GCC Recycling Market Analysis During Gulf War 2026

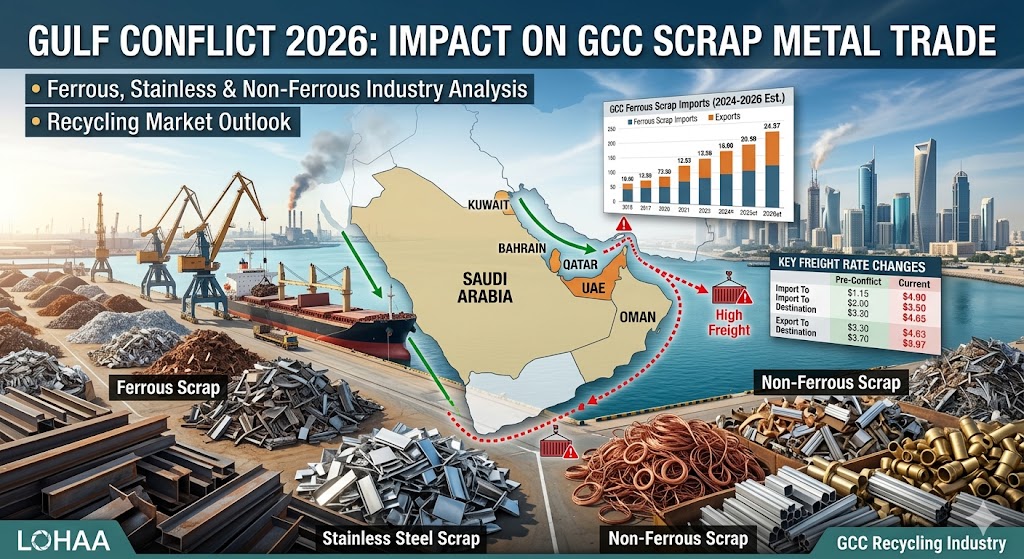

Gulf Conflict 2026: Impact on GCC Scrap Metal Trade and Recycling Industry

Introduction

The Gulf region remains one of the world's fastest-growing consumers of ferrous and non-ferrous scrap due to expanding steelmaking capacity, aluminum production, infrastructure projects, and industrial diversification programs. The escalation of geopolitical tensions in the Gulf during 2026 has created uncertainty across shipping routes, commodity markets, freight costs, insurance premiums, and raw material procurement.

The six GCC countries—Saudi Arabia, UAE, Oman, Kuwait, Qatar, and Bahrain—collectively import millions of tons of scrap annually while simultaneously exporting processed and surplus grades to Asia, Europe, and South Asia.

The ongoing conflict has affected:

• Scrap procurement costs

• Vessel availability

• Marine insurance rates

• Container logistics

• Energy prices

• Regional manufacturing activity

• Investment in recycling infrastructure

Impact of Gulf War on the Metal Industry

Positive Effects

• Higher crude oil revenues strengthen government spending.

• Increased infrastructure investments support steel demand.

• Local recycling becomes more attractive due to import uncertainties.

• Governments accelerate circular economy initiatives.

Negative Effects

• Higher freight costs.

• Increased marine insurance premiums.

• Delayed shipments through strategic waterways.

• Supply disruptions from Europe and North America.

• Volatile steel and aluminum prices.

• Working capital pressure on scrap traders.

