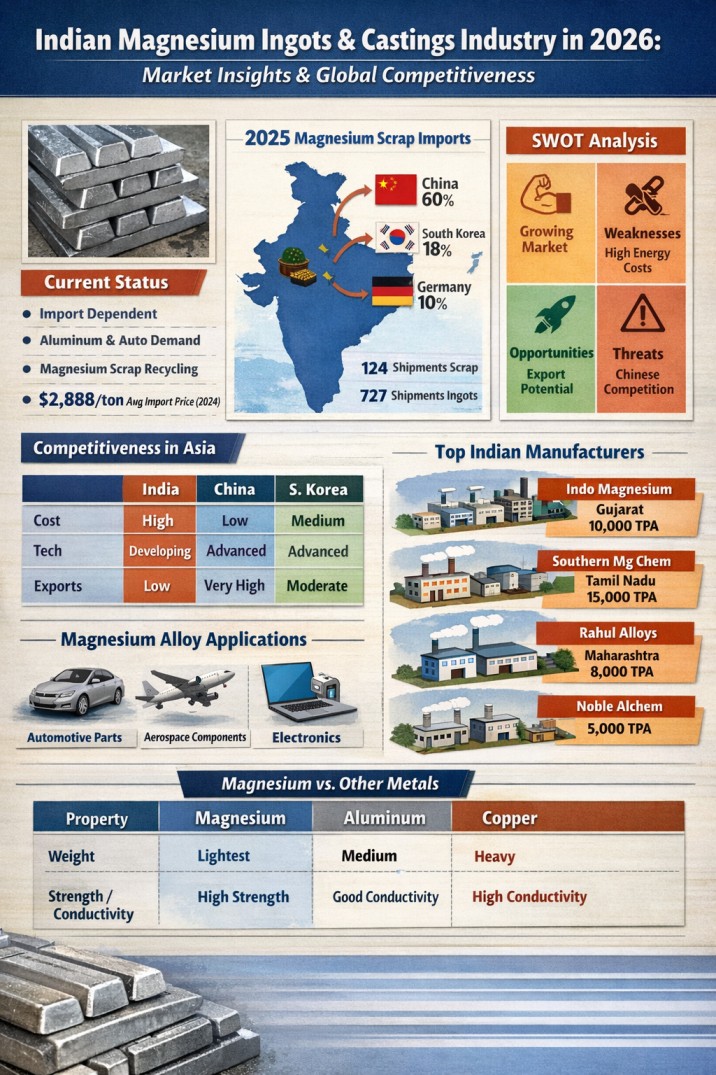

Indian Magnesium Ingots Market Status & SWOT 2026

Introduction

India’s magnesium ingot and casting industry in 2026 is emerging as a niche but strategically important segment within the non-ferrous metals ecosystem. With growing demand from aluminum alloying, automotive lightweighting, aerospace, and die-casting sectors, magnesium is gaining traction as a critical material. However, India remains heavily dependent on imports due to limited domestic primary production capacity. The availability of magnesium scrap, coupled with global sourcing—primarily from China and other Asian countries—plays a vital role in sustaining downstream industries. Rising environmental regulations, recycling initiatives, and the push for lightweight materials are reshaping the industry landscape. This blog explores the present status of Indian magnesium ingot manufacturers, supply chain dynamics, SWOT analysis, regional distribution, and future competitiveness compared to Asian markets.

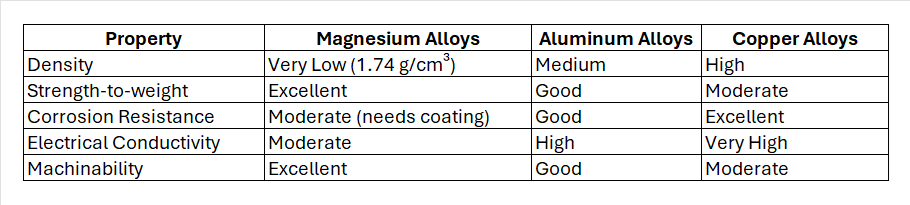

Importance of Magnesium Alloys vs Other Non-Ferrous Metals

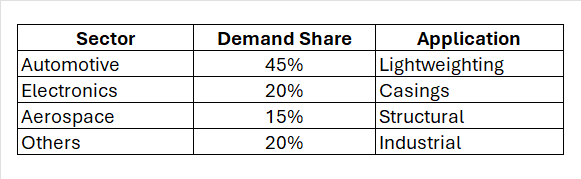

Demand & Applications of Magnesium Alloys

Demand & Applications of Magnesium Alloys Importance of Magnesium Alloys vs Other Non-Ferrous Metals

