SEA Nonferrous Scrap Market Outlook 2024–2030

Introduction

The Southeast Asian nonferrous metals sector has emerged as one of the fastest-growing industrial ecosystems globally due to rapid urbanisation, infrastructure development, automotive manufacturing, electronics production and energy transition investments. Countries such as Indonesia, Vietnam, Thailand, Malaysia and the Philippines are increasingly important in the production and consumption of aluminium, copper, nickel, lead, zinc and related scrap materials.

The region is witnessing a structural shift toward circular economy practices, with governments encouraging recycling, domestic processing and higher-value downstream manufacturing. Scrap availability has grown significantly due to industrialisation, increasing end-of-life products, construction demolition and automotive recycling. Simultaneously, several Southeast Asian countries continue to depend on imported scrap to support secondary smelting and alloy production.

Between 2024 and 2030, Southeast Asia is expected to strengthen its role as a strategic hub for both primary nonferrous metal production and secondary recycling activities. Indonesia’s nickel and aluminium expansion, Vietnam’s manufacturing boom, Thailand’s automotive recycling ecosystem and Malaysia’s secondary metal processing sector will shape regional trade flows.

This report analyses:

• Nonferrous scrap generation potential by country

• Primary nonferrous metal production trends

• Surplus and deficit positions

• Export opportunities

• Export restrictions and regulatory frameworks

• Domestic demand trends

• Forecasts for 2026–2030

Key Nonferrous Materials Covered

a). Aluminium

b). Copper

c). Brass

d) Lead

e). Zinc

f) . Nickel

g) Stainless Steel Scrap

h) . Electronic Scrap (E-waste containing nonferrous metals)

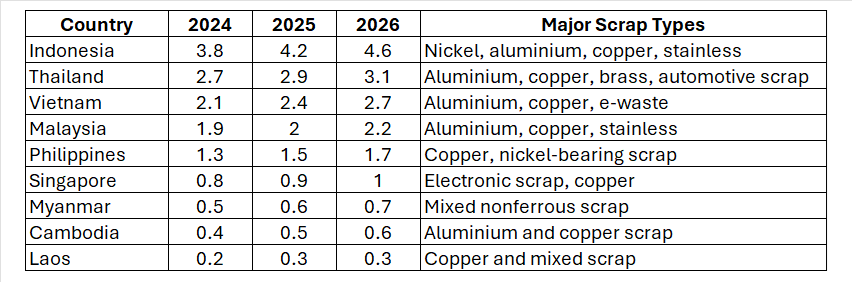

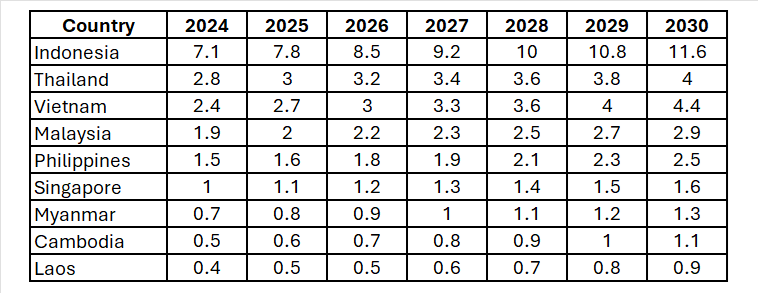

Southeast Asia Nonferrous Scrap Generation Potential (2024–2026)

Table 1: Estimated Nonferrous Scrap Generation by Country (Million Tonnes)

Key Observations

Indonesia

Indonesia is rapidly emerging as the dominant nonferrous scrap generator in Southeast Asia due to:

• Massive nickel processing expansion

• Stainless steel manufacturing growth

• EV battery ecosystem development

• Infrastructure and construction activity

Nickel-bearing scrap and stainless steel scrap are expected to show the fastest growth rates.

Thailand

Thailand remains the region’s largest automotive manufacturing hub, creating substantial:

• Aluminium auto scrap

• Copper wire scrap

• Brass scrap

• Lead battery scrap

Vietnam

Vietnam’s electronics manufacturing boom is increasing:

• Copper scrap generation

• Aluminium extrusion scrap

• E-waste recovery potential

Malaysia

Malaysia is a major secondary metal processing hub importing and reprocessing regional scrap flows.