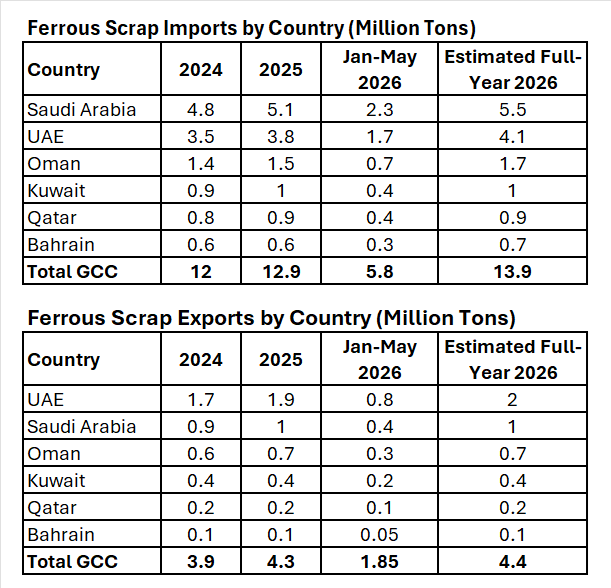

GCC Ferrous Scrap Imports and Exports

Major Ferrous Scrap Suppliers

Major Ferrous Scrap Suppliers

• United States

• United Kingdom

• Netherlands

• Germany

• Belgium

• Japan

• Australia

Major Export Destinations

• India

• Pakistan

• Bangladesh

• Türkiye

• Vietnam

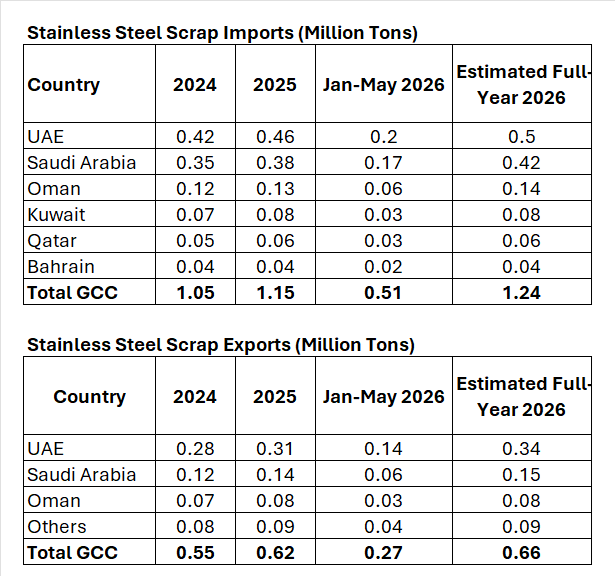

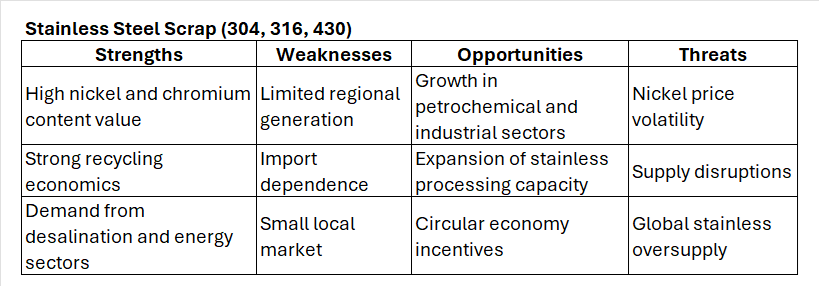

GCC Stainless Steel Scrap Imports and Exports GCC Non-Ferrous Scrap Imports and Exports

