India Secondary Steel Industry Report 2026 to 2030

Importance of Secondary Steel Manufacturing in India

India’s secondary steel sector has become one of the most important pillars of the country’s industrial economy. Secondary steel production mainly uses:

• Scrap steel

• Sponge iron (DRI)

• Induction furnaces (IF)

• Electric arc furnaces (EAF)

• Rolling mills

The sector supports infrastructure, housing, railways, automobiles, engineering, renewable energy and industrial manufacturing.

India achieved approximately 168–169 MTPA crude steel production in FY 2025-26, maintaining its position as the world’s second-largest steel producer. (Press Information Bureau)

1. The National Steel Policy 2017 targets:

The Indian National Steel Policy 2017 aims to increase the country’s crude steel production capacity to 300 million tonnes and per capita steel consumption to 160 kg by 2030–31. The policy focuses on promoting domestic steel manufacturing, improving raw material security, expanding infrastructure, encouraging technology upgrades, and enhancing global competitiveness. It also supports secondary steel production through increased scrap recycling, energy efficiency, and environmentally sustainable manufacturing practices. The policy encourages value-added steel production, export growth, and development of modern steel clusters while reducing import dependence and promoting employment generation across the steel and allied industries.

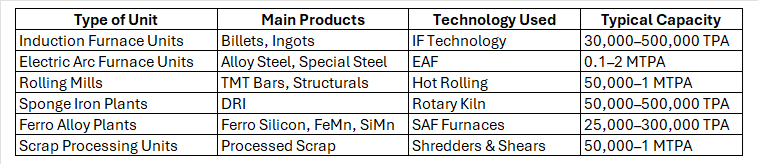

2. Types of Secondary Steel Manufacturing Units

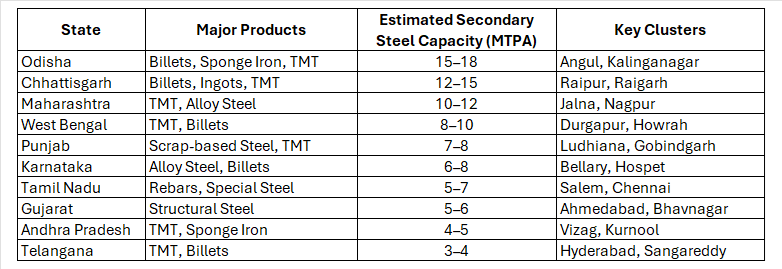

Top 10 States in Secondary Steel Manufacturing

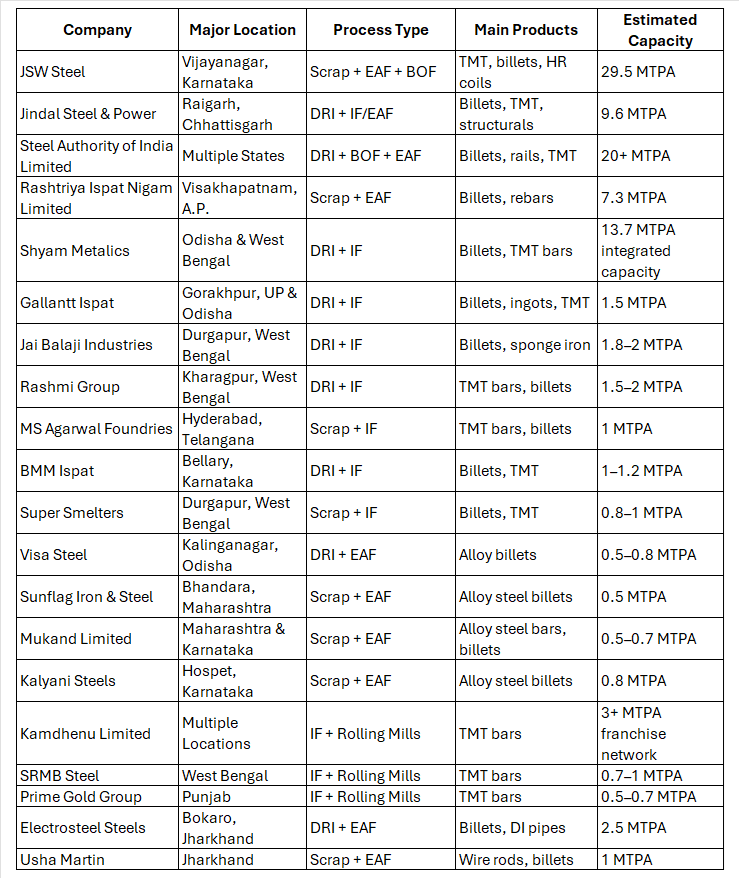

Top 20 Secondary Steel Manufacturing Companies in India

India’s Top Secondary Steel Mills by Process Type, Capacity & Location

Scrap Steel, Sponge Iron (DRI), Induction Furnace (IF) & Electric Arc Furnace (EAF) Based Producers

