India Vehicle Scrap Generation Outlook 2024 to 2030

1. Introduction

India is emerging as one of the world's fastest-growing automotive and manufacturing economies. Rapid urbanization, infrastructure expansion, increasing vehicle ownership, and government initiatives promoting circular economy practices are significantly increasing the availability of recyclable metal scrap.

The introduction of the Vehicle Scrappage Policy, stricter emission norms, expansion of electric vehicles (EVs), and modernization of recycling infrastructure are expected to transform India's recycling ecosystem during 2026–2030.

India currently produces millions of two-wheelers, passenger vehicles, commercial vehicles, tractors, and three-wheelers annually. At the same time, ageing vehicles and infrastructure demolition are generating enormous quantities of ferrous and non-ferrous scrap. This scrap serves as an important raw material for steel mills, aluminium producers, foundries, copper recyclers, zinc smelters, and secondary metal industries.

This report presents production statistics, vehicle life regulations, state-wise recycling potential, construction demolition scrap generation, SWOT analysis, and future demand forecasts for India's recycling industry.

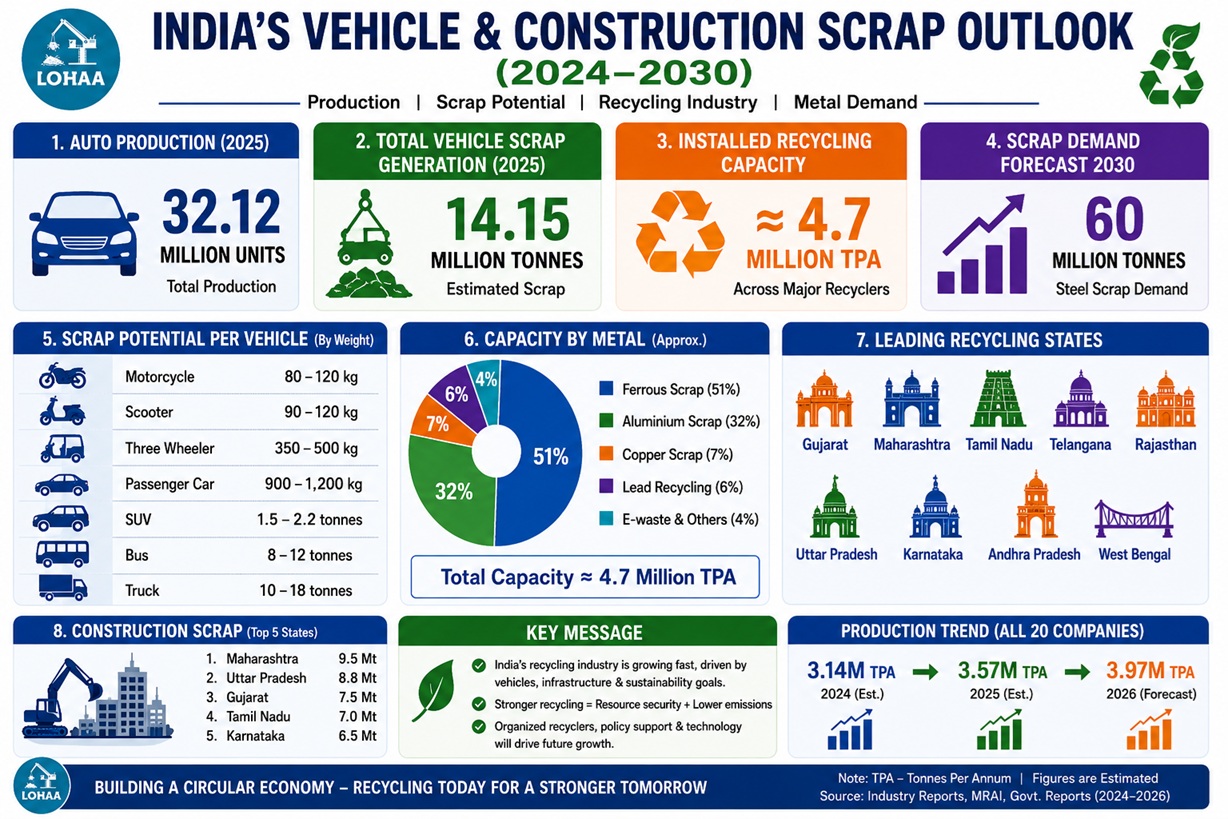

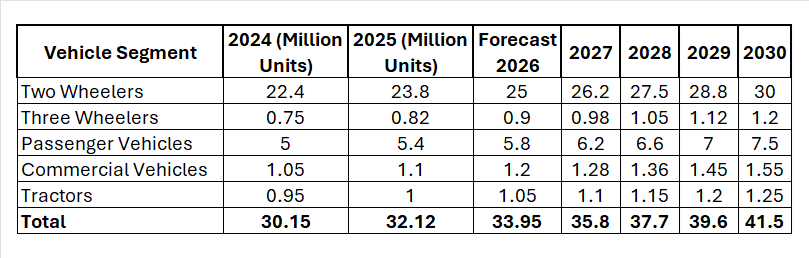

2. India's Automobile Production (2024–2030 Forecast)

Table 1: India's Automobile Production

3. Government Regulations on Vehicle Life

3. Government Regulations on Vehicle Life

3.1 Two-Wheelers

• Registration validity: 15 years

• Renewal possible after fitness test

• Vehicles above 15 years require periodic fitness certification

3.2 Three-Wheelers

• Registration validity: 15 years

• Commercial vehicles require regular fitness inspection

• Electric three-wheelers follow similar renewal procedures

3.3 Passenger Cars (Four-Wheelers)

Private Vehicles

• Registration: 15 years

• Renewable every 5 years after fitness

Government Vehicles

• Mandatory scrapping after 15 years

3.4 Trucks and Buses

Commercial Vehicles

• Fitness test every year after 8 years

• Mandatory periodic inspection

• Vehicles failing fitness tests are recommended for scrapping

Fleet operators are increasingly replacing vehicles between 12–15 years due to fuel efficiency and maintenance costs.

