Aluminium Scrap 2026: CBAM, Gulf Risk & India Trade

Introduction

The global aluminium market in 2026 stands at a critical inflection point. Two converging forces — geopolitical tension in the Gulf region and the European Union’s Carbon Border Adjustment Mechanism (CBAM) — have reshaped global trade flows, supply chains, and industrial strategies.

For India, one of the world’s largest aluminium scrap importers (~2 million tonnes in 2025), these developments have struck both opportunity and vulnerability.

As global supply chains tighten and carbon policies evolve, India’s aluminium recycling and manufacturing sectors are reimagining their strategies to ensure cost efficiency, sustainability, and competitive advantage.

1. Gulf Conflict: The Supply Shock

Supply Chain Disruptions

The Middle East — especially the UAE and Saudi Arabia — plays an outsized role in the aluminium ecosystem, contributing nearly 9% of global primary aluminium production and supplying 20–30% of India’s aluminium scrap imports.

The Gulf conflict of 2025–2026 has disrupted shipping through the Strait of Hormuz, directly impacting freight prices and insurance premiums.

As a result, aluminium scrap prices in India rose ~30% year-on-year. Secondary aluminium smelters began operating at 20–40% lower capacity, especially affecting automotive and extrusion producers reliant on imported scrap.

Strategic Shifts

• Diversification: Imports increasingly redirected from the USA and EU.

• Domestic recycling initiatives gained traction.

• Stockpiling behaviors intensified among importers anticipating longer lead times.

2. Changing Import Structure & Market Realities

India’s aluminium scrap imports remain heavily concentrated among a few regions and suppliers. Disruptions from the Gulf drove freight and prices higher and forced India to rely more on US and EU suppliers known for consistent quality. Meanwhile, Southeast Asia’s re-export hubs (Malaysia, Thailand, Vietnam) emerged as secondary sources offering flexibility but lower-grade material.

Disruptions from the Gulf drove freight and prices higher and forced India to rely more on US and EU suppliers known for consistent quality. Meanwhile, Southeast Asia’s re-export hubs (Malaysia, Thailand, Vietnam) emerged as secondary sources offering flexibility but lower-grade material.

3. The CBAM Factor: A Carbon-Cost Revolution

3. The CBAM Factor: A Carbon-Cost Revolution

The EU’s CBAM (Carbon Border Adjustment Mechanism) – implemented in January 2026 – applies a carbon levy on aluminium, steel, and other high-emission goods imported into the European Union.

The regulation ties import costs to embedded CO? emissions, aligning with EU ETS (Emission Trading System) prices. This discourages carbon-intensive production and rewards low-carbon, scrap-based aluminium products. Emission Benchmarks

Emission Benchmarks

• Primary aluminium: 1.423 t CO2/t

• Secondary aluminium (scrap-based): 0.091 t CO2/t

This differentiation creates a cost advantage of over 90% for recycled aluminium, promoting scrap trade and domestic recycling in countries like India.

4. Impact on India’s Export Dynamics

As a result of CBAM, India’s aluminium exports face an additional cost burden of 15–22% depending on carbon footprint levels. This shift forces exporters to move away from the EU toward Asia and Gulf markets for volume retention.

India's Strategic Response

• Accelerated adoption of “green aluminium” projects

• Expansion of scrap-based production capacity

• Diversification away from Europe-centric exports

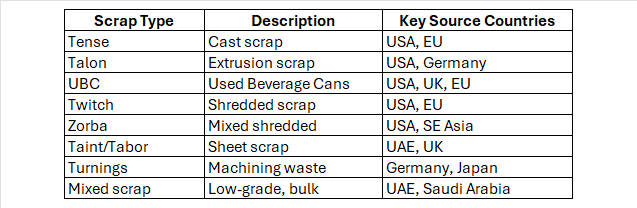

5. Aluminium Scrap Ecosystem: Types & Sources

Recycling aluminium saves ~95% energy compared with producing primary aluminium. This makes it the cornerstone of future decarbonization and CBAM compliance.