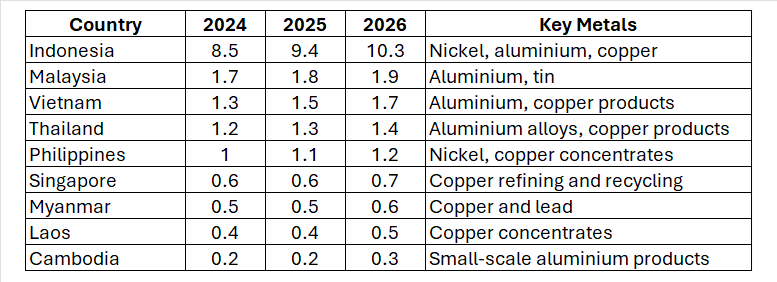

Primary Nonferrous Materials Production by Country (2024–2026)

Table 2: Estimated Primary Nonferrous Production (Million Tonnes)

Major Regional Trends

Major Regional Trends

Nickel Expansion in Indonesia

Indonesia dominates regional nickel production through:

• Integrated smelting investments

• Chinese-backed industrial parks

• EV battery supply chain development

• Stainless steel expansion

Aluminium Growth

Aluminium demand and production are rising due to:

• Construction sector growth

• Solar panel installations

• EV light weighting trends

• Packaging demand

Copper Demand Growth

Copper usage is accelerating because of:

• Renewable energy projects

• Grid expansion

• Electronics manufacturing

• Data centre investments

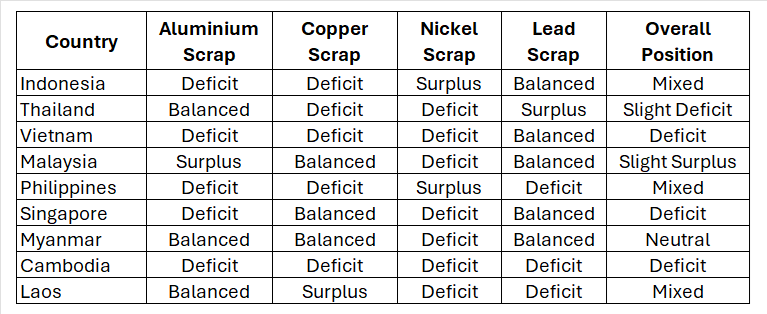

Surplus or Deficit Position of Nonferrous Scrap

Table 3: Regional Scrap Surplus/Deficit Status (2025)

Analysis

Analysis

• Indonesia remains a large importer of aluminium and copper scrap despite abundant nickel resources.

• Vietnam is heavily dependent on imported scrap for manufacturing.

• Malaysia acts as a regional scrap aggregation and redistribution hub.

• Thailand’s automotive recycling sector supports lead and aluminium recovery.