4. Average Vehicle Life in India

- Motorcycle: 15–18 Years

- Scooter: 15 Years

- Three Wheeler: 12–15 Years

- Passenger Car: 15–20 Years

- SUV: 15 Years

- Pickup: 15 Years

- Truck: 12–15 Years

- Bus: 12–15 Years

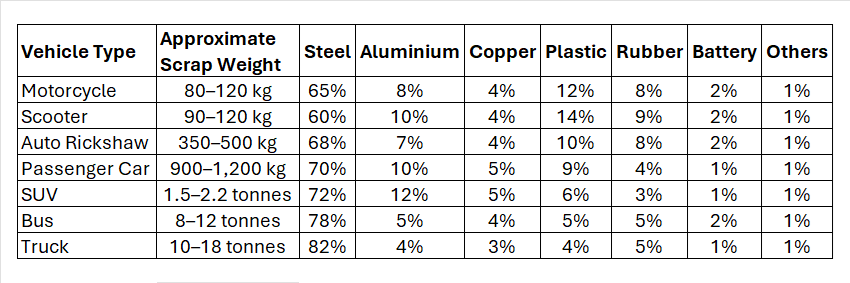

5. Scrap Generation Potential per Vehicle

Table 2

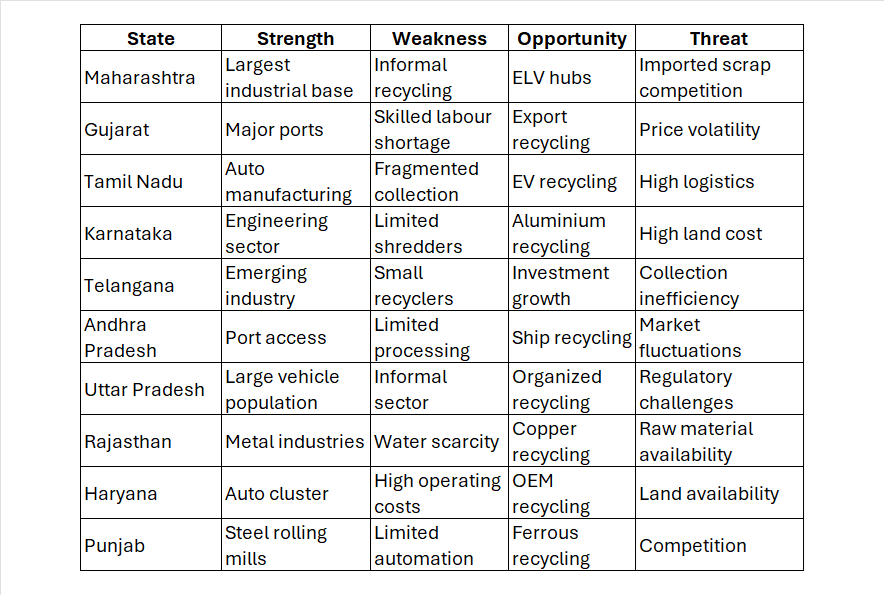

6. SWOT Analysis of Recycling Industry in Top 10 States

Table 3

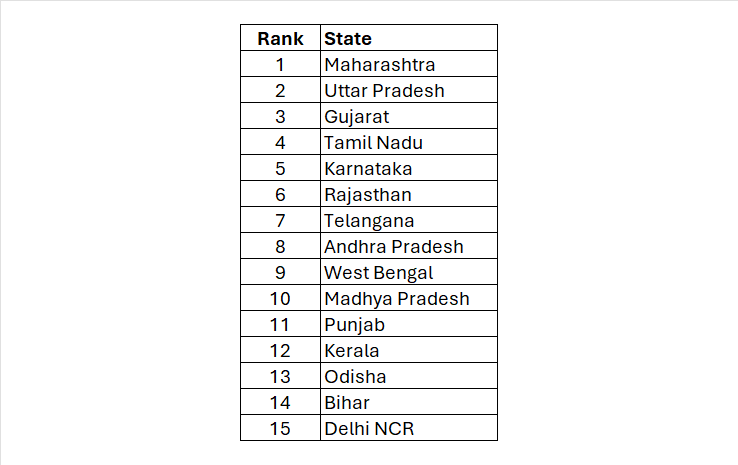

7. Top 15 States by Vehicle Scrap Generation Potential

Table: 4

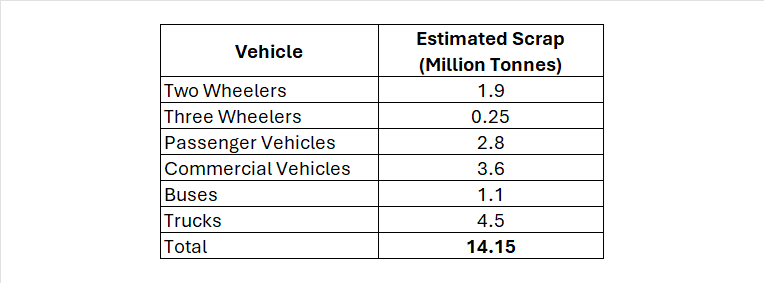

8. Estimated Annual Scrap Generation by Vehicle Category (2025)

8. Estimated Annual Scrap Generation by Vehicle Category (2025)

Table 5

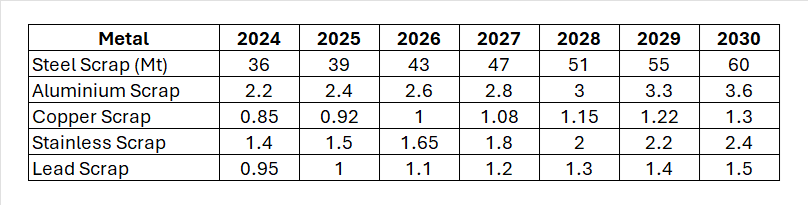

9. Indian Demand for Various Metal Scrap

9. Indian Demand for Various Metal Scrap

Table 6

10. Scrap Generation from Building Demolition

10. Scrap Generation from Building Demolition

Rapid urban redevelopment, smart cities, metro rail projects, highways, airports, and industrial parks are substantially increasing demolition waste generation.

The majority consists of steel reinforcement bars, structural steel, aluminium, copper cables, stainless steel, and cast iron.