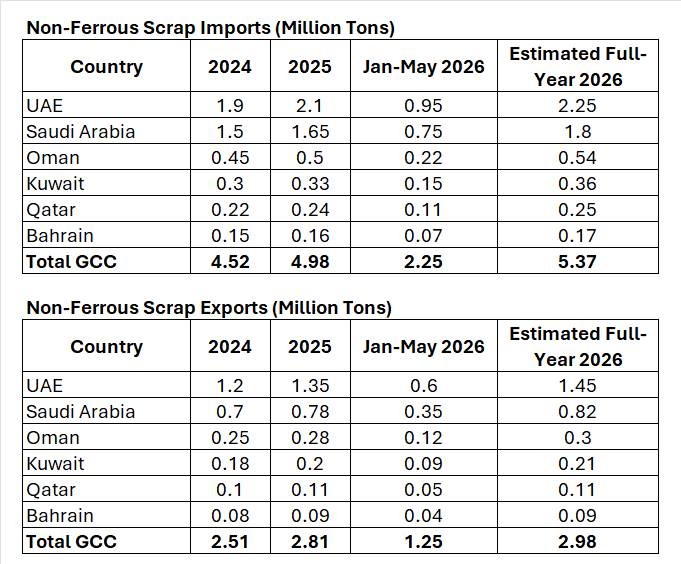

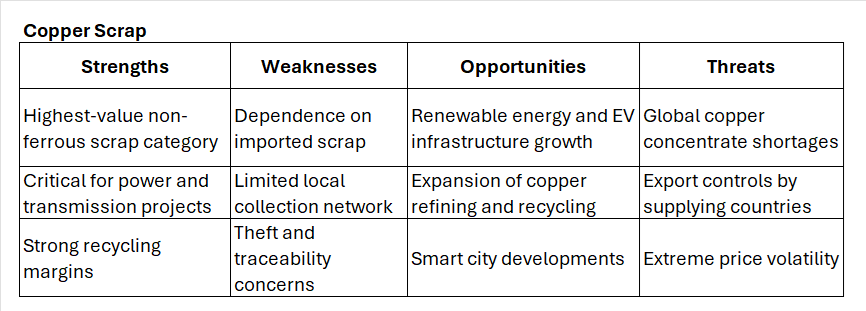

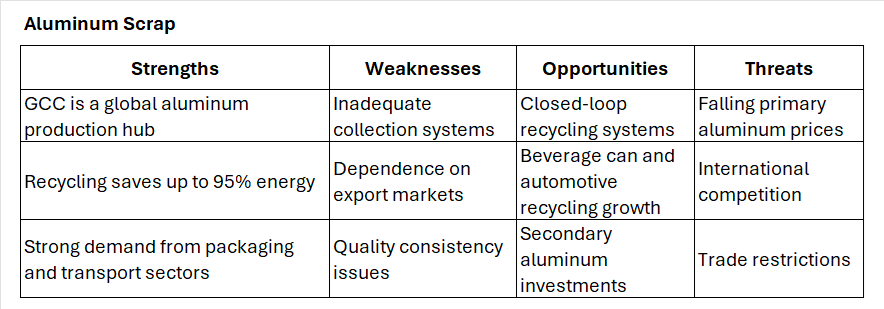

GCC Non-Ferrous Scrap Imports and Exports

Key Non-Ferrous Grades

• Aluminum scrap

• Copper scrap

• Brass scrap

• Lead scrap

• Zinc scrap

• Nickel-bearing scrap

• Electric motor scrap

• Cable scrap

Future Prospects of the GCC Recycling Industry

Saudi Arabia

• Vision 2030 supports circular economy.

• Large-scale steel and aluminum projects.

• Growing domestic scrap collection network.

UAE

• Regional recycling hub.

• Advanced free zones and logistics infrastructure.

• Strong aluminum recycling growth.

Oman

• Strategic export gateway.

• Increasing investments in metal processing.

Qatar

• Infrastructure maintenance cycle generating scrap.

• Expansion of industrial recycling capacity.

Kuwait & Bahrain

• Growing demand for processed scrap.

• Modernization of recycling facilities.

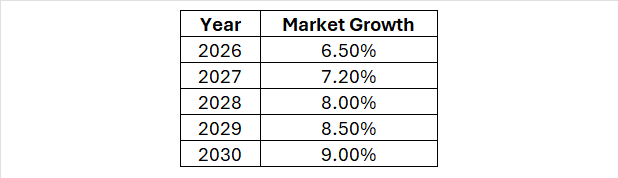

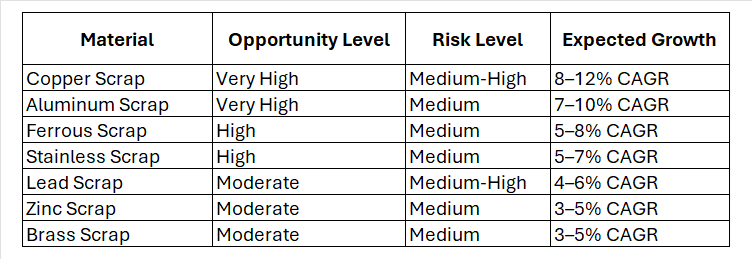

Industry Outlook

Expected GCC recycling market growth:

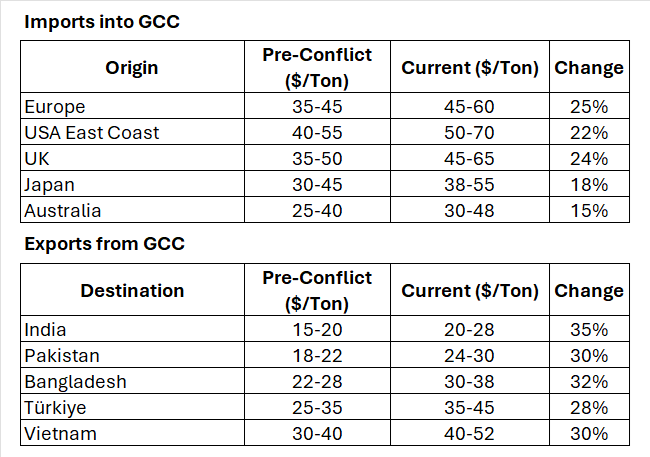

Effect on Sea Freight Charges

Effect on Sea Freight Charges

Imports into GCC

Main Reasons for Higher Freight

Main Reasons for Higher Freight

• Increased war-risk insurance.