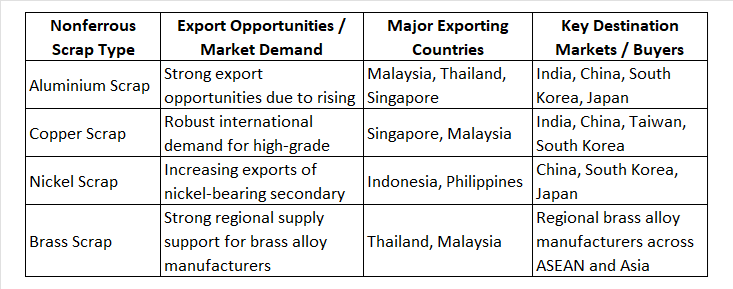

Table:5 Export Opportunities for Nonferrous Scrap

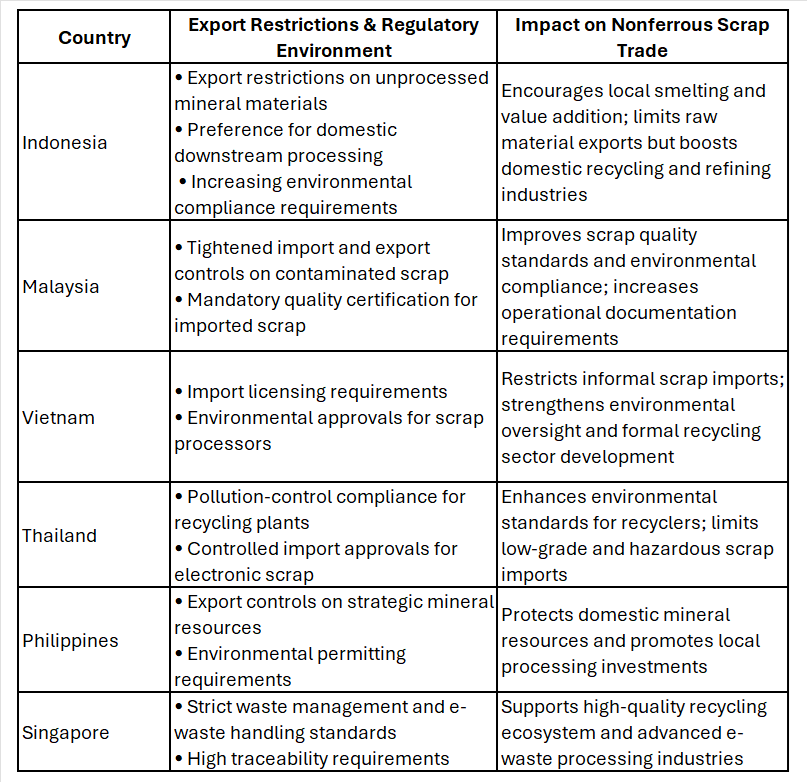

Export Restrictions and Regulatory Environment

Export Restrictions and Regulatory Environment

Export Restrictions and Regulatory Environment in Southeast Asia

E-Waste Recovery

Singapore and Vietnam are expanding:

• Precious metal recovery

• Copper recovery

• Secondary aluminium recovery

Export Restrictions and Regulatory Environment

Table: 6 Export Restrictions and Regulatory Environment in Southeast Asia

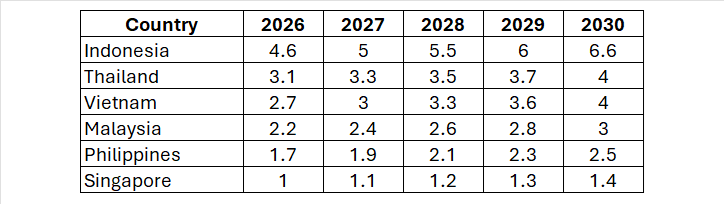

Forecast: Primary Nonferrous Materials Production (2026–2030)

Forecast: Primary Nonferrous Materials Production (2026–2030)

Table 7: Forecast Primary Production (Million Tonnes)

Forecast Drivers

Energy Transition

The expansion of EVs, batteries and renewable energy will boost demand for:

• Copper

• Aluminium

• Nickel

• Lead

Infrastructure Investments

Large-scale infrastructure projects across ASEAN will support sustained metal consumption.

Recycling Expansion

Secondary metal production is projected to grow faster than primary metal production due to:

• ESG policies

• Lower carbon emissions

• Cost advantages

• Scrap availability improvements

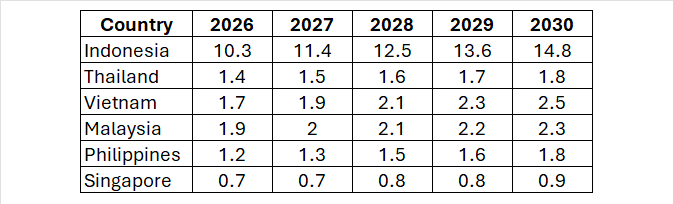

Forecast: Nonferrous Scrap Generation (2026–2030)

Table 7: Forecast Scrap Generation (Million Tonnes)

Growth Segments

Fastest-growing scrap categories:

1. Aluminium scrap

2. Copper wire scrap

3. Lithium-ion battery scrap

4. Stainless steel scrap

5. E-waste derived metals

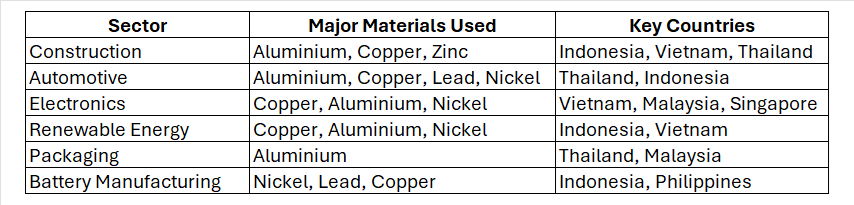

Domestic Usage of Nonferrous Materials in Southeast Asia (2024–2030)

The domestic consumption of nonferrous materials across Southeast Asia continues to expand rapidly due to industrialisation, urban infrastructure growth, renewable energy investments, automotive production and rising electronics manufacturing activities. Aluminium, copper, nickel and lead remain the most strategically consumed nonferrous materials across the region.

Indonesia, Vietnam and Thailand are expected to remain the fastest-growing consumers through 2030 because of expanding manufacturing ecosystems and energy transition projects.

Key Consumption Drivers

1.Infrastructure & Construction

Rapid urbanisation across ASEAN nations is driving strong demand for:

• Aluminium products

• Copper cables and wires

• Zinc-coated steel applications

• Brass fittings and components

2. Electric Vehicles & Battery Industry

The EV transition is significantly increasing demand for:

• Nickel

• Copper

• Aluminium

• Lead-acid and lithium battery materials

Indonesia is expected to dominate battery-related nonferrous consumption.

3. Electronics Manufacturing

Vietnam, Thailand and Malaysia continue attracting investments in:

• Consumer electronics

• Semiconductor assembly

• Electrical appliances

• Data centre infrastructure

This is boosting copper and aluminium consumption substantially.

4. Renewable Energy Expansion

Solar and wind energy installations are increasing demand for:

• Copper wiring

• Aluminium frames

• Nickel-containing battery systems

Table 8: Domestic Usage of Nonferrous Materials (Million Tonnes)

Table 8: Major Nonferrous Materials Consumption by Sector

Table 8: Major Nonferrous Materials Consumption by Sector

From 2026 to 2030, the region is expected to witness:

• Strong growth in aluminium and copper demand

• Rapid expansion of battery-related metals consumption

• Higher generation of recyclable nonferrous scrap

• Increased investments in secondary metallurgy

• Rising importance of ESG-compliant recycling systems

However, the market will also face challenges including:

• Environmental compliance costs

• Scrap quality concerns

• Dependence on imported scrap in several countries

• Regulatory tightening

• Global commodity price volatility

Companies involved in nonferrous recycling, trading and downstream processing that focus on traceability, sustainability and technological upgrading are likely to gain significant competitive advantages over the coming decade.

Overall, Southeast Asia’s nonferrous industry is expected to emerge as a strategic pillar of the global metals supply chain by 2030.

Table: 9

SWOT Analysis of Nonferrous Scrap Generation & Export Potential in Southeast Asia