Recycling aluminium saves ~95% energy compared with producing primary aluminium. This makes it the cornerstone of future decarbonization and CBAM compliance.

6. Regional Scrap Generation in India (2025 Estimate) Total estimated domestic scrap generation: 2.1 million tons – still below national demand, explaining reliance on imports covering ~85% of needs.

Total estimated domestic scrap generation: 2.1 million tons – still below national demand, explaining reliance on imports covering ~85% of needs.

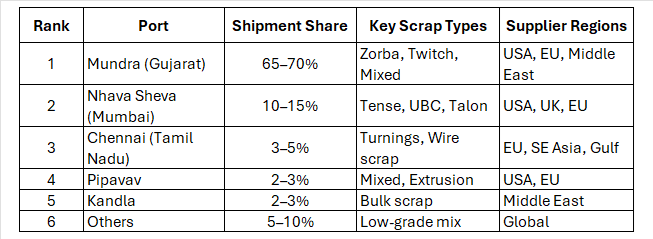

7. Port-Wise Import Dynamics (India, 2025)

Mundra Port has emerged as India’s aluminium scrap capital — cost-efficient, connected to Gujarat’s recycling corridor, and optimized for bulk shipments.

Nhava Sheva specializes in high-grade and containerized scrap, while Chennai sustains South India’s die-casting and engineering clusters.

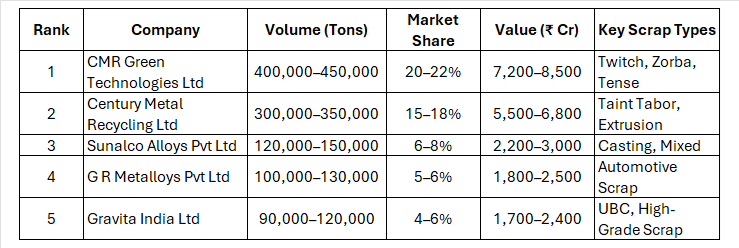

8. Top Importing Companies (India, 2025)

This shows a highly consolidated top, with fragmented lower tiers relying heavily on fluctuating Gulf supply.

This shows a highly consolidated top, with fragmented lower tiers relying heavily on fluctuating Gulf supply.

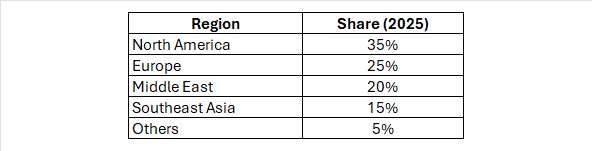

9. Global Supply Links: USA, EU & UAE

Key Observations

Key Observations

• USA: Dominates ~60% share due to abundant, clean, and sorted scrap.

• European Union: Supplies premium, CBAM-compliant material for value-added production.

• UAE: Acts as a trading bridge, aggregating and re-exporting scrap globally.

This triangulation enables India to balance cost, supply security, and sustainability.

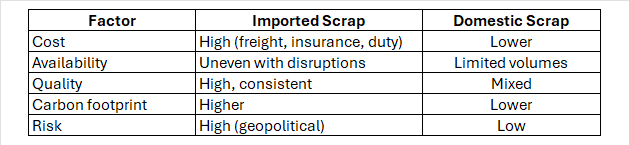

10. Imported vs Domestic Scrap: Cost-Benefit Analysis

Conclusion: Building strong domestic recycling ecosystems is India’s best medium-term strategy to hedge against geopolitical uncertainty and CBAM-related trade barriers.

Conclusion: Building strong domestic recycling ecosystems is India’s best medium-term strategy to hedge against geopolitical uncertainty and CBAM-related trade barriers.

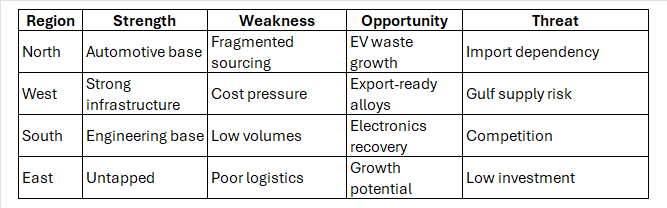

11. Regional Recycling Structure in India

While West and North India dominate processing, South India holds significant potential for expansion through electronics and EV-related scrap.