• Vessel rerouting.

• Longer transit times.

• Port congestion.

• Higher bunker fuel costs.

SWOT Analysis of GCC Recycling Industry After Gulf Conflict (2026–2028 Outlook)

Country-Wise SWOT Analysis

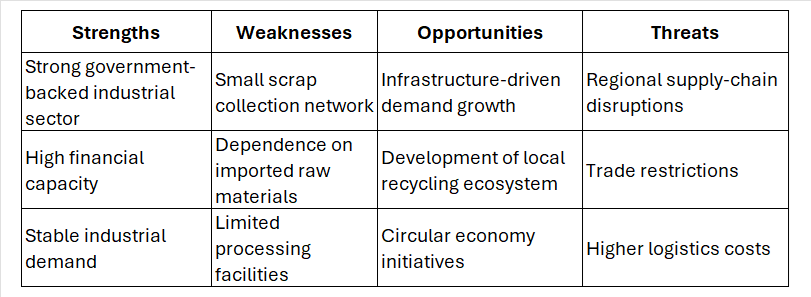

Saudi Arabia

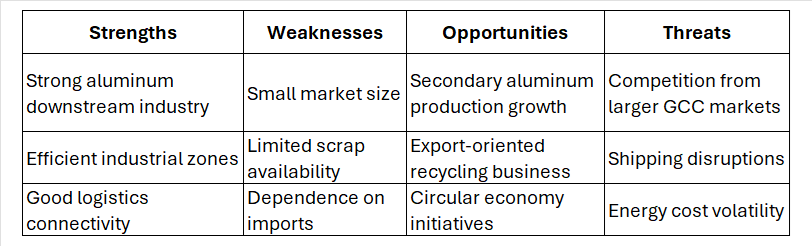

United Arab Emirates (UAE)