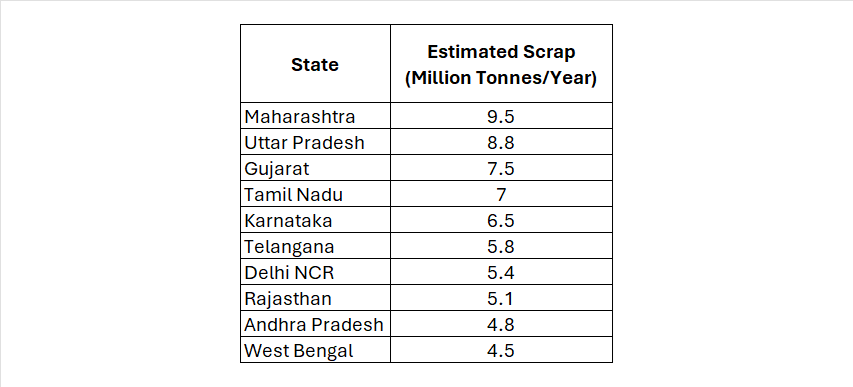

Table 7: Top 10 States Generating Construction Scrap

11. Growth Drivers of India's Recycling Industry

11. Growth Drivers of India's Recycling Industry

Major growth drivers include:

• Vehicle Scrappage Policy

• Circular Economy initiatives

• Net Zero commitments

• Growth in Electric Vehicles

• Steel capacity expansion

• Aluminium recycling investments

• Urban redevelopment

• Infrastructure expansion

• Digital scrap trading platforms

• Organized recycling parks

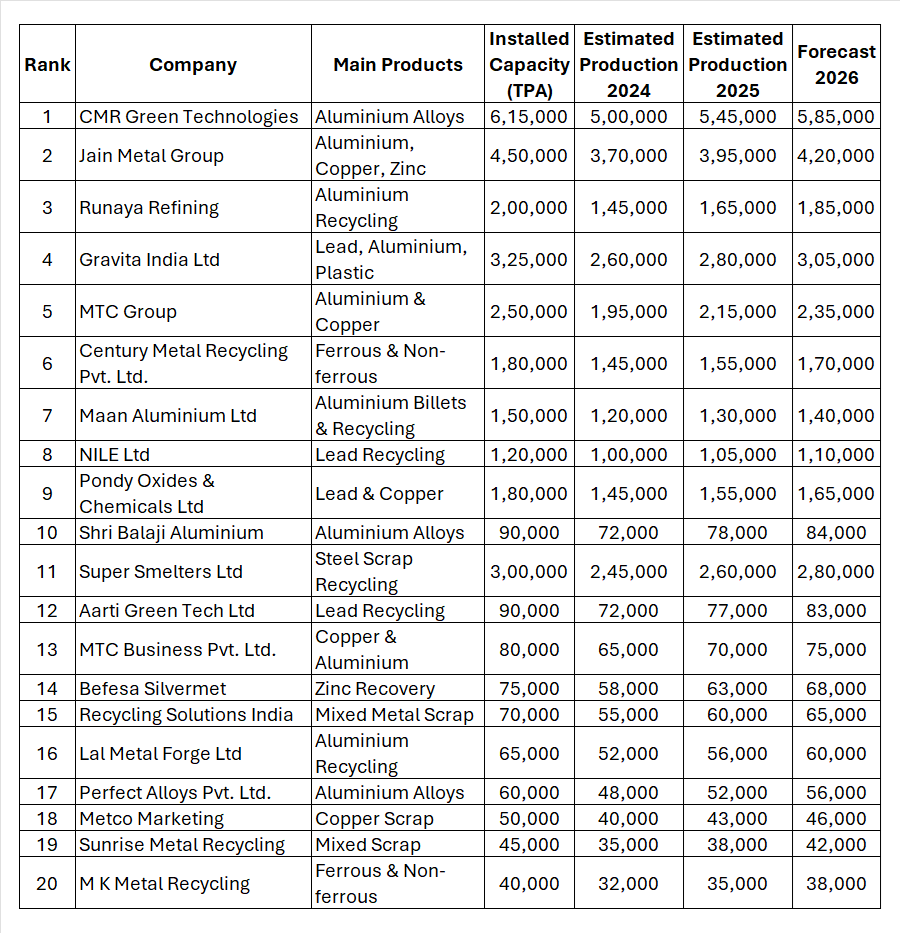

12. Below is a consolidated list of India's leading organized metal recyclers. Since most Indian recyclers are privately held, plant capacities are publicly available, but annual production is often not officially disclosed. Therefore, the production figures below are industry estimates based on capacity utilization, company announcements, and market trends rather than audited production data.