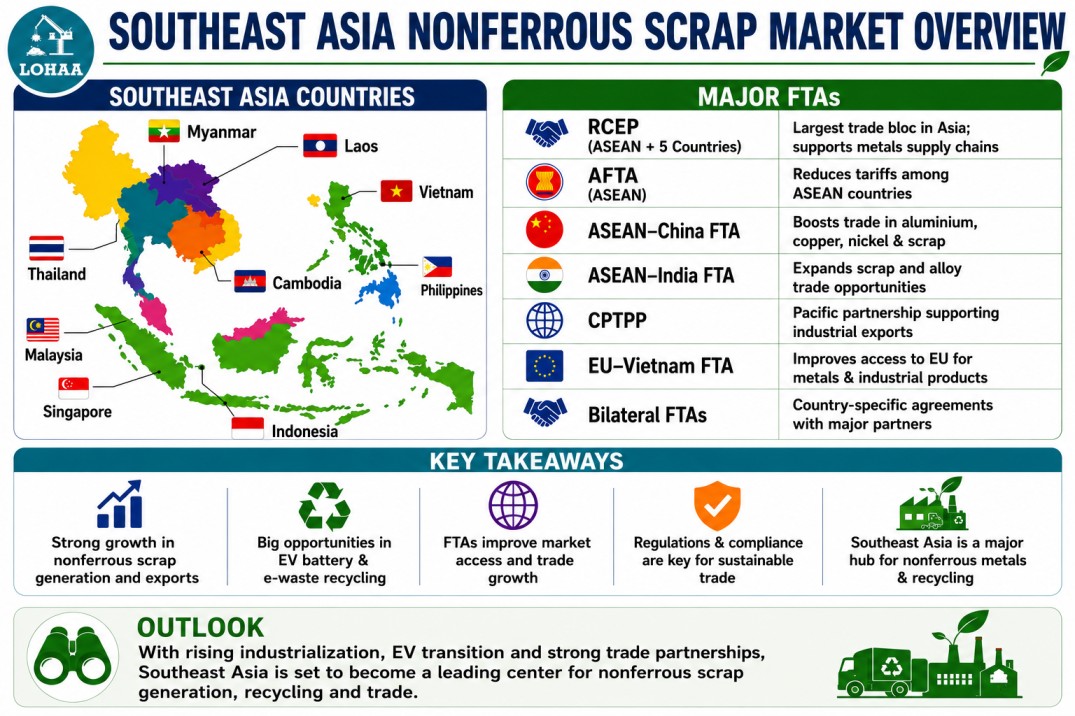

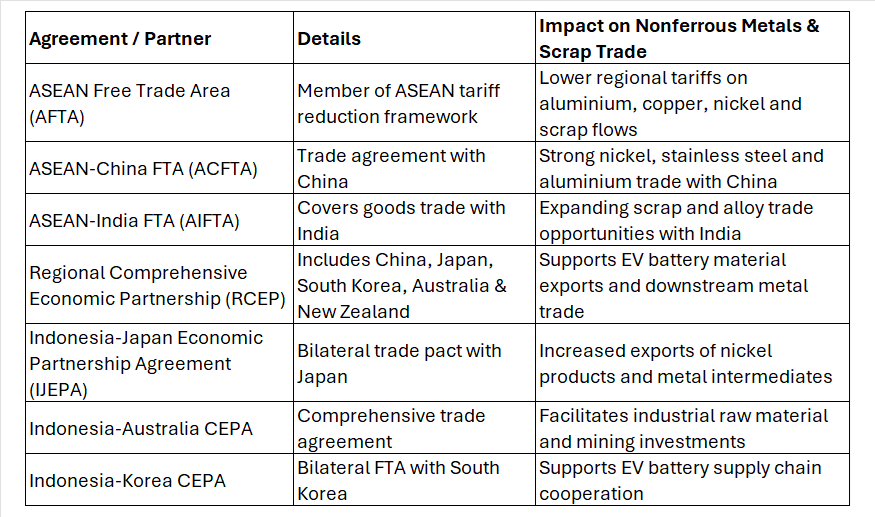

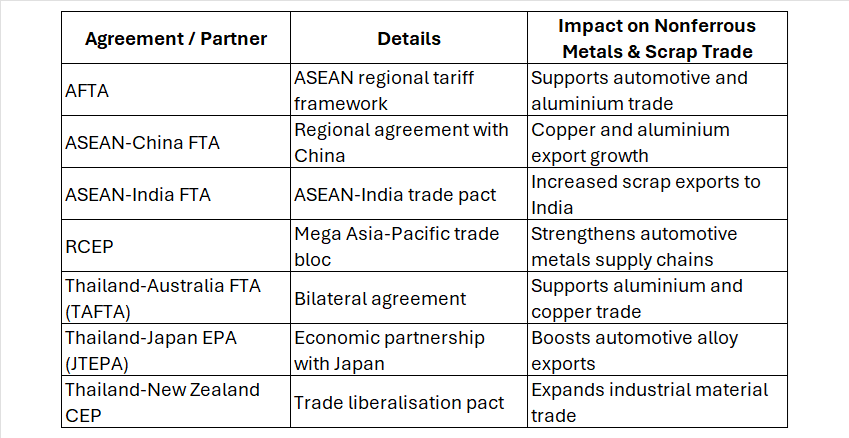

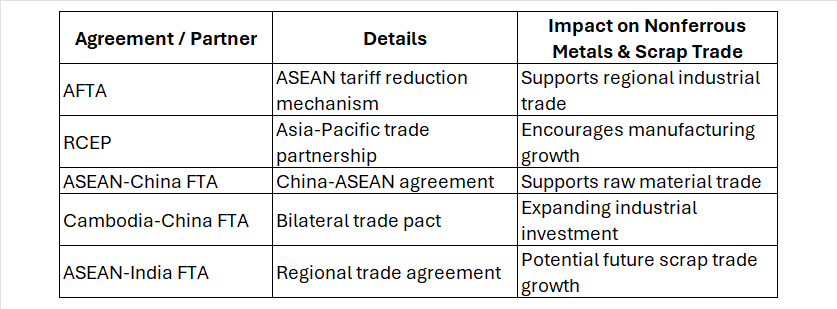

Free Trade Agreements (FTA) of Southeast Asian Countries – Country-wise Detailed Overview

Free Trade Agreements (FTA) of Southeast Asian Countries – Country-wise Detailed Overview