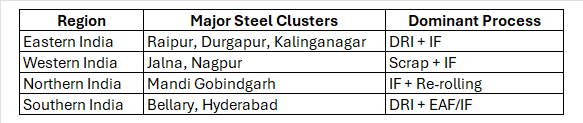

3. Major Secondary Steel Manufacturing Clusters

Key Industry Insights

• India’s secondary steel sector contributes around 45–50% of total steel production.

• Induction furnace units dominate India’s billet and ingot production.

• Chhattisgarh remains India’s largest sponge iron-producing state.

• Maharashtra and Gujarat lead in imported ferrous scrap usage.

• EAF-based steelmaking is expected to grow due to CBAM and green steel demand.

• Scrap-based steel production will increase significantly by 2030 as India expands recycling infrastructure.

JSW Steel, Tata Steel and JSPL continue major capacity expansion programs as India advances toward 300 MTPA steel capacity by 2030. (Press Information Bureau)

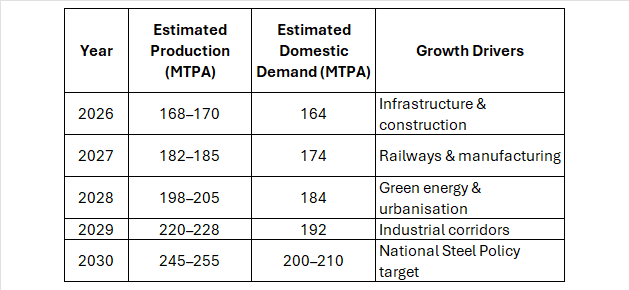

4.India Steel Production & Demand Forecast (2026–2030)

Crude steel and finished steel demand forecast

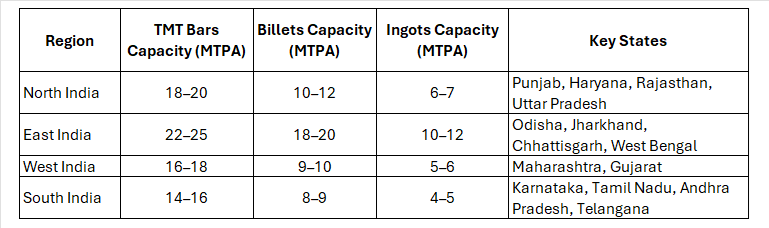

5. Regional Wise TMT, Billet & Ingot Production Capacities

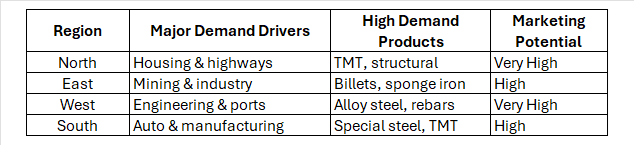

Regional Wise Demand & Marketing Potential

Regional Wise Demand & Marketing Potential

Emerging Growth Segments

• Smart cities

• Metro rail projects

• Warehousing

• Renewable energy structures

• Data centres

• Industrial parks

• Rural infrastructure

India’s finished steel consumption continues to grow rapidly due to infrastructure-led economic expansion. (Press Information Bureau)

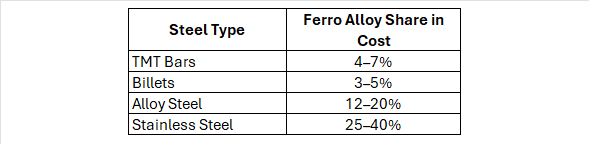

6.Impact of Ferro Alloy Prices on Secondary Steel Manufacturing

a)Ferro alloys are essential for improving:

• Strength

• Hardness

• Corrosion resistance

• Weldability

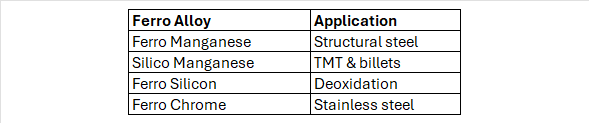

Key Ferro Alloys Used

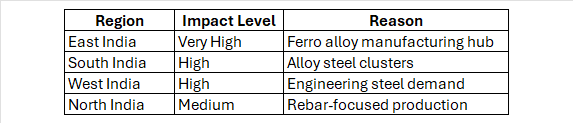

b) Regional Impact of Ferro Alloy Prices

b) Regional Impact of Ferro Alloy Prices

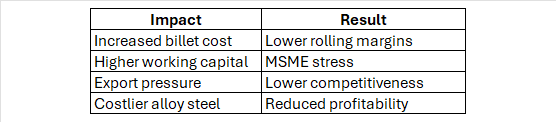

c) Effects of Ferro Alloy Price Rise

Power tariff volatility and manganese ore pricing are major drivers of ferro alloy price fluctuations in India.

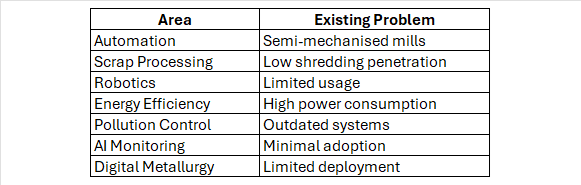

7. Technology & Mechanisation Gaps

India still relies heavily on induction furnace-based steelmaking, while advanced economies use highly automated EAF systems. (AP News)

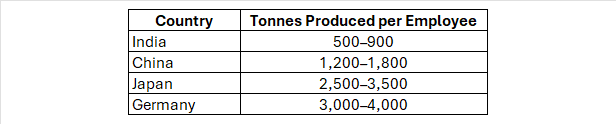

Manpower Requirement in Secondary Steel Plants

Labour Productivity Comparison

India’s steel industry could significantly improve productivity through automation, AI systems and robotic material handling.

India’s steel industry could significantly improve productivity through automation, AI systems and robotic material handling.

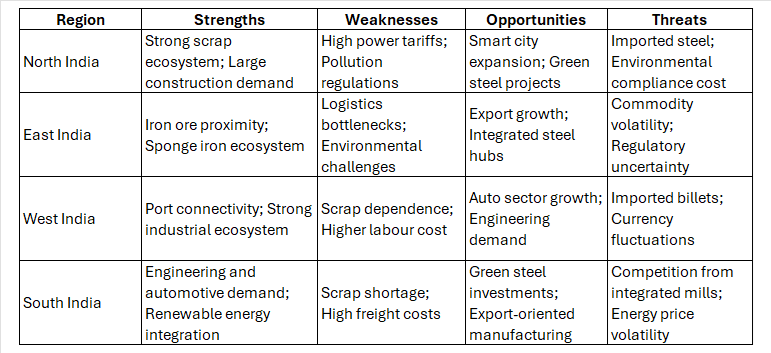

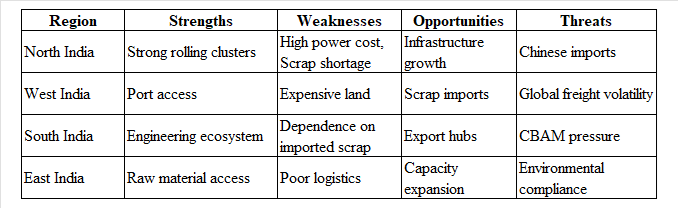

8. SWOT Analysis — Regional Wise

Outlook of India’s Secondary Steel Industry

Outlook of India’s Secondary Steel Industry

Key Trends Expected by 2030

• Expansion of scrap-based EAF steelmaking

• Green steel adoption

• AI-driven rolling mills

• Hydrogen-ready steelmaking

• Renewable energy integration

• Automated scrap sorting

• Increased organised recycling

India’s total steel capacity has already reached approximately 220 MTPA and is progressing toward the official target of 300 MTPA by 2030. (Press Information Bureau)

The secondary steel sector will remain the largest contributor to India’s long steel and construction steel market during the next decade.