While West and North India dominate processing, South India holds significant potential for expansion through electronics and EV-related scrap.

12. SWOT Analysis: Regional Scrap Ecosystem 13. Aluminium Exports: India’s 2025 Snapshot

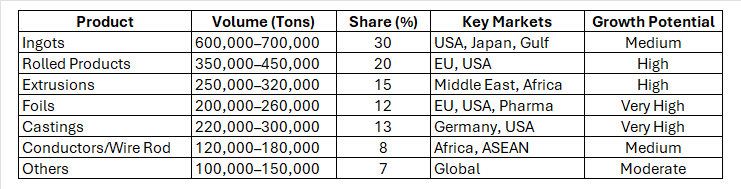

13. Aluminium Exports: India’s 2025 Snapshot

India exported 1.8–2.2 million tonnes of aluminium finished and semi-finished products in 2025, spanning ingots, foils, extrusions, and rolled products.

Export Growth Drivers (2026–2030)

• Global China+1 diversification

• Surge in demand for EV components

• Foil demand from pharma & food sectors

• CBAM incentive for certified low-carbon aluminium

Product-Level Highlights

Product-Level Highlights

• Foils: Fastest-growing, pharma-driven

• Castings: Key in global EV chains

• Rolled Products: Benefit from CBAM realignment

• Extrusions: Bolstered by Middle East infrastructure growth

15. Strategic Outlook (2026–2030)

Key Trends

• Accelerating recycling capacity investments

• Scrap as strategic resource, not residue

• Formation of regional trade blocs for low-carbon materials

• Expansion of CBAM-like carbon trade systems globally

• Global secondary aluminium already approaching 42.4 million tons annually

16. Strategic Recommendations

For Industry Leaders:

• Build deeper USA–EU supply partnerships

• Invest in traceable, low-carbon aluminium

• Localize recycling clusters and standardize quality

• Optimize port logistics and inland connectivity

For Policymakers:

• Support domestic scrap recovery programs

• Simplify import tariffs for secondary producers

• Encourage green certification frameworks compatible with CBAM

For Traders & SMEs:

• Diversify sourcing (UAE, SE Asia)

• Develop carbon reporting readiness

• Form consortiums to pool logistics and finance

17. Conclusion

By 2026, the aluminium scrap industry has moved from being a niche recycling segment to a globally strategic ecosystem.

• The Gulf conflict has exposed supply risks and overdependence.

• CBAM has triggered a transformative shift toward green, traceable, low-carbon trade.

• India’s recyclers — led by structured giants like CMR and Century Metal Recycling — are turning adversity into advantage by strengthening supply chains, improving quality, and scaling capacity.

India’s aluminium future depends on local recycling agility, diversified sourcing, and green compliance. Scrap is no longer a by-product — it is a vital industrial asset that defines competitiveness and sustainability in the global aluminium economy.

References

- Reuters – Gulf conflict disrupts aluminium scrap supply (2026)

- European Aluminium – CBAM Report (2025)

- Argus Media – CBAM Benchmarks Update (2025)

- Times of India – CBAM Impact on Indian Exports

- Lohaa Market Report – India Aluminium Scrap Imports 2025–26

- Volza Trade Data – India Aluminium Scrap Shipments

- BigMint – Global Aluminium Scrap Outlook 2026

- GTAIC Market Dashboard – India Scrap Forecast 2026

- OEC Global Trade Data – Aluminium Scrap in India (2025)

By using digital trade platforms like LOHAA Mobile application, you can reach global buyers, source quality material, and strengthen long-term partnerships.

Download the LOHAA Mobile application today and connect with verified scrap suppliers and manufacturers.

(Notes: market and production volume estimates are synthesized from public market reports and industrial press; exact tonne figures for materials are not centrally published in a single comprehensive public dataset, therefore the numeric projection above is a conservative, documented estimate built from available intelligence and reasonable regional share assumptions.)