Importance of Magnesium Alloys vs Other Non-Ferrous Metals

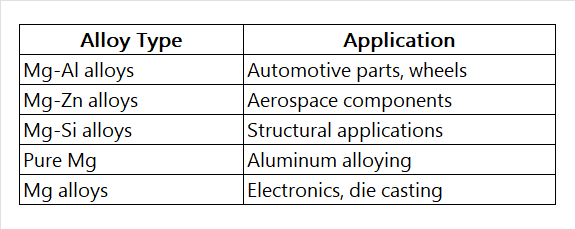

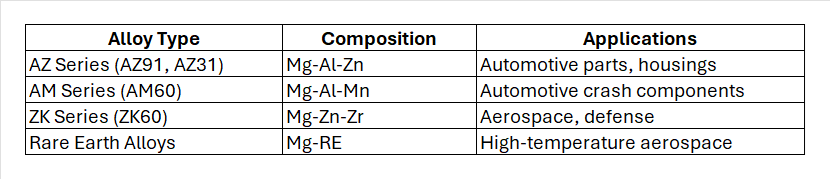

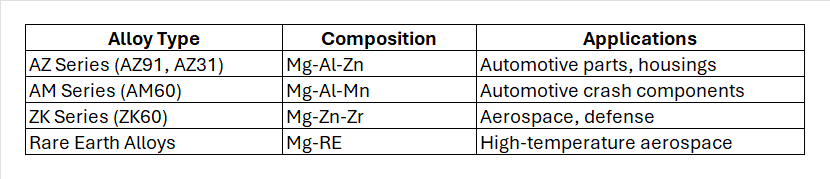

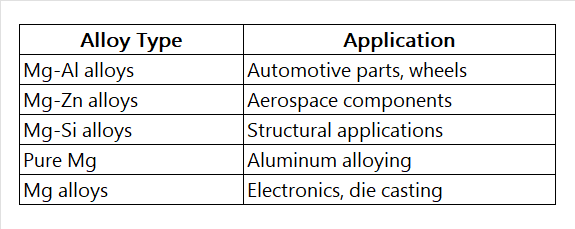

Types of Magnesium Alloys & Applications

Types of Magnesium Alloys & Applications

Demand for Magnesium Alloy Ingots & Applications

Industrial Applications of Magnesium Alloy Components

• Automotive: Gearboxes, steering wheels, EV battery housings

• Aerospace: Structural components, aircraft interiors

• Electronics: Laptop frames, mobile casings

• Renewable Energy: Lightweight structures for solar & wind systems

Demand & Applications of Magnesium Alloys

Present Status of Magnesium Ingots in India (2026)

Present Status of Magnesium Ingots in India (2026)

• India is a net importer of magnesium, with domestic production limited.

• Import dependency is primarily due to:

o Lack of large-scale primary magnesium plants

o High energy requirements for production

• Demand is driven by:

o Aluminum alloying (largest consumption)

o Automotive light weighting

o Steel desulfurization

Key Insight:

• Average magnesium import price: ~$2,888/ton (2024)

• Price volatility is influenced by Chinese export policies & energy costs

Magnesium Scrap Availability & Imports (2025)

Domestic Scrap Scenario

• Limited organized magnesium scrap ecosystem

• Scrap mainly generated from:

o Die-casting industries

o Alloy manufacturing units

Import Data (2025)

• ~124 shipments of magnesium scrap imported (Volza)

• ~727 shipments of magnesium ingots imported (Volza)

Insight:

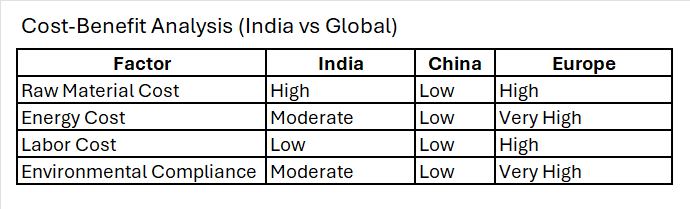

India has cost advantages in labour, but depends heavily on imports, affecting competitiveness.

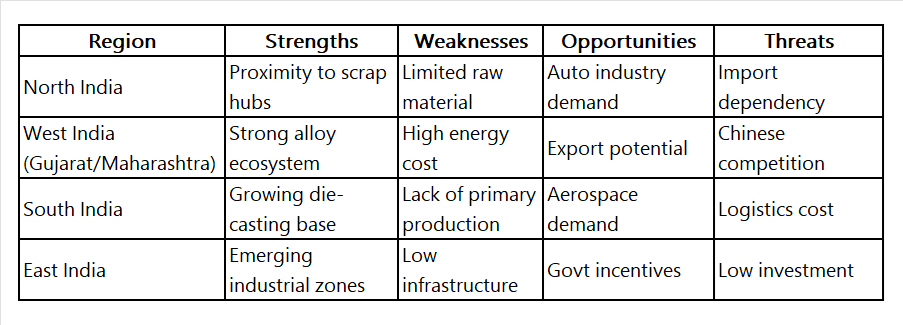

SWOT Analysis – Indian Magnesium Ingot Manufacturers (Regional)