9. India Secondary Steel Industry Outlook (2026–2030)

India’s secondary steel industry is becoming the backbone of low-cost and low-emission steel production. The country is targeting 300 MT steelmaking capacity by 2030, and scrap-based steel production through induction furnaces (IF) and electric arc furnaces (EAF) is expected to contribute significantly. (Reclimatize.in)

The major growth drivers are:

• Infrastructure expansion

• Urban housing demand

• Railway and renewable projects

• Automotive manufacturing

• Rising preference for recycled “green steel”

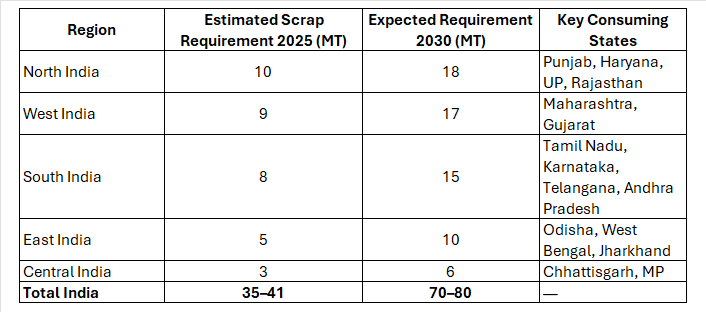

10. Regional Requirement of Ferrous Scrap for Secondary Steel Units

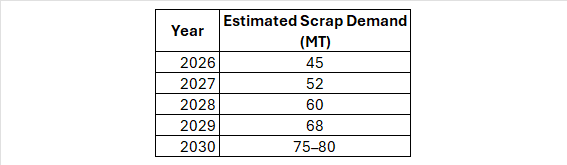

India’s scrap consumption crossed nearly 35–41 MT in FY2025 and may rise to 70–80 MT by 2030 due to EAF/IF expansion. (Reclimatize.in)

India’s scrap consumption crossed nearly 35–41 MT in FY2025 and may rise to 70–80 MT by 2030 due to EAF/IF expansion. (Reclimatize.in)

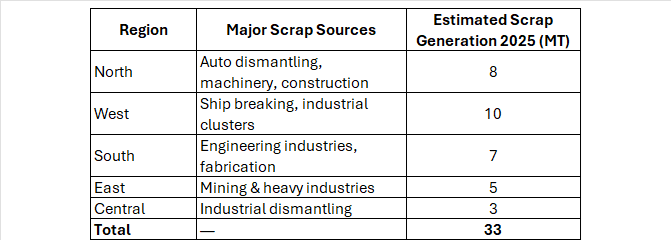

11. Ferrous Scrap Generation within India – Regional Wise Major Scrap Generation Hubs

Major Scrap Generation Hubs

• Gujarat (Alang ship-breaking yard)

• Maharashtra

• Tamil Nadu

• Punjab

• Karnataka

• Delhi NCR

India still faces a structural scrap deficit and depends heavily on imports. (Metals Hub)

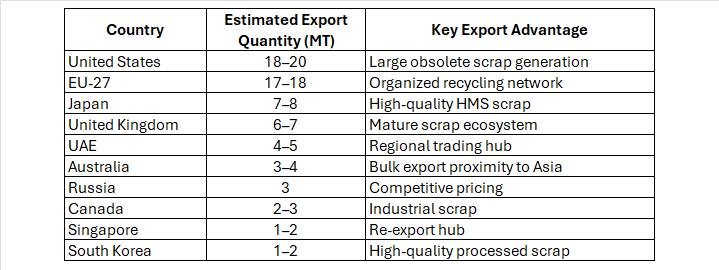

12. Top Ferrous Scrap Exporting Countries (2025)

EU and the US remain dominant global exporters of recycled steel scrap. (BIR)

EU and the US remain dominant global exporters of recycled steel scrap. (BIR)

13. Scrap Demand Forecast in India (2026–2030)

Key Drivers

Key Drivers

• Expansion of EAF steelmaking

• Government green steel policies

• Lower carbon emissions versus BF-BOF route

• Higher urban scrap generation

• Automotive recycling policies

India may face a 20–30 MT annual scrap import gap by 2030.

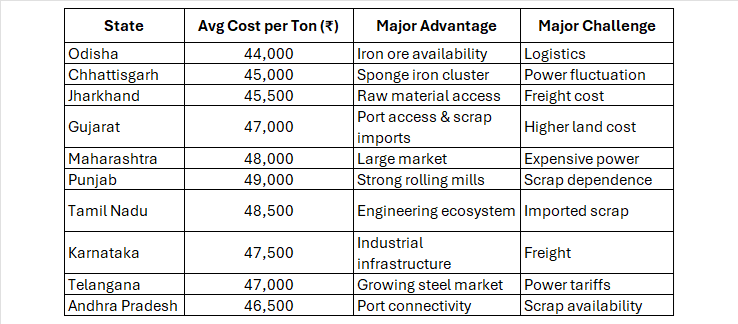

14. Manufacturing Cost Analysis – Top 10 Steel Producing States

a) Approximate Secondary Steel Manufacturing Cost (TMT Rebar) b). Cost Benefit Analysis