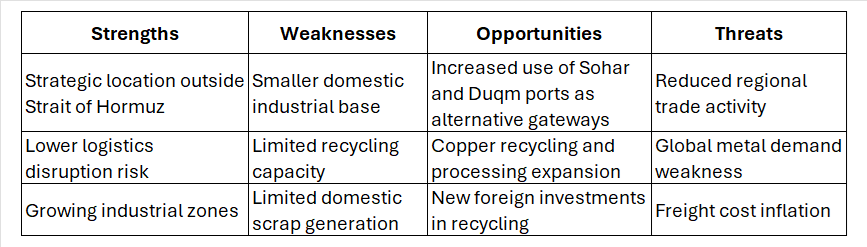

Oman

Qatar

Qatar

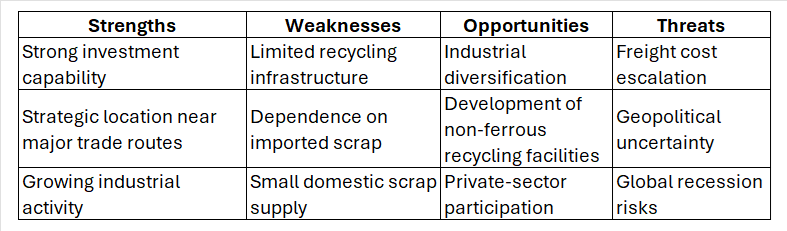

Kuwait

Kuwait

Bahrain

Bahrain

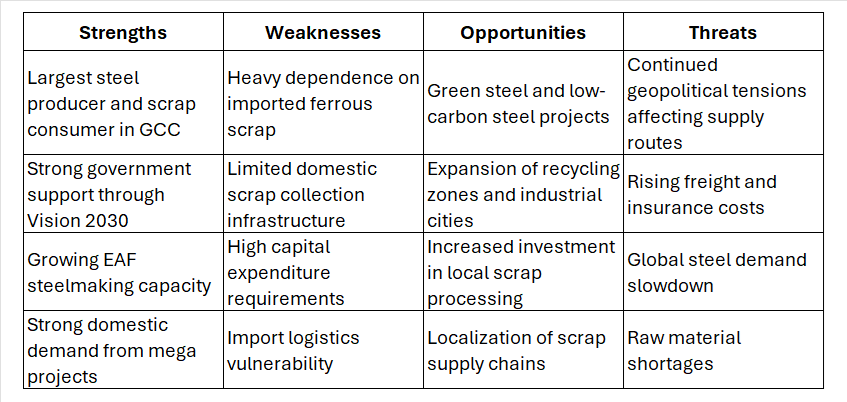

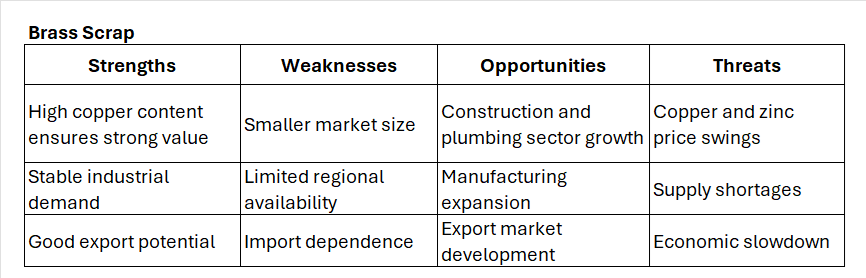

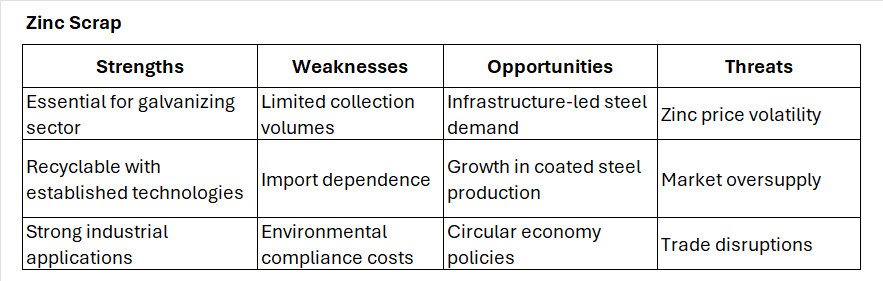

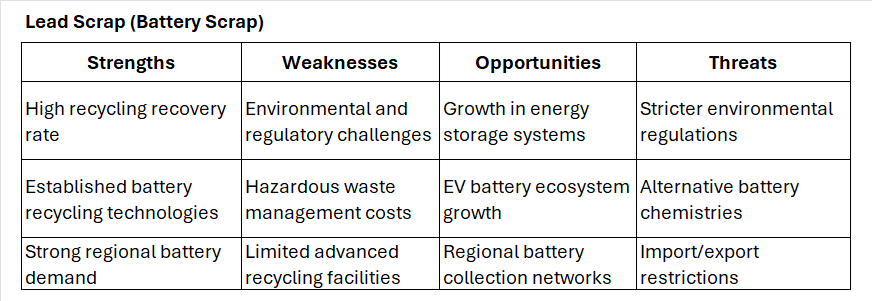

Material-Wise SWOT Analysis After Gulf Conflict

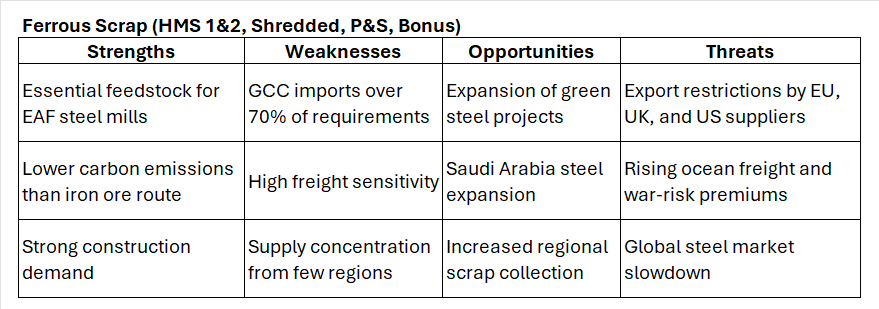

Ferrous Scrap (HMS 1&2, Shredded, P&S, Bonus)