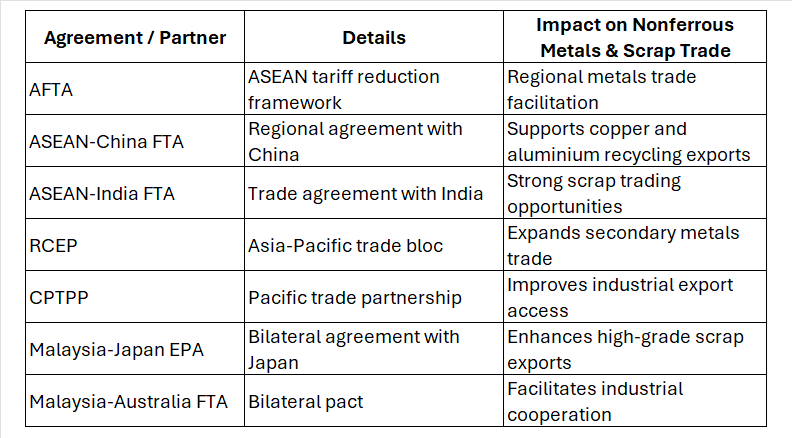

Indonesia

Key Benefits

Key Benefits

• Strong export advantage for nickel and stainless steel products

• Attracts foreign investment into smelting and recycling

• Lower tariffs improve competitiveness in Asian markets

Thailand

Key Benefits

Key Benefits

• Automotive manufacturing exports gain tariff advantages

• Improved market access for recycled aluminium and copper

• Strong integration into regional supply chains

Vietnam

Key Benefits

Key Benefits

• Access to EU and CPTPP markets

• Increased foreign investment in manufacturing

• Lower export tariffs improve competitiveness

Malaysia

Key Benefits

Key Benefits

• Strengthens Malaysia’s role as regional recycling hub

• Improved access to Asian and Pacific markets

• Enhances logistics and re-export activities

Philippines

Key Benefits

Key Benefits

• Supports nickel exports to battery markets

• Improves foreign investment prospects

• Facilitates downstream industrial development

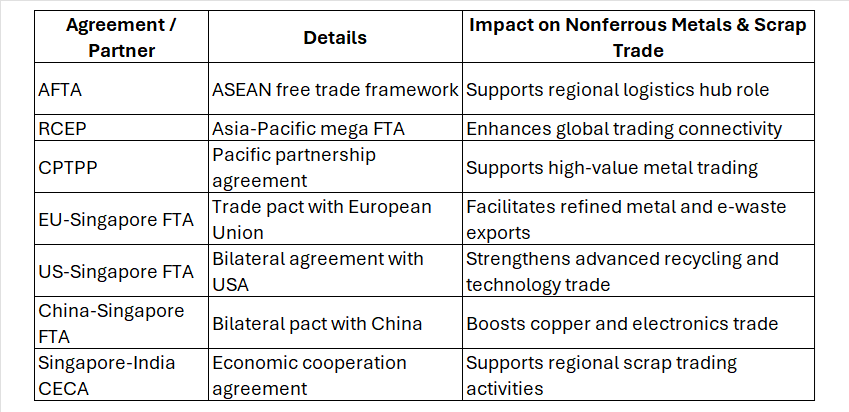

Singapore

Key Benefits

Key Benefits

• Strongest trade connectivity in ASEAN

• Major global metals trading centre

• Facilitates high-value recycled materials trade

Myanmar

Key Benefits

Key Benefits

• Regional integration opportunities

• Access to neighbouring ASEAN markets

Challenges

• Political instability limits full FTA utilisation

• International sanctions affect trade participation

Cambodia

Key Benefits

Key Benefits

• Manufacturing expansion support

• Improved market access for industrial products

Laos