Table 8: Top 20 Indian Metal Recyclers – Capacity, Production (2024–2026 Forecast)

13. Challenges

The sector continues to face several challenges:

• Large informal recycling market

• Low collection efficiency

• Lack of organized dismantling facilities

• Limited shredding capacity

• Poor segregation of metals

• High logistics costs

• Price volatility

• Limited awareness among vehicle owners

• Import dependence for quality scrap

• Limited investment in advanced recycling technologies

Industry Highlights

• CMR Green Technologies is India's largest organised aluminium recycler, with more than 615,000 tonnes per annum of installed recycling capacity across multiple plants. (Reuters)

• India's organised metal recycling sector is expanding rapidly as demand from the automotive, infrastructure and engineering sectors increases, while government support for circular economy initiatives strengthens. (IMARC Group)

• Industry-wide capacity utilisation among organised recyclers is generally estimated at 80–95%, depending on scrap availability and metal prices.

• Aluminium recycling is expected to be the fastest-growing segment through 2030, driven by automotive lightweighting, EV manufacturing and increasing demand for secondary aluminium. (Reuters)

14. Future Outlook (2026–2030)

India's scrap recycling industry is expected to witness unprecedented growth over the next five years. The combination of increasing vehicle ownership, ageing vehicle fleets, expanding infrastructure, and supportive government policies will significantly increase domestic scrap availability.

Steel recycling will remain the largest segment, supported by the rapid expansion of electric arc furnace (EAF) steelmaking. Aluminium recycling is expected to grow due to rising use of lightweight materials in automobiles and electric vehicles. Copper recycling will also gain momentum with increasing electrification, renewable energy projects, and EV adoption.

Organized vehicle dismantling centres, automated shredding facilities, digital scrap marketplaces, and improved reverse logistics are likely to enhance collection efficiency and material recovery rates. States with strong industrial ecosystems and port infrastructure, such as Maharashtra, Gujarat, Tamil Nadu, Karnataka, Telangana, and Andhra Pradesh, are expected to emerge as key recycling hubs.

Overall, India's transition towards a circular economy will reduce dependence on imported raw materials, lower carbon emissions, conserve natural resources, and create significant employment opportunities across the recycling value chain.

15. Conclusion

India's vehicle and construction recycling sector is entering a transformative phase driven by economic growth, urbanization, sustainability goals, and supportive government policies. Rising automobile production, combined with an ageing vehicle fleet and increased infrastructure redevelopment, is creating substantial opportunities for organized scrap collection and recycling. Steel will continue to dominate the recycling market, while aluminium, copper, stainless steel, lead, and battery recycling will expand rapidly with the growth of electric mobility and renewable energy. Although the industry still faces challenges such as fragmented collection systems, informal recycling practices, and inadequate processing infrastructure, investments in modern recycling facilities and digital trading platforms are steadily improving efficiency. Between 2026 and 2030, India is expected to become one of the world's fastest-growing recycling markets, strengthening domestic raw material security, reducing carbon emissions, supporting circular economy objectives, and generating significant employment. A well-organized recycling ecosystem will play a crucial role in achieving India's long-term industrial and sustainability ambitions.

16. References

1. Ministry of Road Transport and Highways (MoRTH), Government of India

2. Ministry of Heavy Industries, Government of India

3. Society of Indian Automobile Manufacturers (SIAM)

4. Automotive Component Manufacturers Association of India (ACMA)

5. Ministry of Steel, Government of India

6. Ministry of Environment, Forest and Climate Change (MoEFCC)

7. Central Pollution Control Board (CPCB)

8. NITI Aayog – Circular Economy Reports

9. Indian Bureau of Mines (IBM)

10. Steel Scrap Recycling Policy, Government of India

11. National Vehicle Scrappage Policy Guidelines

12. World Steel Association

13. International Aluminium Institute (IAI)

14. International Copper Study Group (ICSG)

15. International Energy Agency (IEA)

16. Bureau of Indian Standards (BIS)

17. Construction and Demolition Waste Management Rules, India

18. Federation of Indian Chambers of Commerce & Industry (FICCI)

19. Confederation of Indian Industry (CII)

20. Various industry reports on metal recycling, infrastructure, and automotive sector forecasts (2024–2026).

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the Lohaa Metal Trading App for Android to access live scrap prices and real-time market updates anytime, anywhere.

Download the Lohaa Metal Trading App for iOS to access live scrap prices and real-time market updates anytime, anywhere.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)