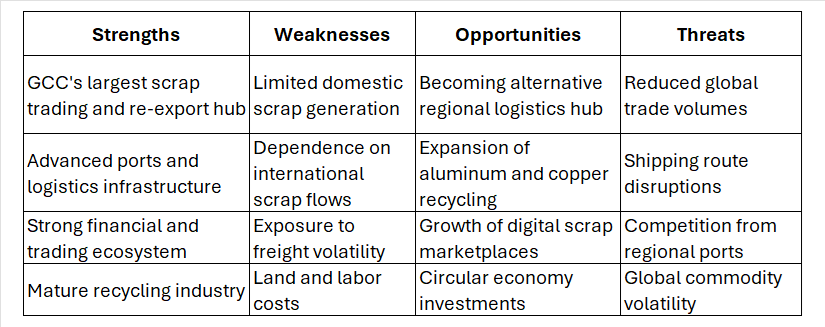

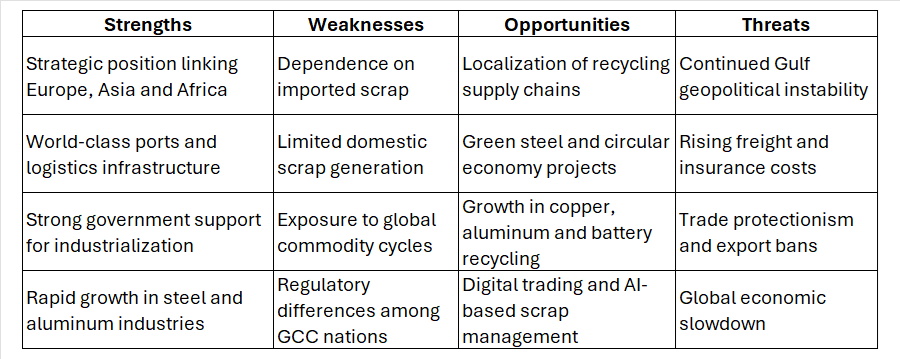

Overall GCC Recycling Industry SWOT After Gulf Conflict

Overall GCC Recycling Industry SWOT After Gulf Conflict

Post-Conflict Strategic Winners (2026–2030)

Post-Conflict Strategic Winners (2026–2030)

Key Takeaway

Key Takeaway

Following the Gulf conflict, Saudi Arabia is expected to dominate ferrous scrap and green steel recycling, while the UAE will remain the leading regional hub for copper, aluminum, stainless steel, and global scrap trading. Oman is positioned to benefit as an alternative logistics corridor, particularly if shipping risks persist around the Strait of Hormuz. Among all materials, copper and aluminum scrap offer the strongest growth potential, driven by energy transition projects, EV infrastructure, and circular economy investments across the GCC.

Conclusion

The Gulf conflict has introduced significant uncertainty into global scrap metal markets, particularly affecting freight costs, supply chains, and procurement strategies. Despite these challenges, the GCC recycling industry remains fundamentally strong due to continued industrialization, infrastructure investments, and ambitious sustainability initiatives.

Ferrous, stainless steel, and non-ferrous scrap demand is expected to continue growing through 2030, supported by steelmaking expansion, aluminum production, and circular economy policies. Countries such as Saudi Arabia and the UAE are likely to emerge as regional recycling leaders, while Oman, Qatar, Bahrain, and Kuwait continue strengthening their processing and export capabilities.

Although short-term disruptions may persist, the long-term outlook for GCC scrap recycling remains positive, with increased local recovery, higher recycling rates, and stronger regional trade expected to offset geopolitical risks.

References

1. Bureau of International Recycling (BIR)

2. World Steel Association

3. International Aluminium Institute

4. Gulf Cooperation Council

5. National customs statistics of GCC member countries

6. Port authority cargo movement reports

7. Metal recycling industry trade associations

8. International shipping and freight market assessments

Note: The 2026 figures for January–May and full-year estimates are indicative market estimates based on trade trends, GCC steelmaking capacity, recycling flows, and shipping activity. Actual customs-reported figures may vary as complete 2026 data becomes available.

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)