Key Benefits

Key Benefits

• Better connectivity with China and Thailand

• Supports copper and mineral exports

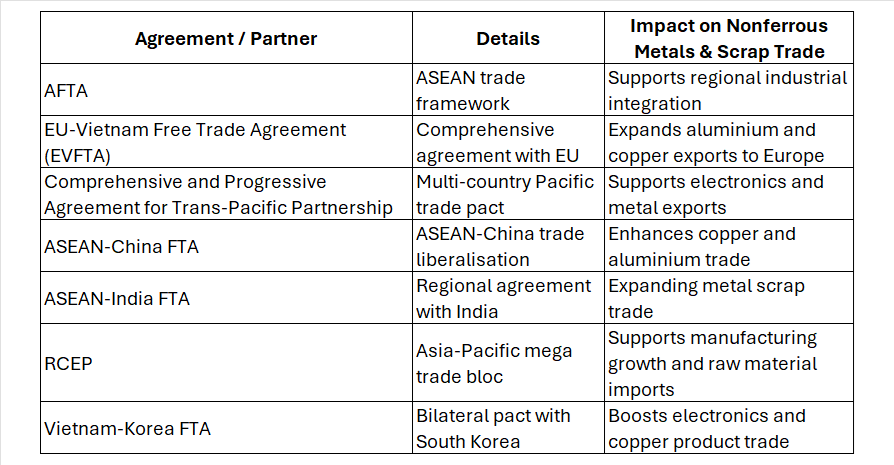

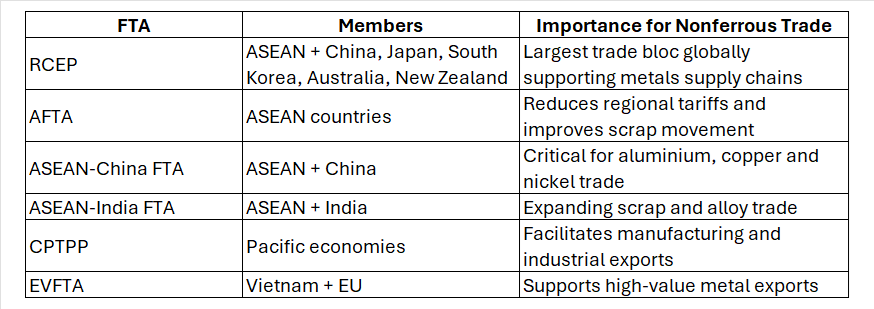

Major Regional FTAs Influencing Southeast Asia

Strategic Impact of FTAs on Nonferrous Scrap & Metals Trade

Strategic Impact of FTAs on Nonferrous Scrap & Metals Trade

Positive Impacts

• Lower tariffs on scrap and primary metals

• Improved supply chain integration

• Increased foreign investment

• Expansion of EV battery supply chains

• Better logistics and customs cooperation

Challenges

• Environmental compliance standards

• Rules of origin requirements

• Competition among ASEAN exporters

• Trade policy uncertainty in strategic minerals

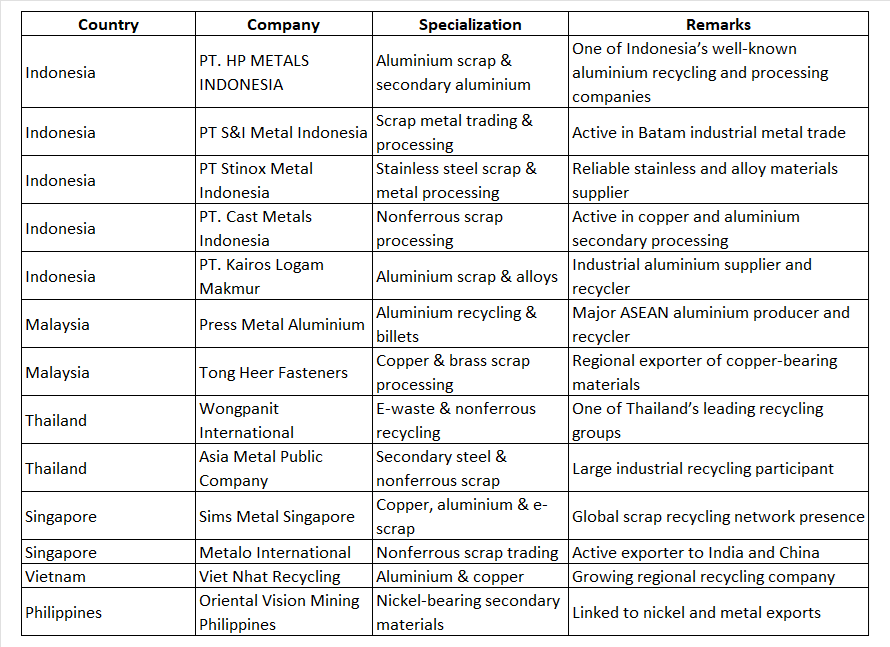

Here are some of the top-rated and reliable nonferrous scrap exporters and processors across Southeast Asia, particularly active in aluminium, copper, stainless steel, nickel-bearing scrap and secondary metals trade.

Key Southeast Asian Export Strengths

- Indonesia dominates nickel-bearing scrap and stainless steel secondary materials.

- Malaysia and Singapore are strong in copper and aluminium scrap exports.

- Thailand leads in automotive aluminium scrap and brass recycling.

- Vietnam is rapidly expanding e-waste and copper recycling activities.

The region continues to benefit from growing demand from India, China, Japan and South Korea for secondary nonferrous raw materials.

Conclusion