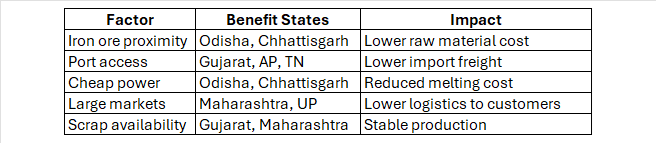

b). Cost Benefit Analysis

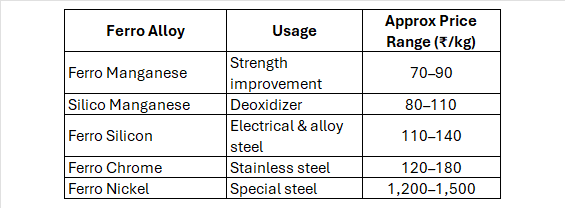

c). Ferro Alloy Requirement & Cost Impact

Major Ferro Alloys Used

Note: Prices are for references only.

Note: Prices are for references only.

d) Impact on Manufacturing Cost

Price Impact

Price Impact

• Manganese ore volatility directly affects TMT margins.

• Chrome and nickel prices significantly influence stainless steel exports.

• Power tariffs heavily impact ferro alloy production economics.

15. Export Opportunities for Secondary Steel

High Potential Export Products India became a net finished steel exporter again in FY2025–26.

India became a net finished steel exporter again in FY2025–26.

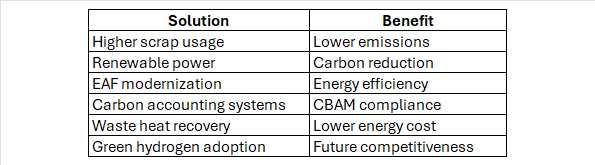

16. SWOT Analysis – Regional Wise a). Impact of CBAM (Carbon Border Adjustment Mechanism)

a). Impact of CBAM (Carbon Border Adjustment Mechanism)

The EU CBAM mechanism may significantly impact Indian steel exporters because Indian steel emissions are higher than EU benchmarks. (CO2 AI)

Expected Impact Remedial Solutions

Remedial Solutions

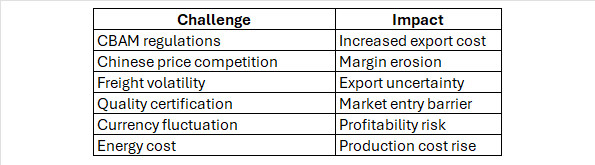

b). Challenges in Exporting Secondary Steel

b). Challenges in Exporting Secondary Steel

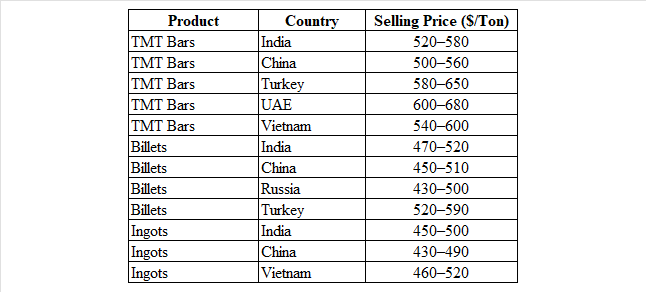

16. Selling Price Comparison with Other Countries (2026 Approx.)

16. Selling Price Comparison with Other Countries (2026 Approx.)

17. Strategic Recommendations

For Manufacturers

• Invest in automated scrap processing

• Increase renewable power usage

• Improve yield optimization

• Adopt digital quality systems

• Develop low-carbon steel products

For Government

• Incentivize organized scrap collection

• Reduce logistics bottlenecks

• Promote green steel certification

• Support ferro alloy capacity expansion

• Encourage CBAM-compliant exports

Conclusion:

India’s secondary steel industry is becoming a vital pillar of sustainable industrial growth, driven by rising infrastructure demand, recycling initiatives, and the transition toward low-carbon steel production. With strong regional manufacturing clusters, growing scrap utilisation, and expanding export opportunities, the sector has significant long-term potential. However, challenges such as technology gaps, mechanisation limitations, high logistics costs, and CBAM-related compliance pressures must be addressed. Investments in automation, renewable energy, advanced recycling systems, and green steel technologies will strengthen competitiveness. By improving efficiency, quality, and sustainability, India’s secondary steel sector can emerge as a global leader in circular and environmentally responsible steel manufacturing.

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)