as the Gulf conflict remained unresolved.

However, commodity markets do not operate solely on current events. They react to changing expectations.

When traders realize that:

• Smelters are still operating normally

• Exports continue flowing

• Shipping routes remain open

• Governments are avoiding escalation

the initial risk premium begins to fade.

As fear decreases, prices often retreat despite the underlying geopolitical issue remaining unresolved.

This explains why aluminium prices can fall even when headlines continue to report ongoing tensions.

Stable Production Does Not Mean Stable Prices

One common misconception is that prices should remain stable if production remains stable.

In reality, commodity markets are influenced by much more than production.

Consider the following factors:

Market Expectations

Traders continuously assess future supply and demand conditions. Expectations often move prices faster than actual physical changes.

Inventory Levels

When inventories are low, markets become extremely sensitive to any perceived risk.

Logistics

Transportation disruptions can affect availability even when production remains unchanged.

Financial Markets

Large investment funds can buy or sell enormous volumes of aluminium contracts, causing price swings unrelated to physical demand.

The Role of Declining Inventories

One of the most important drivers of aluminium prices during 2026 has been declining inventory levels.

Exchange inventories serve as a buffer between supply and demand.

When inventories are high:

• Buyers have multiple sourcing options.

• Markets remain calm.

• Prices tend to be stable.

When inventories fall:

• Available metal becomes scarce.

• Buyers compete for immediate delivery.

• Market sensitivity increases.

Low inventory environments amplify every geopolitical event, shipping concern, or economic announcement.

Physical Premiums and Backwardation

Another major factor supporting aluminium prices has been the emergence of strong physical premiums and backwardation.

Backwardation occurs when:

Spot Price > Future Price

This market structure indicates immediate demand for physical metal.

Manufacturers requiring prompt delivery are willing to pay higher prices than those seeking future deliveries.

Strong backwardation often signals:

• Tight physical supply

• Low inventories

• Strong nearby demand

This condition can support prices even when overall production remains unchanged.

Freight and Logistics Risks Continue to Influence Prices

Even if aluminium production remains stable, moving metal from producers to consumers remains a challenge.

The Gulf conflict has increased concerns regarding:

• Shipping security

• Insurance costs

• Vessel availability

• Port operations

• Fuel expenses

As transportation costs rise, delivered aluminium becomes more expensive.

Consequently, aluminium prices can increase despite stable production levels.

Financial Investors Play a Major Role

Modern commodity markets are heavily influenced by institutional investors.

Participants include:

• Hedge funds

• Commodity trading advisors

• Investment banks

• Exchange-traded funds

• Algorithmic traders

These investors often trade based on:

• Technical indicators

• Economic forecasts

• Interest-rate expectations

• Currency movements

• Geopolitical developments

A large inflow of speculative capital can push prices significantly higher.

Likewise, profit-taking and risk reduction can trigger rapid declines.

This explains why aluminium prices sometimes move far more aggressively than underlying physical fundamentals would suggest.

Impact of US Dollar Movements

Aluminium is traded globally in US dollars.

As a result:

Strong Dollar

• Makes aluminium more expensive for international buyers.

• Can reduce demand.

• Usually pressures prices lower.

Weak Dollar

• Makes aluminium more affordable globally.

• Encourages buying.

• Supports higher prices.

Currency movements often contribute to daily and weekly price fluctuations.

Demand Remains Strong in Strategic Sectors

Despite concerns about economic growth, several sectors continue to support aluminium consumption.

These include:

Renewable Energy

Solar farms, wind projects, and power transmission networks require large quantities of aluminium.

Electric Vehicles

Automakers continue increasing aluminium usage to reduce vehicle weight and improve efficiency.

Construction

Infrastructure spending remains a major source of demand in many countries.

Packaging

Aluminium remains a preferred material for beverage cans and food packaging.

Strong demand from these sectors provides underlying support to the market.

Trade Policies and Tariffs Add Further Uncertainty

Governments worldwide continue to influence aluminium trade through:

• Import tariffs

• Export restrictions

• Anti-dumping measures

• Carbon regulations

• Local-content requirements

These policies can dramatically alter trade flows.

Metal that would normally move to one region may be redirected elsewhere, creating temporary shortages and surpluses that contribute to price volatility.

Why Aluminium Prices Move Faster Than Production Changes

The key reason aluminium prices are moving rapidly is that markets are pricing future possibilities rather than current realities.

Prices respond to:

• Potential shipping disruptions

• Possible sanctions

• Inventory changes

• Economic forecasts

• Investor sentiment

• Interest-rate expectations

• Currency fluctuations

Physical production is only one component of a much larger pricing equation.