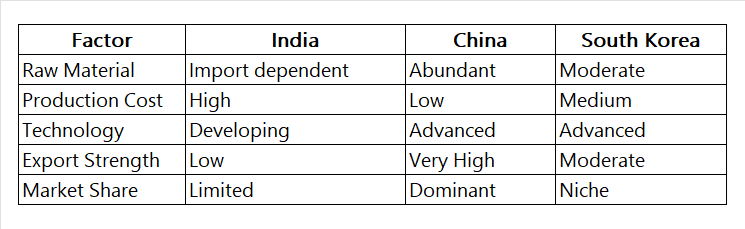

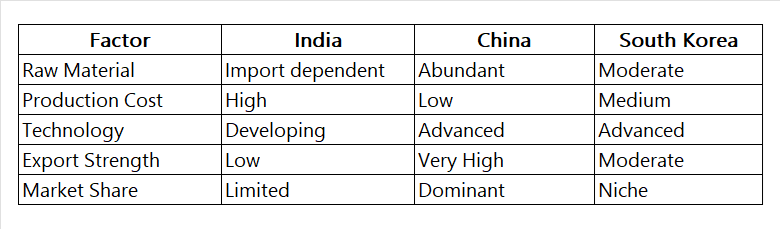

Competitiveness vs Asian Countries

Competitiveness vs Asian Countries

Key Insight:

Key Insight:

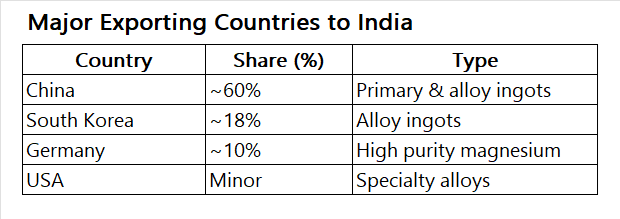

• China dominates ~97% global magnesium exports (Volza)

• India competes mainly in downstream alloying and casting

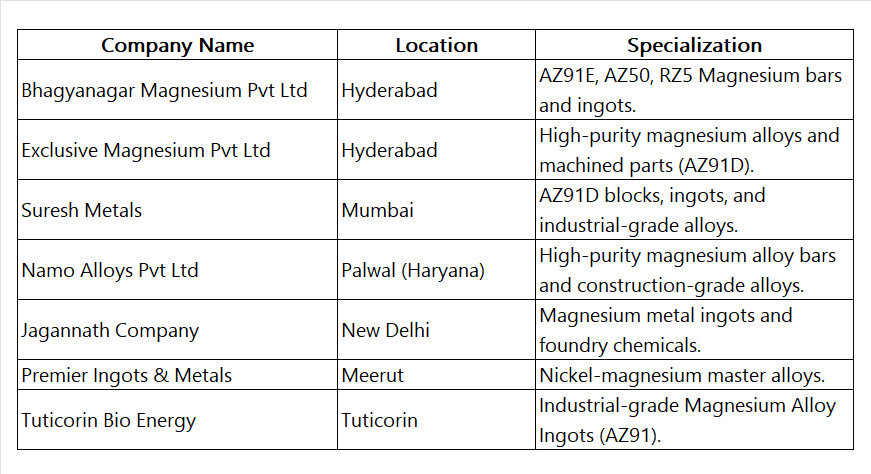

Top Magnesium Ingots Manufacturers (Indicative Table)

(Note: Industry is fragmented with SMEs and alloy producers)

(Note: Industry is fragmented with SMEs and alloy producers)

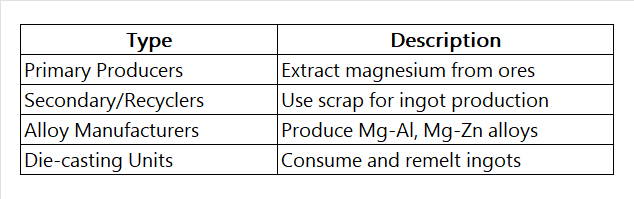

Types of Magnesium Ingots Manufacturers

Competitiveness vs Asian Countries

Competitiveness vs Asian Countries

Key Insight:

Key Insight:

• China dominates ~97% global magnesium exports (Volza)

India competes mainly in downstream alloying and casting

Quality Compliances of Magnesium Ingots

• ASTM B92 / B93 standards

• ISO 9001 certified production

• Chemical composition control:

o Mg purity (99.8%+)

o Impurities (Fe, Ni, Cu)

• Surface quality:

o No oxidation

o No cracks/voids

Conclusion

India’s magnesium ingot industry in 2026 remains import-dependent but holds strong growth potential driven by lightweight applications and alloy demand. Strengthening domestic production, recycling infrastructure, and technology adoption will be key to improving competitiveness against dominant Asian players, especially China.

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for scrap metal are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)