Southeast Asia is rapidly transforming into one of the world’s most important nonferrous metals and recycling regions. The combined impact of industrialisation, infrastructure expansion, electric vehicle manufacturing, renewable energy investments and circular economy initiatives is significantly reshaping regional metal flows.

Indonesia will remain the dominant force in nickel production and battery-material development, while Vietnam and Thailand are expected to strengthen their positions as manufacturing and consumption hubs for aluminium and copper products. Malaysia and Singapore will continue serving as important processing and redistribution centres for secondary nonferrous materials.

From 2026 to 2030, the region is expected to witness:

• Strong growth in aluminium and copper demand

• Rapid expansion of battery-related metals consumption

• Higher generation of recyclable nonferrous scrap

• Increased investments in secondary metallurgy

• Rising importance of ESG-compliant recycling systems

However, the market will also face challenges including:

• Environmental compliance costs

• Scrap quality concerns

• Dependence on imported scrap in several countries

• Regulatory tightening

• Global commodity price volatility

Companies involved in nonferrous recycling, trading and downstream processing that focus on traceability, sustainability and technological upgrading are likely to gain significant competitive advantages over the coming decade.

Overall, Southeast Asia’s nonferrous industry is expected to emerge as a strategic pillar of the global metals supply chain by 2030.

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)