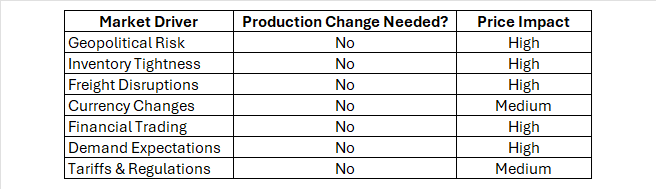

Table 1: Key Drivers of Aluminium Price Volatility

Table 2: Why Prices Move Without Production Growth

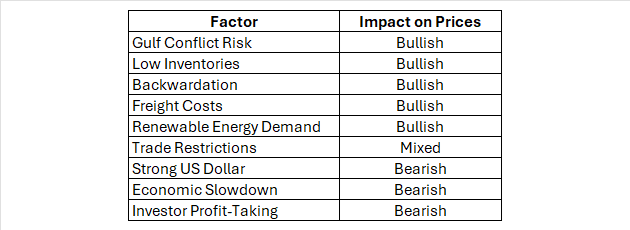

Table 3: Bullish vs Bearish Forces in the Aluminium Market

Table 3: Bullish vs Bearish Forces in the Aluminium Market

Who Are the Winners from the Gulf Conflict?

While geopolitical conflicts create uncertainty, certain market participants benefit from higher aluminium prices.

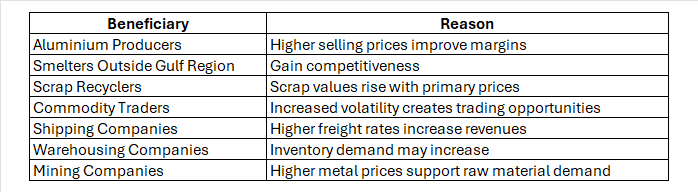

Table 4: Winners from Higher Aluminium Prices

Aluminium Producers

Aluminium Producers

Primary aluminium producers generally benefit when prices rise because their revenues increase while fixed costs remain relatively stable.

Scrap Recyclers

Secondary aluminium producers and scrap recyclers often enjoy higher margins because scrap prices usually rise more slowly than primary metal prices.

Commodity Traders

Volatility creates opportunities for traders to profit from both rising and falling markets.

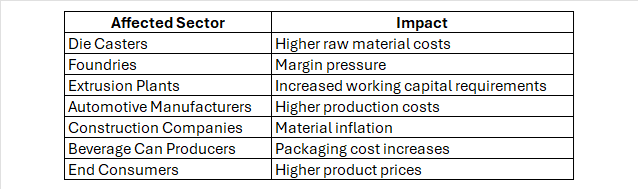

Who Are the Losers from the Gulf Conflict?

Not all market participants benefit from higher prices.

Table 5: Losers from Higher Aluminium Prices Foundries and Die Casters

Foundries and Die Casters

Many foundries struggle to pass higher aluminium costs directly to customers, reducing profitability.

Automotive Industry

Vehicle manufacturers face increased material costs, particularly in electric vehicle production.

Construction Sector

Infrastructure and building projects become more expensive due to higher aluminium costs.

Table 6: Major Drivers of Aluminium Price Volatility

Table 7: Why Prices Move Without Production Growth

The Road Ahead for Aluminium Prices

Going forward, aluminium prices will depend on:

• Gulf geopolitical developments

• Inventory levels

• Global economic growth

• Chinese demand

• Renewable energy investments

• Interest-rate trends

• US dollar movements

Even without production changes, these factors can continue to create substantial volatility.

Conclusion

The recent volatility in aluminium prices cannot be explained solely by the Gulf conflict or by changes in primary aluminium production. While geopolitical tensions continue to create uncertainty, they are only one part of a much larger picture. Aluminium prices today are influenced by declining inventories, strong physical premiums, freight and logistics concerns, investor activity, currency fluctuations, trade policies, and changing expectations regarding future supply and demand.

The market is increasingly driven by perception and anticipation rather than actual production changes. As long as inventories remain tight and geopolitical risks persist, aluminium prices are likely to continue experiencing sharp upward and downward movements. Buyers, sellers, manufacturers, recyclers, and traders must therefore focus not only on production figures but also on broader market indicators that shape sentiment and pricing trends across the global aluminium industry.

References

1. London Metal Exchange (LME) Aluminium Market Data

2. International Aluminium Institute (IAI)

3. World Bureau of Metal Statistics (WBMS)

4. Shanghai Futures Exchange (SHFE)

5. S&P Global Commodity Insights

6. CRU Aluminium Market Reports

7. Reuters Metals Reports

8. World Bank Commodity Markets Outlook

9. International Monetary Fund (IMF) Commodity Analysis

10. Industry Research from Goldman Sachs, Citi and JP Morgan

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the Lohaa Metal Trading App for Android to access live scrap prices and real-time market updates anytime, anywhere.

Download the Lohaa Metal Trading App for iOS to access live scrap prices and real-time market updates anytime, anywhere.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)